Systemic Fear, Modern Finance and the Future of Capitalism

Shimshon Bichler and Jonathan Nitzan[1]

Jerusalem and Montreal, July 2010

![]()

CreativeCommons: Attribution-Non Commercial-No Derivatives

Existing theories of political economy, liberal as well as Marxist, see capital as a dual entity. According to these theories, the “real” essence of capital consists of material/productive commodities, while the “financial” appearance of capital either accurately mirrors or fictitiously distorts this underlying reality. We reject this duality. Capital, we argue, is finance, and only finance. In its modern incarnation, capital exists as forward-looking capitalization, a universal financial ritual that discounts expected future earnings to a singular present value.

The universality of this reduction makes capitalization the most supple power instrument ever known to humanity. Previously, distributive power was associated with clear socio-ecological distinctions – differences between king and subject, owner and slave, tiller and landlord, field and citadel, village and town. Capitalization flattens these qualitative features to the point of irrelevance. In principle, anyone can be a capitalist, and what distinguishes one capitalist from another is the quantity of their capitalization: the most powerful are those with the greatest capitalization (dominant capital), and those that hold that power achieve and augment it by increasing their capitalization faster than others (differential accumulation). In this way, capitalization crystallizes the power of capitalists to shape their world, as well as the resistance of those that oppose this power. It gauges the capitalists’ success in directing production and consumption, in shaping ideology and culture, in affecting the law, public policy, conflict, war and even the environment. It is the all-encompassing algorithm that creorders – or creates the order – of the capitalist mode of power.

The purpose of our paper is to examine the breakdown of this algorithm. To be sure, this type of inquiry is hardly novel. Marxists have long searched for objective signs of capitalist collapse, preliminary omens that would foretell the system’s imminent disintegration. However, because of their dual conception of capital, they’ve tended to look for such signs in the so-called real sphere of production and consumption, while paying far less attention to finance, which, in their view, is merely a distorted mirror of that reality. But finance isn’t a mirror of real capital; it is real capital – and indeed the only real capital. So if we want to look for signs of systemic crisis and possible disintegration, our search should begin here, in the very ritual of capitalization.

The specific focus of the article is two historical ruptures of modern finance – the periods of 1929-1939 and 2000-2010. During both periods, capitalists abandoned the conventional forward-looking ritual of capitalization, resorting instead to the backward-looking posture of pre-modern finance. In our view, these rare episodes are of great importance for understanding the nature of capitalist confidence and the capitalists’ ability to rule – as well as the possibility that this system of rule will collapse. Our inquiry seeks, first, to characterize key features of these episodes; second, to speculate on their causes; and third, to assess, however speculatively, what they might imply for the future of capitalism.

Propositions

We set the stage with a number of related propositions. These propositions aim to establish a “nested relationship” between a series of entities – beginning from the broad concept of a mode of power, and continuing with confidence in obedience, dominant ideology, the ritual of capitalization and the forward-looking disposition of modern finance. Most of time, the components of this nested relationship are mutually reinforcing. But on rare occasions the relationship implodes. The trigger for such implosion is systemic fear: fearing for the collapse of their system, capitalists lose sight of the future; with the future having become opaque, the ritual of capitalization falls into disarray; with capitalization having been punctured, dominant ideology is deeply shaken; with dominant ideology having cracked, the capitalists’ confidence in obedience tumbles; and with no confidence in obedience, the very continuation of the capitalist mode of power is put into question. Let’s examine the relationship between these concepts more closely, beginning with power.

● Modes of power and confidence in obedience. Hierarchical societies, we argue, are characterized by their modes of power. Every mode of power – whether slave-based, feudal or capitalist – rests on confidence in obedience: the confidence of rulers in the obedience of their subjects. This confidence is never perfect: the ruled often resist, rise up and revolt; occasionally they demand and periodically achieve moderate change; sometimes they even manage to effect significant reform; and in very rare instances they take over power, though only for a brief historical moment. But as long as the bottom-up disobedience of the underlying population does not significantly undermine the top-down confidence of those who rule them – a breach that seldom happens on a large enough scale – the mode of power itself remains intact.

● Confidence in obedience and dominant ideology. The framework that shapes and fixates this confidence in obedience is the dominant dogma, or ideology: the broad belief system that propels and restricts the social imagination. The dogma or ideology that dominates a given mode of power conditions action and inaction, justifies the prevailing social structure and provides its organizing principles. It molds rulers and ruled alike – and in so doing locks them both into the same mode of power.

● Dominant ideology and capitalization. The dominant ideology of modern capitalism revolves around the ritual of capitalization: the financial algorithm that discounts expected future earnings to their present value. This ritual is all pervasive. The capitalist system is denominated in prices, and for the past century or so, the habitual price-setting mechanism has been capitalization. Discounting seems to pervade every thing and every process: it determines the prices of human life and its genomic code; it sets the prices of consumer goods and services, it generates the prices of corporate assets and government debt; it calculates the prices of military operations and humanitarian aid; it is even used to compute the price of our ecological future. The imperatives of capitalization are accepted, internalized and obeyed, usually without question, by the rulers as well as the ruled – and that acceptance makes capitalization central to the dominant ideology of our society.

● Capitalization and the forward-looking outlook. The ritual of capitalization is feverishly forward looking: it is concerned not with the past or the present, but with the future. The elementary particles of capitalization – earnings, investors’ hype, risk perceptions and the normal rate of return – represent not what is known to have happened, but what is expected to happen. The expectations themselves are inherently uncertain and always in flux. But underneath their shifts and turns, one thing remains constant: the conviction that the capitalization process itself will continue to rule and organize humanity, forever.

This latter conviction is necessary for the existence of modern capitalism, at least in its present form, and the easiest way to demonstrate that necessity is to assume it away. Suppose for argument’s sake that capitalists, instead of expecting capitalization to continue indefinitely, believed that the process would cease to exist at some future point. At that point, with capitalization gone, their assets would have a nil value, by definition; and with future prices being zero, current prices would have nowhere to trend but down. Now, the fact that capitalists invest shows that they expect the very opposite – i.e., that the value of their assets will grow, not contract – and that expectation means that, consciously or not, they also think that the ritual that valuates their assets will never end.[2]

These propositions lead to two related conclusions. First, they suggest that the very existence of capitalization attests to the capitalist confidence in obedience. The fact that this ritual is so pervasive implies that most people believe it will remain so; and the only way for this ritual to remain pervasive is if capitalists are convinced that they can continue to impose it on a society that is unwilling or unable to oppose it. The second conclusion is that a protracted breach of capitalization – a period during which the ritual breaks down – signifies the loss of confidence in obedience, the potential disintegration of the dominant ideology and, ultimately, a threat to the very existence of the capitalist mode of power. If correct, these conclusions can offer a quantitative insight into the long-term outlook of the ruling capitalist class – and, by extension, into the prospect of systemic change to the capitalist mode of power.

The first question, then, is how do we know that capitalization has “broken down”? What are the features of such a breakdown? How do these features differ from investment as usual? Can these features be quantified – and if so, how?

Takeoff

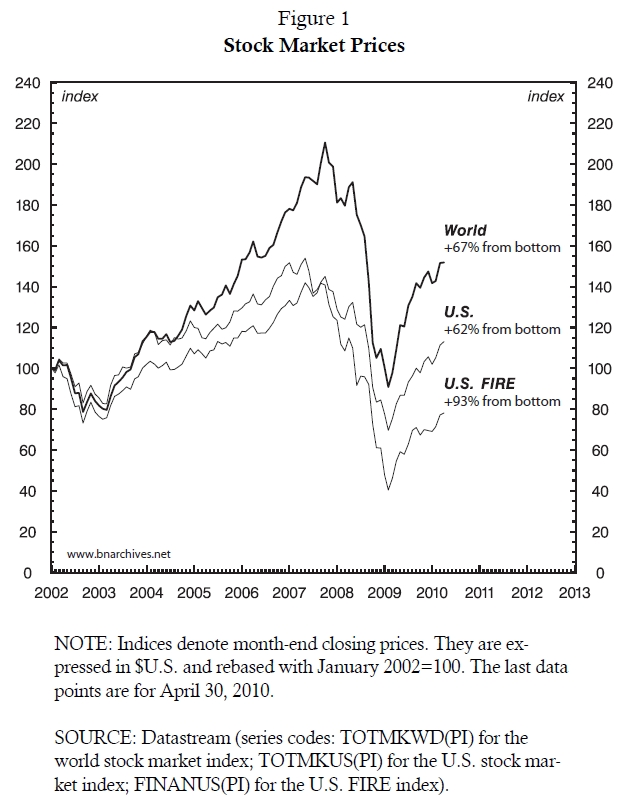

To begin answering these questions, let us backtrack a bit and consider the situation in early 2010. The capitalist class is finally seeing light at the end of the tunnel. For many months now, its analysts, statisticians and public officials have been spotting “green shoots” everywhere they look. The snowballing global recession, they say, seems to have slowed down and perhaps even ended. Managers the world over are purchasing more inputs after a period of buying much less; the factories of Asian exporters are running at full steam; raw material prices have rebounded strongly; bank lending is reviving and home owners are starting to refinance their mortgages at lower rates; and in the United States, the world’s biggest producer-consumer, initial unemployment claims seem to have peaked, while consumers are beginning to loosen their purse strings. But the most important sign that the worst of the crisis is over comes from the equity market: stock prices are the ultimate barometer of capitalist health, and they have been soaring.

The market takeoff is evident in Figure 1. The chart traces the U.S. dollar price of three key indices – all world equities, U.S. equities, and the equities of the U.S. FIRE sector (finance, insurance and real estate). All three indices show a sharp, synchronized rise. In slightly more than a year, from February 2009 to April 2010, the world index gained 67%, the U.S. index 62%, and the U.S. FIRE index – previously the most battered of the three – a whopping 93%.

Suddenly, the bulls are everywhere. The greatest returns are usually earned during the initial part of a rally, and no respectable fund manager likes being beaten by a rising average. With the economy apparently bottoming out and with the stock market having been in a major bear phase for nearly a decade, investors are no longer afraid of losing money; their fear now is not making enough of it.[3] And so arises the specter of “panic buying,” a frenzied attempt to jump on the bandwagon before the really large gains are gone.[4]

Of course, not everyone buys this rosy scenario. Many observers continue to feel that the recent stock market rally is no more than a dead-cat bounce. In the eyes of the pessimists, investors are knee-jerking to a false start. The economic recovery, they say, will be W-shaped, and the market will re-collapse before any real boom can begin. This recession, they warn, is nasty and likely to linger for years.[5]

Looking Forward

Regardless of who is right, though, there is something fundamentally wrong with the debate itself. The current news may be good or bad, revealing or misleading – but, then, investors aren’t supposed to take their cue from the current news in the first place.

To trade assets on the basis of today’s statistics is to be backward looking. It is to be retrospective rather than predictive, to react rather than initiate, to trail rather than lead. It puts investors at the tail end of social dynamics.

Needless to say, such behavior is entirely improper. According to the sacred annals of modern finance, formalized a century ago by Irving Fisher (1907) and popularized during the Great Depression by Benjamin Graham and David Dodd (1934), asset prices are forward looking: “The value of a common stock,” dictate Graham and Dodd in their immortal doorstopper, “depends entirely upon what it will earn in the future” (p. 309).

These lines were written against the backdrop of the 1920s. The roaring stock market and the accompanying optimism ushered in by the end of the First World War offered a fertile breeding ground for what Graham and Dodd called the “New-Era Theory,” especially in the land of limitless possibilities. The principles of discounting the future gained adherents, and soon enough past profits became passé. They no longer mattered for the stock market. From now on, declared the gurus of finance, one should view the markets “from the standpoint of eternity, rather than day-to-day” (Benjamin Graham quoted in Zweig 2009). Looking forward, the only thing that counted was the future trend of earnings.[6]

It should be noted, though, that initially this approach didn’t win too many supporters. In fact, it faced a rather stiff opposition, and not for naught. The late nineteenth century gave birth to a new entity: the modern, publicly traded corporation. It was an entirely novel way of organizing business, both inside and outside the firm, and it spread very quickly, carried on a tidal wave of public offerings. Forward-looking securities of every color, size and denomination were being floated in ever larger numbers, all promising a future of riches to the daringly prescient, and the sheer magnitude and exponential growth of it all left economists baffled and public officials gasping for air.

At the time, there were very few theoretical tools and scarcely any data to make sense of this new development. There was no corporate transparency to speak of, no models to predict future earnings, let alone their trend, and no formal methods to assess risk. To make matters worse, the newspapers were only too happy to amplify the forward-looking exploits of corporate promoters. The key owners and their bankers were blamed, not without cause, for “overcapitalizing” their assets and “watering” their stocks relative to their “actual” (read greenfield) investments – all in order to rip off the innocent public.[7]

The whole thing smelled of a racket: “the principle that capitalization should be based on earning capacity rather than on actual cost,” declared one disgruntled rejectionist, “is not only unsound in theory but is also vicious in its practical application” (Bonbright 1921: 482). Under these conditions, officials and theorists were unsure of how to reconcile the new practice of discounted future earnings with the familiar “par value.” It seemed much easier to stick to the conservative principles of “historical cost” accounting.

In retrospect, though, these were futile acts of resistance. Forward-looking finance was not a mere technical gismo. It was the basis for a totally new architecture of power: capitalization. As noted, capitalization is a symbolic financial entity, a ritual that the capitalists use to discount to present value risk-adjusted expected future earnings. This ritual has a very long history. It was first invented in the capitalist bourgs of Europe, probably sometime during the fourteenth century. It overcame religious opposition to usury in the seventeenth century, to become, for the first time, a conventional practice among bankers. And its mathematical formulae, previously relying on habit and rules of thumb, were first rigorously developed and synthesized in the mid-nineteenth century by a group of German foresters. But it was only in the late nineteenth century, with the birth of the publicly-traded modern corporation, that these principles were poised to become the broad norm of what we now call modern finance.[8]

Capitalization: Marx’s Fiction

Karl Marx, one of the first to dissect the social underpinnings of capitalization, sided with the rejectionists. The capitalist system, he said, fancies two different entities: “actual” capital and “illusionary” or “fictitious” capital. The driving force of the system is actual capital, which exists as commodities. For Marx, actual capital comprises means of production, work in progress and commodity money, whose prices are governed by the reality of labor time, whether historical or current. By contrast, fictitious capital is an ownership claim on future earnings, an illusionary entity whose price is the present value of those earnings.[9]

According to Marx, the latter entity is fictitious for three separate reasons. First, the ownership claim on earnings often has no “actual” principal to call on, as is the case with state debt, for instance. Second, the claim extends into the uncertain future: it capitalizes expected earnings, and these could easily fail to materialize. Third and finally, discounting depends on the rate of interest, which means that the same flow of earnings can give rise to many different levels of capitalization (Marx 1909, Vol. 3: 546-47 and 550-51).

For Marx, then, actual and fictitious capitals are totally different creatures. They consist of different entities, and they are quantified through different processes – the former via past and current productive labor time, the latter through future earnings expectations and the rate of interest. So, when considered separately, their respective magnitudes and movements need have nothing in common. The problem, though, is that they cannot be considered separately. The capitalist system is denominated in prices, and as Marx himself conceded, prices are affected by both fictitious and actual accumulation. As a result, any divergence of the former from the latter is bound to “distort” the value system:

All connection with the actual process of self expansion of capital is thus lost to the last vestige, and the conception of capital as something which expands itself automatically is thereby strengthened. . . . The accumulation of the wealth of this class [the large moneyed capitalists] may proceed in a direction very different from actual accumulation. . . . Moreover, everything appears turned upside down here, since no real prices and their real basis appear in this paper world, but only bullion, metal coin, notes, bills of exchange, securities. Particularly in the centers, in which the whole money business of the country is crowded together, like London, this reversion becomes apparent; the entire process becomes unintelligible” (Marx 1909, Vol. 3: 549, 561 and 576, emphases added).

These considerations led Marx – and many Marxists since – to view the “illusion” of capitalization as antithetical to the “real” essence of value and accumulation, and therefore as offering only secondary insight into the larger analysis of capitalism.[10] The seemingly independent gyrations of fictitious capital of course could be hugely important, and in recent years Marxists have put increasing effort into their analysis. But this importance is mostly negative and temporally limited. In the short run, capitalization wreaks havoc: it contaminates the underlying system of labor values, it sends false signals, and it amplifies the underlying economic cycle with an even more violent financial cycle that oscillates between euphoric bubbles and deflationary crashes. In the long run, though, it is the “real” economy of production, not the nominal “fiction” of finance, that counts. Production is the Galtonian anchor, the historical trend from which finance deviates and to which it must eventually revert. And since the key to capitalist development remains a proper understanding of the labor process, the extraction of surplus value and the accumulation of actual capital, Marxists never felt they needed to develop their own unique theory of capitalization, let alone to place such a theory at the heart of their analysis.

Capitalization: The Neoclassical Reconstruction

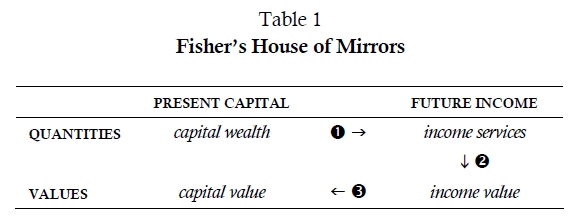

This later task was taken on by the liberals. Contrary to the Marxists, who begin from two different entities, the neoclassicists start from equivalence: capitalization both derives from and reflects the actual capital goods. One of the first stylized expressions of this symmetry is due to Irving Fisher. In an article aptly titled “What is Capital?” (1896), Fisher opens by devising a consistent set of definitions. His starting point is a distinction between “stock” (quantity at a point in time) and “flow” (quantity per unit of time). Capital is a stock; income is a flow. Capital gives rise to income, whereas income gives capital its value. The precise correspondence between these concepts is articulated in his book The Rate of Interest (1907):

The statement that “capital produces income” is true only in the physical sense; it is not true in the value sense. That is to say, capital-value does not produce income-value. On the contrary, income-value produces capital-value. . . . [W]hen capital and income are measured in value, their causal connection is the reverse of that which holds true when they are measured in quantity. The orchard produces the apples; but the value of the apples produces the value of the orchard. . . . We see, then, that present capital-wealth produces future income-services, but future income-value produces present capital-value. (13–14, original emphases)

The feedback loop is illustrated in the Table 1, adopted from Fisher (14):

Explanation: In the material world, depicted by step 1 of the sequence, capital wealth (measured by the physical quantity of capital goods) produces future income services (similarly measured by their physical quantity). In the nominal world, depicted by step 3, the income value of the future services (measured in dollars) is discounted by the prevailing rate of interest to generate the present value of capital (also measured in dollars). The two worlds are connected through step 2, whereby the physical quantity of future income services determines their dollar price.

Hypothetical numerical illustration: Intel has 10 million units of capital wealth, which, during its future life, will produce 1 billion units of income services in the form of microchip-generated utils (step 1). These 1 billion utils’ worth of services, spread over the life of the capital wealth, will fetch 100 billion dollars’ worth of future profits and interest (step 2), which in turn are discounted to 50 billion dollars’ worth of capital value (step 3).

From a theoretical standpoint, this articulation is deeply problematic – primarily because neoclassical “capital goods,” much like Marx’s “actual capital,” cannot be measured in universal units, whether we call them utils or abstract labor hours.[11] But this difficulty hardly deterred the neoclassicists. At stake here was the wholesale conversion of capitalism to a new, financial footing, and the articulations offered by Fisher and other liberal economists provided the detailed rituals on which this new capitalized structure were to stand from then to eternity.

Dominant Ideology

And, indeed, liberals soon began to believe, first, that any expected income flow can be discounted to present value; second, that, in addition to earnings, discounting reflects both the normal rate of return and the risks specific to the income in question; and finally, that capitalization applies universally across time and space. Now, since in capitalism every process has a potential impact on the flow of income, it follows that accumulation, seen through the spectacles of capitalization, incorporates, at least potentially, every aspect of social life. From this viewpoint, capital is no longer a narrow matter of economics – or, alternatively, everything is now a matter of finance. Whatever affects the future trend of earnings, risk and the normal rate of return can be capitalized; and once capitalized it becomes part of capital.

And so a new comprehensive ethic was born. What Marx dismissed as a fiction, and what early twentieth-century liberals considered a rip-off, became the new template for creordering capitalist power. By the middle of the twentieth century, the forward-looking notion that asset prices discount the deep future had replaced “actual cost” as the new creed. In the 1950s, capitalization started to appear in finance textbooks; in the 1960s and 1970s, it helped propagate portfolio theory and took over corporate budgeting; in the 1980s and 1990s, it was underwriting the worldwide spread of neoliberalism and the tenfold increase in global stock prices; and by the 2000s, it was safely established as a sacrosanct gospel, an organized belief system with more followers than all of the world’s religions combined.

The rituals of this forward-looking gospel are now articulated, published and republished in millions of learned papers and monographs, and reproduced endlessly in finance textbooks. They are deeply embedded in computer models and are hardwired into pocket calculators. Every accountant, analyst and capitalist accepts them as an article of faith; most politicians and government officials are conditioned to follow their dictates; and the remainder of humanity – from employees and small business owners, through pensioners and the unemployed, to criminals and illegal aliens – unknowingly obeys their decree. Encompassing, imposing and largely beyond dispute, forward-looking capitalization has become the heart and center of today’s dominant ideology.

The Puzzle

Now, turning from this broad discussion back to the current historical moment, a puzzle arises: if asset prices look forward to the long-term future trend of earnings, why worry about the ongoing economic cycle, however volatile?

Every investor is conditioned to know that crises come and go with remarkable regularity and that recession always gives way to expansion, so what’s the point of following the latest news on green shoots, commodity prices, or the actions and inactions of purchasing managers and policy makers? Although these immediate news items may be important for journalists, politicians and even economists, their impact on the long-term trajectory of profit is negligible – so why should they be of any concern to dominant capitalists and their prescient strategists?

The short answer is that, normally, the latter indeed don’t seem to care. But there are crucial exceptions to this rule. And in order to understand both the exceptions and the rule from which they deviate, we need first to step back and examine the historical record.

The Great Divide

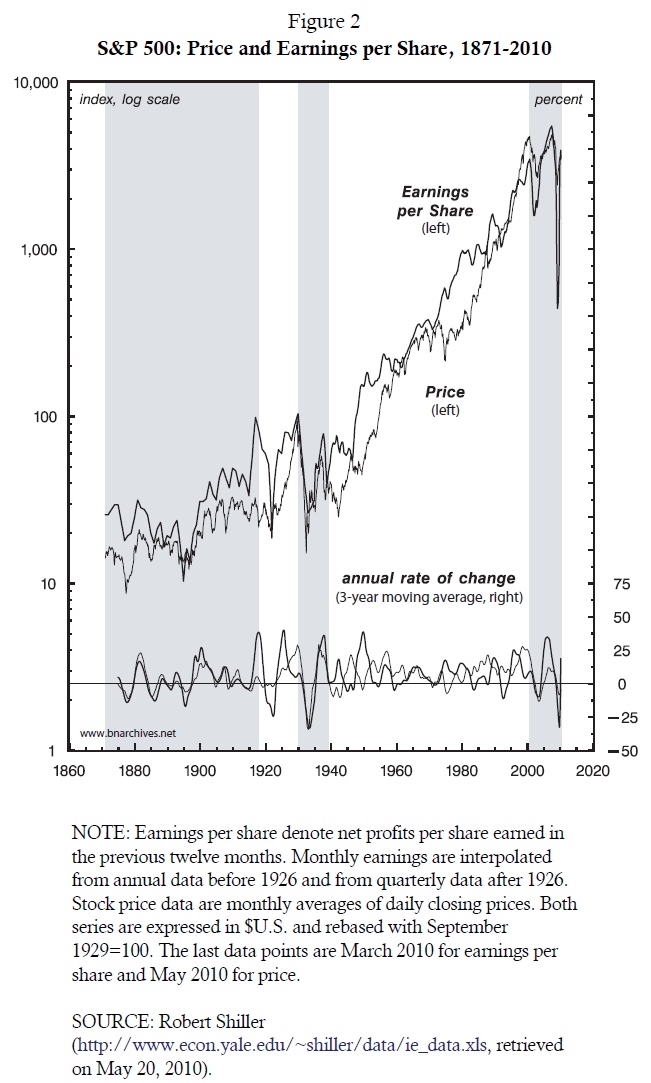

Consider Figure 2, which shows the relationship between the dollar price and dollar earnings per share of the S&P 500, a group representing the largest listed corporations in the United States.[12]

The chart contains two sets of monthly series. The top set, starting in January 1871, displays the actual levels of the series. The price series is calculated as the monthly average of daily closings. The earnings-per-share series is computed in two steps: first by interpolating monthly earnings from annual data (before 1926) and from quarterly data (after 1926); and then by expressing the result as a 12-month moving average. In the chart, both series are normalized, with September 1929=100, and are plotted against the left logarithmic scale to facilitate visual inspection.[13]

The bottom set, beginning in December 1874, shows the respective rates of change of the top series. The series are calculated, first, by computing for each month the percent growth rate relative to the same month a year earlier, and then by smoothing the resulting data as a three-year moving average (so that each observation shows the average annual growth rate of the last 36 months). The resulting series are plotted against the right-hand arithmetic scale.

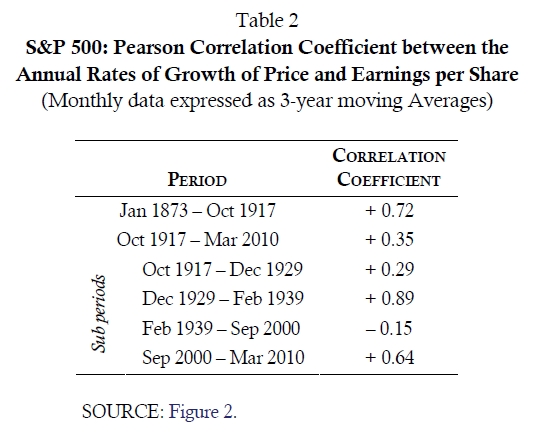

Table 2 shows the Pearson correlation coefficient between the two growth rate series (smoothed as three-year moving averages). The coefficient, which quantifies the co-movement of the series, is measured separately for the periods before and after 1917, as well as for four sub-periods that make up the post-1917 era.[14] The rationale for delineating between the different periods is explained in what follows.

If we take a bird’s-eye view of the entire period from 1871 to 2010, equity prices seem to have moved more or less together with earnings per share. But from a shorter perspective, there is a great divide between the periods before and after the First World War.

During the period ending in 1917, which the figure shades for easier visualization, the correlation between the two series is very high. The fit is evident in the tight co-movement of the levels of price and earnings per share (top series) and even more so in their almost identical rates of change (bottom set). Between 1873 and 1917, the Pearson correlation between the latter series was +0.72, and this tight fit shouldn’t surprise us.[15]

Recall that during that period, forward-looking finance was still in its infancy, and that investors were conditioned to believe that “what you see is what you get.” According to Graham and Dodd, the investment outlook was largely conservative, and most stock owners tended to view common equities as little more than glorified bonds. The main reason for holding equity was dividends – which, at the time, were free of any taxes and accounted, on average, for 70% of corporate profits (compared with less than 50% in the second half of the twentieth century and about 45% since the mid 1970s).[16] There were of course those who bought stocks with an eye to future capital gains, but these were considered “speculators,” not “investors.” For the latter, the main criteria for choosing stocks were: (1) stable dividends; (2) a somewhat higher level of earnings to support such dividends and maintain the company; and (3) a stock price that was solidly backed by so-called tangible assets.[17]

Like the interest on bonds, corporate earnings and dividends were not expected to trend upwards; although investors would have welcomed such an increase, the common premise was that both streams would remain solidly stable. And since the ownership of equities, like the ownership of bonds, was supposed to generate a fairly constant yield, equity prices tended to fluctuate closely with current corporate earnings and dividends – which is more or less what we see in Figure 2.

The second period, though, from 1917 onward, is completely different. For the most part, the fit between price and earnings per share is very loose and often negative: the variations of the series are usually out of sync, the magnitudes of the variations are often very different, and there are extended periods during which the numbers move in opposite directions. The Pearson correlation coefficient for the growth-rate series over the entire post-1917 period (including the anomalous 1930s and 2000s) is a mere +0.35 – less than half of its pre-1917 level.

Of course, theorists of finance don’t consider this decoupling problematic. On the contrary, they see it as a vindication of their forward-looking model, clear evidence that capitalist finance has finally come into its own.

Decoupling Price from Earnings

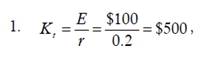

According to the modern forward-looking habitus, investors price an asset by discounting the future profit trend that the asset is expected to generate. In this ritual, the participants set the price of the asset – say a share of Microsoft – as equal to the ratio between what they expect Microsoft’s future profits to be on the one hand and the rate of return they wish those profits to represent on the other. For instance, if investors expect ownership of a Microsoft share to generate a fixed annual profit stream of $100 in perpetuity, and if they want this stream to represent a 20% rate of return, then they would be willing to pay for the share (or demand to be paid) a price of $500. We can represent this computation symbolically, so that:

where Kt is the price of Microsoft’s share in year t, E is the level of annual earnings investors expect Microsoft to generate in perpetuity, and r is the decimal rate of return appropriate for Microsoft.

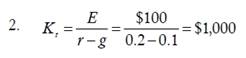

Now, given the common belief that capitalism is a perpetual growth system, it seems only reasonable to expect Microsoft’s annual earnings to flow not at a fixed rate E, but at a rate that grows over time. This expectation could easily be fit into the framework by substituting a higher fixed level of earnings for the exponentially growing one. Alternatively, if we assume, as investors habitually do, that the expected growth of earnings will be maintained indefinitely at a rate g, say 10%, and provided that this growth rate is lower than the discount rate r, Microsoft’s share price can be computed as follows:[18]

In general, the practical pricing process can be far more intricate, but the basic ritual of contrasting expected profits with a discount rate of return is always present.[19] Now, regardless of the merits of this ritual, one thing seems obvious: prices set in this manner should bear little or no relationship to the current level of profit.

There are three reasons for the dissociation. First, since the price reflects the future trend of earnings, and since this trend is affected only marginally, if at all, by present or past earnings, there is no inherent reason why month-to-month fluctuations in current profits should affect stock prices. And that is just for starters. Note that the future earnings trend, by its very nature, cannot be known with certainty and is forever conjectural. For this reason, investors discount not the profits they will earn, but the profits they expect to earn. In the case of Equation 1 above, for example, investors can easily misjudge the perpetual future flow of Microsoft’s earnings per share to be $50 or $400 instead of the eventual $100; this error will in turn cause them to price the company’s stock at $250 or $2000, respectively (=50/0.2 or 400/0.2). Similarly, if investors erroneously predict that Microsoft’s earnings will grow annually by 1% or 19% instead of the eventual 10%, they will misprice its stock at $526 or $10,000, respectively. And since profit expectations are rather open ended and commonly hyped either positively or negatively, the effect is to widen further the disparity between the movement of price on the one hand and of current earnings on the other.

Second, a given level of expected earnings can generate any number of asset prices, depending on the discount rate of return. For instance, if the discount rate in Equation 1 were 10% (rather than 20%), the stock price would double to $1,000 (=$100/0.1). Now, the discount rate changes constantly – partly because of variations in the overall rate of interest and partly in response to changing perceptions of risk specific to the particular equity in question. However, since in and of themselves these changes are unrelated to current earnings, the effect is to reduce the correlation further.

Finally, investors are not always able to follow the rituals of finance with sufficient precision. Regardless of how hard they try, their computations are constantly thrown off, or so we are told, by various market “imperfections,” government “intervention” and other such diseases; and sometimes, particularly when investors get overly excited, the calculations can even become “irrational.” Now, since neither the miscalculations nor the irrationality are correlated with current profits, the result is to loosen the fit even more.

So if we adhere to the scriptures of modern finance, we should expect to see no systematic association between equity prices and current profits. And given that most if not all present-day investors obey the scriptures – including the allowed imperfections and irrationalities – their actions tend to validate the “theory.”

But not always.

Looking Backward

Figure 2 and Table 2 show two clear exceptions to the rule: the first occurred during the 1930s, the second during the 2000s. In both periods, which Figure 2 shades for easier visualization, equity prices moved together – and tightly so – with current earnings. Between 1929 and 1939, the correlation between the respective growth rates of the two series (smoothed as 3-year moving averages) was +0.89, while in the period between 2000 and 2010 it was +0.64. The difference with the rest of the post-1917 period is stark: in the period from 1917 to 1929 the correlation was a much lower +0.29; and in the period from 1939 to 2000 the correlation was –0.15 – which means that the series had very limited co-movement, and that the limited relationship that did exist was actually negative.

Needless to say, the tight positive correlation of the 1930s and the 2000s, reminiscent of a bygone era, is a gross violation of modern forward-looking finance. In fact, the violation is worse than it seems. Note that, despite their name, monthly earnings per share represent profits that were earned not during the current month, but during the previous twelve months. This measurement convention means that, during the 1930s, and again during the 2000s, investors committed a cardinal sin. They priced assets based not on future earnings, and not even on current earnings, but on past earnings!

What caused this sharp departure from conventional practice? Why would investors regress to a backward-looking posture that the scientists of finance tell them is patently “false”? Why would they suddenly abandon their convenient forward-looking ceremony and instead take their cue from the dead past? Why give up the predictive powers of precise positivism in favor of poor historicism?

A naïve observer, unschooled in the rituals of modern finance, may be tempted to blame such regression on the heightened turbulence of the two periods. According to this view, investors are always forward looking. But when rattled by crisis, they become more cautious about the future, and that greater caution causes them to use the movement of current earnings as an indication of heightened future risk. As a result, increases in current earnings mitigate risk perceptions; lower risk perceptions reduce the discount rate; and a lower discount rate raises stock prices (and vice versa).

This type of behavior, although possible, would be entirely inconsistent with the basic ritual of forward-looking asset pricing. First, according to this ritual, the level of caution – or the “risk premium” embedded in the discount rate (r) of Equations 1 and 2 – is a slowly-changing magnitude. It reflects the overall price volatility of the assets – historically as well as with an eye to the future – and as such, it changes very little from year to year. Second, in the manuals of modern finance the “risk premium” pertains to the volatility not of earnings (E), but of prices (Kt). This association means that even if the risk premium were to exhibit large temporal variations, still there would be no reason for such variations to track the ups and downs of current earnings.

So what is behind the two reversals?

Systemic Fear

In our view, the reason is systemic fear.

Systemic fear is a class of its own. It has little to do with the periodic downswings that make capitalists cautious, and it has no connection to the dread and apprehension that regularly puncture their habitual greed. “Business as usual” is always uncertain, and with capitalism constantly in flux, investors are forever fearful about profit and wary about risk: they are concerned that earnings may not rise as quickly as they hope, or that they might fall; that volatility will increase; that interest rates will rise; and so on.

But these fears, no matter how intense, are self-contained. They pertain to the level and pattern of profit, not to its existence. They do not impinge on the normality of profit – i.e., on the belief that assets have a “natural” tendency to grow and that capitalists have the power and right to enforce and appropriate such expansion. And most crucially, they reflect the belief that expected profits, whether high or low, could always be priced to their present value. Regardless of the market’s ups and downs, the underlying assumption is that the capitalization process itself – the ritual that creorders modern capitalism and anchors its dominant ideology – will remain intact.

Occasionally, though, there arises a very different and far deeper type of fear: the terrifying thought that the entity of profit – and, worse still, the very institution of capitalization on which the entire capitalist megamachine stands – might cease to exist.[20] This latter fear is associated with systemic crisis – that is, with periods during which the very future of capitalism is put into question. It is what Hegel meant when he spoke of the bondsman’s “fear of death”:

For this consciousness [of the capitalist bound to the steering wheel of a megamachine gone wild] was not in peril and fear for this element or that [such as falling profit or rising volatility], nor for this or that moment of time [like a sharp market correction or a declaration of war], it was afraid for its entire being; it felt the fear of death, the sovereign master [the ultimate wrath of the ruled]. It has been in that experience melted to its inmost soul, has trembled throughout its every fibre, and all that was fixed and steadfast has quaked within it [will capitalism survive?]. (Hegel 1807: 237)

The first time capitalists were gripped by such systemic terror was during the Great Depression of the 1930s. The second time is during the present crisis, a protracted turbulence that started in the early 2000s and is still ongoing.

The 1930s

Let’s examine each of these periods more closely, beginning with the 1930s.

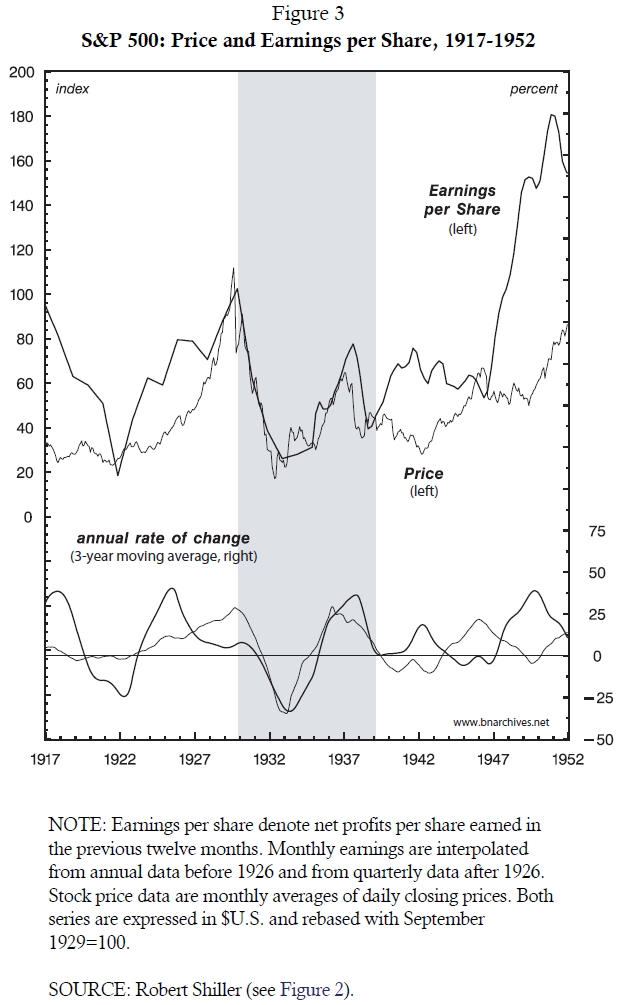

Figure 3 “magnifies” the data from Figure 2. It focuses specifically on the period from the late 1910s to the early 1950s, with the shaded area denoting the period of systemic crisis. For ease of comparison, the two top series are rebased with October 1929=100 and plotted against an arithmetic left scale. The rate-of-growth series, as before, are plotted against the arithmetic right scale.

The data show that, after the First World War and during the happy 1920s, stock prices moved rather independently of earnings, exactly as the “New-Era Theory” decreed. But once the stock market crashed in 1929 and the Great Depression began, the “New-Era Theory” broke down: the two series, instead of moving independently of each other, suddenly converged and remained tightly locked for nearly a decade.

Both series fell in tandem from 1930 to 1932, and then rose in tandem from 1933 to 1936 – charting what initially looked like a V-shaped recovery. But the hopeful V soon became a disheartening W. In 1937, a new downturn began, and the two series, which briefly decoupled, again converged in a free fall. It was only in 1939, after a decade of frustration, that the two series again diverged and that the “New-Era” theorists could breathe a sigh of relief.

The political-economic background of the period requires little elaboration. During much of the 1930s, the United States, along with the rest of the world, was mired in a systemic crisis. The very existence of the capitalist mode of power was at stake, with liberalism fighting for its life against both communism and fascism. The dominant ideology suffered a major blow. The “free market” didn’t seem to be working, and with laissez faire theories in deep disarray, the rulers were no longer confident in the obedience of the ruled. Few felt certain that capitalism would survive, and many – including some of the system’s leading advocates – feared its imminent demise.

In this context, the “future trend of earnings” was no longer a very meaningful concept, and there was little point in extrapolating, let alone quantifying, its growth rate. Furthermore, the very institution of capitalization was put into question, so even if future earnings could somehow be predicted, it didn’t seem certain that future ownership claims on these earnings could be priced and transacted.

There was no anchor ahead. All that was solid melted into air, all that was holy was profaned. And so, in despair, forward-looking investors found themselves latching onto the only “real” thing they could see: the past. Like the Aymara Indians of South America, they suddenly realized that the future was behind them.[21] Nominally, their assets still represented a claim over the future; but the only way to price that future was to look backward, to what the assets had already earned.

The pricing anomaly ended in 1939. Suddenly, the disorder dissipated, optimism re-emerged and history could again be forgotten. The onset of the Second World War and the boom that ensued sent profits soaring (they doubled in less than two years). And the capitalists, cajoled by the apparent efficacy of the new welfare-warfare state, regained their systemic confidence. They abandoned the stale past, returned to their forward-looking rituals and resumed the discounting of expected future earnings. Within two years, the stock market was down 25%, but this decline was no longer symptomatic of systemic fear. On the contrary, it was evidence that capitalism had survived and that capitalists could fearlessly practice their capitalization rituals.

The 2000s

This situation lasted for sixty years. During that period, capitalism went through many ups and downs, and there was the occasional scare that sent markets reeling. But none of the jolts was serious enough to evoke the Hegelian fear of death. At no point was the existence of the system itself in doubt. It was business as usual, with greed and fear easily incorporated into future earnings projections and risk calculations. The financial model seemed to work like clockwork.

But in 2000, the machine stopped. The threat of a new systemic crisis suddenly loomed large, and the specter of backward-looking pricing, having been dormant for decades, returned to haunt the markets.

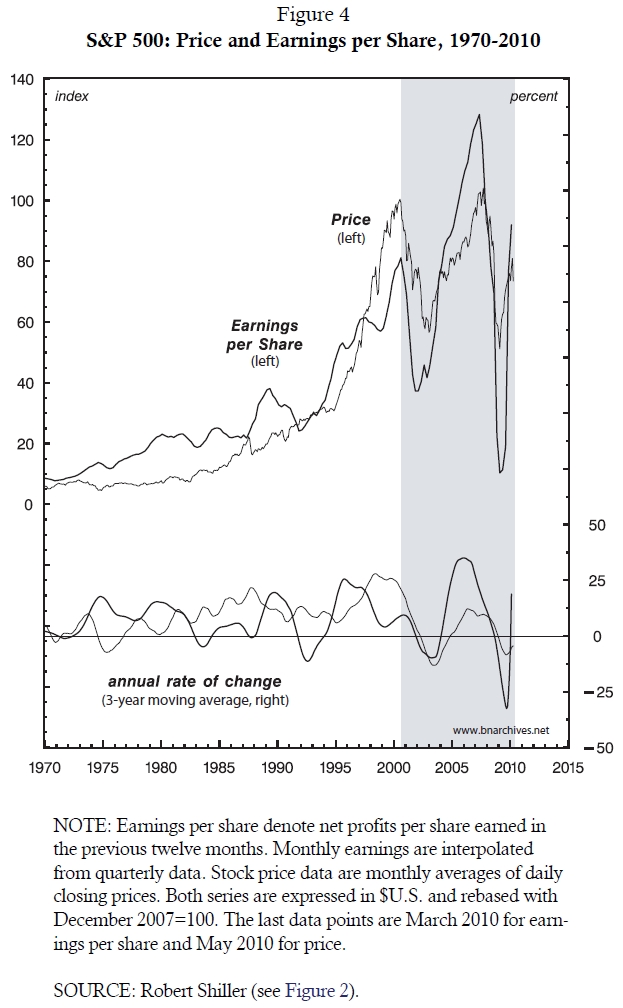

Figure 4 displays price and earnings per share data from 1970 to the present, with the shaded area denoting a period of systemic crisis. The two top series, denoting levels, are rebased with December 2007=100 and graphed against the left arithmetic scale. The bottom series express the annual rates of change (smoothed as 3-year moving averages) and are plotted against the right arithmetic scale.

As the data in Figure 2 and Figure 4 show, from 1939 to the early 2000s, both price and earnings per share trended upwards. But in line with the “New-Era Theory” – which by now had become mainstream finance – the short-term correlation between them remained loose and indeed negative (see Table 2). During that long stretch, earnings went through several sharp declines. For instance, during the end-of-communism crisis of 1989-1991 they dropped 37%, and following the emerging markets scare of 1997-1998 they fell 6% – yet in both cases stock prices continued to soar. And conversely, in 1972-1974 earnings increased by 42% while prices dropped by 43%; similarly, at the end of 1987 earnings increased by 14% while prices dropped by 27%. All in all, then, investors seemed perfectly happy to obey the theory. Throughout the period, they ignored the ephemeral present in favor of the eternal future.

But in 2000, they suddenly lost their forward-looking vision, and they haven’t regained it since. Over the past decade, earnings have experienced two very violent swings; yet stock prices, instead of remaining impartial to the immediate gyrations of the earnings cycle, have traced it, and rather tightly: the correlation coefficient between the rates of growth series, smoothed as 3-years moving averages, jumped to +0.64, up from to –0.15 in the preceding six decades.

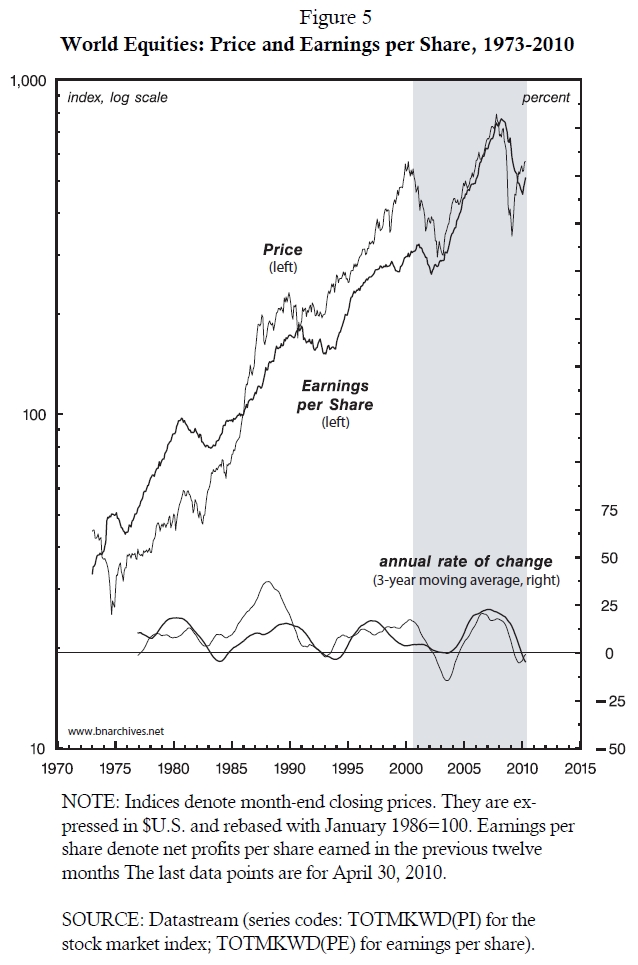

A fairly similar picture arises at the global level. Figure 5 shows price and earnings per share for the Datastream world equity index, covering the period between January 1973 and April 2010 (there are no prior data). The top series, plotted against the left logarithmic scale, show levels and are rebased with January 1986=100. The bottom series show the annual rates of change, smoothed as a three-year moving averages, and are plotted against the right arithmetic scale. As before, the shaded area denotes a period of systemic crisis.

Because the world aggregate is far broader than the U.S. one, reflecting many different markets that often move through different phases and that are subject to different conditions, one would expect the correlation between the two series to be looser throughout. But it is not. For the period from January 1974 to August 2000, the Pearson correlation coefficient between the two rate-of-growth series, smoothed as 3-year moving average, is –0.16, which is similar to that of the U.S. And the coefficient for the subsequent period is +0.48 – lower than U.S.’s +0.64, but still far too high for the forward-looking ritual.

Is Capitalization Approaching a Glass Ceiling?

Let’s examine the experience of the past decade more closely, beginning with the first market cycle, which started to decline in 2000, troughed in 2003 and peaked in 2008 (given the similar statistical patterns in Figure 4 and Figure 5, our discussion refers to the former figure only). The 2000 “dotcom” crash and the demise of the “new economy,” together with the 2001 collapse of the Twin Towers and the onset of the “infinite war on terror,” signaled the beginning of a new era of uncertainty. Analysts started to debate the end of the “Washington Consensus,” strategists deliberated over the decline of the “American Empire,” and culturalists lamented the death of the “global village.”

It is true that, initially, nobody was seriously contemplating the “end of capitalism.” But capitalists nonetheless started to grow wary. This didn’t feel like yet another “crisis as usual,” and the long-term trajectory of future profits – which in previous decades had appeared neatly bounded and relatively easy to project – suddenly looked murky. And so, once again, capitalists found themselves with their backs to the future. As we can see in Figure 4, instead of projecting the earning trend looking forward, they began to watch earnings as they unfolded and to discount their past declines.

By the middle of 2002, the earnings crisis finally appeared to have ended, and in early 2003 the stock market bottomed. Profits staged a massive, V‑shaped recovery and, over the next five years, rose by nearly 350%. And yet, despite the surge, capitalists still found the future hard to envisage. The earnings boom certainly was real enough – but so were its limits.

These limits become visible when we take a bird’s eye view of the postwar period. During that period, U.S. market capitalization was fueled by a highly favorable combination of several power processes.[22] First, after the Great Depression, capitalists managed to force a systematic redistribution in their favor, seeing the combined share of their pretax profit and interest in national income rise from about 12% in the 1930s and 1940s to roughly 17% in the 2000s. Second, they also succeeded in pushing down the effective corporate tax rate – from 55% in the 1940s to less than 30% in the 2000s – a decline that caused their after-tax corporate earnings to increase even further. Third, the broader consolidation of power relations and the establishment of capital-friendly regulations and macro stabilization policies helped them reduce earning volatility – and, by extension, their own perceptions of risk. This decline in perceived risk, along with the general fall in interest rates since the late 1970s, lowered the rate at which they discount their expected earnings, thereby boosting their present value even more.

These power processes all had the same impact on the stock market: they pushed it up. The effect of income redistribution and falling corporate taxes convinced capitalists that net profits would continue to rise much faster than national income, while falling risk perception along with the drop in interest rates over the past thirty years allowed them to re-price this steep earning trend at ever lower discount rates. The net consequence was that the overall stock market capitalization rose more than four times faster than the gross national income: it soared from $167 billion in 1952 to $20.3 trillion in 2007 – a 127-fold increase – compared with a mere 39-fold increase in dollar value of gross national income, which grew from $312 billion to $12.4 trillion.[23] [24]

The trouble was that, by the early 2000s, after half a century in overdrive, these power processes have already run much of their course, making future increases in stock prices more difficult to achieve. Capitalism is inherently conflictual, so power is always imposed against opposition. This built-in conflict means that from a certain point onward, there tends to be a positive relationship between the existing level of capitalist power on the one hand, and the force that needs to be exerted in order to further increase that power on the other. Thus, the higher the income inequality, the harder it is to make it more unequal; the lower the corporate tax rate, the harder it is to cut it further; the smaller the volatility of earnings, the harder it is to stabilize them further; and the lower the rate of interest, the harder it is to see it fall further.

The exhaustion of these redistributional/conflictual fuels left the stock market at the mercy of aggregate growth – and yet the “real economy” too seemed to be running into the sand.[25] Expressed in purchasing power parity, annual GDP growth in the United States has drifted downwards, from 3.6% in the period from 1950 to 1975 to 3.1% since then, while world GDP growth dropped from 4.7% to 3.5%.[26] Since the late 1990s, official growth measures seemed to have recovered, leading capitalists to hype the unlimited potential of “high technology” and the “knowledge economy,” along with the fabulous riches promised by rapid urbanization in the so-called “emerging markets.” But by the early 2000s, these hopes were increasingly spoiled by new doomsday scenarios, ranging from “peak oil” and “climate tipping” to “runaway pandemics” and “environmental devastation” (scenarios that we consider later in the paper).

The fact that redistributional difficulties tend to arise together with overall stagnation is no accident. In order to redistribute income and assets in their favor, rulers need to exert their power on the rest of society; to exert such power, they have to strategically limit and partly sabotage the well-being of the underlying population; and this strategic sabotage tends to appear at the aggregate level in the form of stagnation.[27] The rulers themselves, because of their social position, cannot comprehend, let alone accept, this necessity, and their dominant dogmas and ideologies hide and deny it. But the historical evidence, particularly during acute crises, proves it time and again: unable to see the contradiction, the rulers attempt to alleviate the general malaise as well as to keep their redistributional power intact; but because their power depends on the sabotage they cause, this attempt invariably fails.

In light of this discussion, and given the current convergence of redistributional and aggregate limits, can we say that the capitalist mode of power is approaching a glass ceiling? During the early 2000s, few capitalists were expressing the question in such stark terms; but the menacing possibility was certainly lurking in the background, and with the future looking disheartening at best, most preferred to keep their eyes on the immediate past. Share prices started to rise only in October 2002, a full six months after the earnings upswing began, and for the next five years they increased in tandem with profits (albeit at a much lower rate).

And then came the “subprime crisis,” and all hell broke loose.

Is the Dominant Ideology Broken?

As Figure 4 shows, between their June 2007 peak and their May 2009 bottom, earnings fell by 91% – a decline greater than the 75% collapse experienced during the first three years of the Great Depression. If capitalism were here to stay, this must have been the mother of all investment opportunities: with profits bound to rebound back to their long-term trend, their rise was sure to be spectacular – as were the gains to investors loyal to the forward-looking ritual. But few seemed convinced. And, so, instead of anticipating the Galtonian reversion to trend, share prices continued to slide, closely following the footsteps of current earnings.

Given that the bear market, measured in rates of change, was approaching historical lows, and since such bottoms had previously always been followed by major upswings, many forward-looking strategists – from permanent bull Barton Biggs, to Wizard of Omaha Warren Buffet, to doom-and-gloom Martin Wolf – were advising their followers to fasten their seat belts in preparation for an imminent takeoff.[28] And in early 2009 they were finally vindicated.

But the rebound had to do neither with the advice of analysts nor with the prescience of capitalists. The real trigger was earnings. Recall that, by now, investors had lost their belief in the inevitable, at least for the time being, and that instead of looking forward to eternity they kept staring at the past. Everyone was glued to the earning cycle, anxiously waiting for it to find a bottom. And, sure enough, it was only after profits finally started to increase that stock prices began to rise.[29] By April 2010, the market was up 60%; but as with the decline, the increase, too, merely traced the path of earnings. Given the thrust of the profit up-cycle, though, with earnings having risen more than nine-fold from their near-zero level at the 2008 bottom, the question arises again: why are investors still behaving as if they doubt that the upswing is real, not to say sustainable?

In our view, the answer is that the crisis of the late 2000s reintroduced an additional and far deeper form of fear. During the early 2000s, the concern was largely practical: the stock market appeared to be running out of fuel, and the main fear, however fuzzy, was that the level of capitalization may have been approaching a glass ceiling. But since the late 2000s, the very ideology of capitalization has been put into question: the capitalist class seems to have lost confidence in its own theories and rituals – and, therefore, in its ability to rule.

“Uncertainty is the only certain thing in this crisis,” bemoan the editors of the Financial Times. As of today, nobody knows what is going to happen:

[A] dense fog of confusion has . . . descended, obscuring where we are – falling fast, slowly, bumping along the bottom, or finally turning the corner. . . . Economies are behaving unpredictably and will continue to do so. The instability is both cause and consequence of the great uncertainty that has been spreading out from the financial markets. Fearful and confused, people react erratically to changing news, reinforcing confused market behavour. It doesn’t help that our economic theories were constructed for a different world. Most models depict economies close to equilibrium. . . . And unlike what most models assume, prices are not properly clearing all markets. . . . [etc. etc.] (Editors 2009)

This sentiment is echoed in numerous publications and speeches, academic and popular. “The whole intellectual edifice . . . collapsed in the summer of last year,” concedes former Fed Chairman Alan Greenspan (Andrews 2008). “Our world is broken – and I honestly don’t know what is going to replace it,” grieves Bernie Sucher of Merrill Lynch. “[T]he pillars of faith on which this new financial capitalism were built have all but collapsed,” observes Gillian Tett in a special Financial Times series on the future of capitalism, and that collapse, she concludes, “has left everyone from finance minister or central banker to small investor or pension holder bereft of an intellectual compass, dazed and confused (Tett 2009). And with no intellectual compass to rely on, confesses Bank of England Governor Mervyn King, “judging the balance of influences on the economy” becomes “extraordinary difficult” (Editors 2009).

Financial crisis, argues György Lukács, threatens the foundations of the capitalist regime. The ruling class loses its self-confidence and begins to substitute ad-hoc excuses for natural-state-of-things theories. And as the ideological glue that holds the regime together weakens, class conflict becomes visible through the cracks of universal rhetoric, while the threat of naked force suddenly looms large behind the front window of tolerance.

The present stage of the crisis fits this pattern, and so do the justifications. Some, like Alan Greenspan, blame it all on humans failing to live up to their true nature:

All the sophisticated mathematics and computer wizardry essentially rested on one central premise: that the enlightened self-interest of owners and managers of financial institutions would lead them to maintain a sufficient buffer against insolvency by actively monitoring their firm’s capital and risk position. (Greenspan 2009).

[T]hose of us who have looked to the self-interest of lending institutions to protect shareholder’s equity (myself especially) are in a state of shocked disbelief. Such counterparty surveillance is a central pillar of our financial markets’ state of balance. If it fails, as occurred this year, market stability is undermined. (U.S. Congress 2008)

Other observers, like Oxford economist John Kay, see the fault not at the level of the individual, but of the system as a whole. When the Queen of England wondered why “the credit crisis and its evolution were not predicted” by the experts, her “loyal subject” (as Kay names himself), quickly jumped to his colleagues’ defense. National economies, financial markets and businesses, he explained, are simply too complex, dynamic and non-linear, and these systemic intricacies turn prediction into a “wild goose chase” (Kay 2008).

And then there are those, like financial commentator Gideon Rachman, for whom the problem is largely temporary. The economists, Rachman suggests, have actually made great strides in understanding how the economy works. But from time to time the delicate machine gets infected by a “new type of economic virus,” and we need to be a bit patient until the economists discover the cure (Rachman 2009).

By 2010, though, it seems that the virus continues to elude the pundits. The threat of default has spread from business enterprise to sovereign governments, with countries like Iceland, Dubai, Greece and who-knows-who-is-next flirting with bankruptcy. Participants at a special conference hosted by Soros’ Institute for New Economic Thinking at Kings College, including five Nobel-winning economists, expressed grave concern that “many investors now find it hard to judge the ‘real’ riskiness of sovereign debt.” Gillian Tett conveys the atmosphere of theoretical bewilderment and ideological anxiety:

Three years ago, it seemed inconceivable that a country such as Greece would be allowed to default, or exit the eurozone. But back then it seemed equally hard to imagine that Lehman Brothers might fail. Now that Lehman has gone, who knows what the worst-case scenario might be? Could the eurozone break up? Could Greece default? What might happen to other debt-laden nations, such as the US, if the worst case scenario occurred? The one thing that is clear is that the answers to those questions now depend as much on culture and politics as on macro-economics. . . . In this new world of sovereign risk, what really matters is a set of issues that cannot be plugged into a spreadsheet. The old compass no longer works. (Tett 2010)

The predicament is so serious that even the know-all “market” – the collective brain of the capitalist class – has become disoriented. According to Martin Wolf, chief economics commentator at the Financial Times, the markets “don’t know what to fear: will it end up in deflation, default, inflation, financial shocks, or all of these?” “Markets are unpredictable,” he informs his son, “like children. . . .” And when the youngster asks “So what’s going to happen next?” the elder, who is usually able to answer questions that most people cannot even ask, replies: “If I knew that, I wouldn’t be a mere economic journalist. . . .” (Wolf 2010)

Mene, Mene, Tekel, and Parsin: Is Capitalism Heading for Systemic Collapse?

The decade-long breakdown of capitalization is no fluke. The fact that for ten years now capitalists have been pricing equities based on past profit betrays deep distress. Their fear now is not only that the level of capitalization may be bumping into a glass ceiling; it is also that the very ritual of capitalization – the universal crystal ball through which they have been “seeing” the future for nearly a century – may be giving them awfully wrong signals. And when the future looks bleak, and the dominant ideology appears opaque if not misleading, there arises the specter of systemic fear.

Given the foregoing, the obvious question to ask is: does systemic fear signal the imminent collapse of capitalism?

This is by no means an easy question to answer. The difficulty is threefold. First, systemic fear – in capitalism as in other modes of power – is rare and therefore difficult to generalize about. Second, although much has been written about previous episodes of social collapse, it is unclear how much of it applies to the capitalist mode of power. Third and finally, systemic fear and systemic collapse are deeply intertwined in ways that may not be easy to disentangle. Nonetheless, given that we are dealing with the very existence of capitalism, discussing these questions – even speculatively, as we do in the remainder of the paper – seems appropriate.

To start with, we need to distinguish between gradual decline and final collapse. The slow weakening of a mode of power – for instance, the prolonged descent of European feudalism, or the progressive decay of Soviet Union – can happen for many different reasons, stretched over a long period of time. But, in our view, for a mode of power to finally implode, these reasons must be complemented by the loss of confidence in obedience. When the ruling class is no longer certain of its ability to govern, it becomes indecisive; indecision inhibits ruthlessness; lack of ruthlessness fuels opposition; and effective opposition is the other side of disintegrating rule. It is only at that point, when it becomes obvious that the ruling class, benumbed by systemic fear, has lost control, that final collapse becomes possible.

Systemic fear often appears when it is least expected. On the surface, the mode of power seems unassailable, the rulers hubristic and the underlying population submissive. But under the surface, redistribution requires greater sabotage and larger doses of force, and as social stress builds up, the stage is set for the crucial inversion. One such drama is narrated in the biblical story of Babylon. The last Babylonian emperor, Belshazzar, celebrates the height of his power at a sacred royal feast when, suddenly, a mysterious hand comes out to put an indecipherable writing on his wall and sudden terror in his heart: “the king's color changed, and his thoughts alarmed him; his limbs gave way, and his knees knocked together” (Book of Daniel, Ch. 5: Verse 6). None of his enchanters, Chaldeans or astrologers can read the strange writing. Only one pundit – a foreign analyst named Daniel – knows what it means. “Mene, Mene, Tekel, and Parsin,” he reads the menacing omen: “MENE, God has numbered the days of your kingdom and brought it to an end; TEKEL, you have been weighed in the balances and found wanting; PERES, your kingdom is divided and given to the Medes and Persians” (Ch. 5, Verses 24-28). That very night, the king is slain, and his empire collapses.

The socio-ecological collapse of Easter Island, whose final implosion occurred sometime during the seventeenth century, was also triggered by hubris-cum-fear. In a last-ditch effort to stave off their decline, the island’s rulers engaged in a competitive orgy of statue building. The likely purpose was to bolster their status and self confidence; but since statue building did nothing to alter the social structure, the only consequence was a hastening of the destruction of their environment and the demise of their mode of power. Soon after, the rulers and priests fled, the island sank into civil war, a new religion came into being, and the giant moai statues – the chief symbol of the rulers’ power – were systemically toppled and broken (Diamond 2005: Ch. 2).

A similar story can be told of the Soviet Union. Shortly before its collapse, General Secretary Mikhail Gorbachev asserted that Perestroika was a “revolution from above,” and that, “Naturally, we [read the country’s rulers] have no intention to change Soviet power; we will not depart from its basic principles” (Gorbachev 1987: 30-31). But signs of deep fear were there for everyone to see – from the Party’s admission that administered prices distorted the law of value (whatever that “law” means) to its apprehension that central planning could no longer deliver growth to keep the mode of power together. “We only thought we were in the saddle,” confessed Gorbachev, “while the actual situation that was arising was one that Lenin warned against: the automobile was not going where the one at the steering wheel thought it was going” (p. 18). Two years later, the Soviet Union was no more.

The collapse of a mode of power is always underwritten by its own historical circumstances. But as these and numerous other examples suggest, it is the rulers’ systemic fear and loss of confidence that makes those circumstances – whatever they are – culminate in an abrupt crash. In and of themselves, fear and loss of confidence are rarely if ever sufficient to set off the implosion; but they are always necessary, and that necessity makes them important to analyze.

Complex Systems and Time Transformers

As noted, systemic fear is not unique to capitalism. But in our opinion, the likelihood of systemic fear turning gradual decline into rapid collapse is much greater in capitalism than in any prior mode of power. There are two related reasons for this claim. First, modern capitalism is much more “complex” than earlier modes of power, and that complexity makes it susceptible to implosion.[30] Second, unlike other modes of power, the ritual of capitalization acts as a “time transformer”: it condenses the long future into the singular present, and that reduction can turn capitalist expectations – particularly during times of systemic fear – into an immediate reality. Let’s consider these reasons more closely.

Most of the time, the high complexity of capitalism allows it to quell and encompass limited challenges to power and local breakdowns of rule. But the agility and flexibility of capitalism have limits, and when these limits are crossed, complexity can turn “against the system.” At that point, internal challenge, external attack and ecological calamity, instead of being counteracted and absorbed, get amplified. And as the reverberations spread, the system doesn’t simply weaken; it implodes.

This type of scenario, in which complexity facilitates collapse, is spelled out in David Korowicz’s Tipping Point (2010). His argument, like others in this genre, builds mainly on standard “real-growth” economics, of which we are critical, and it offers very little discussion of the power relations that we emphasize. But his analysis of complexity could easily be extended to a broader power perspective and therefore is worth exploring in some detail.

Korowicz claims that the imminent peaking of oil production is a “tipping point” – a threshold beyond which capitalist civilization will not simply decline, but rapidly disintegrate. His initial premises are similar to those of most peak-oil analysts: (1) capitalism requires continuous economic growth; (2) ongoing economic growth necessitates ever-increasing energy inputs; (3) the key energy input – oil and its derivatives – has no immediate substitutes; and (4) once the production of oil – and of fossil fuels more generally – peaks and starts to decline, economic growth and the capitalism that is based on it must follow suit. The disagreement is over what follows. According to most analysts, the systemic consequences of peak oil are likely to be gradual: the optimists envisage an unstable period during which the piecemeal development of renewable energy sources and energy-saving techniques substitutes for the decline of fossil fuels, while the pessimists see a drawn-out process of deindustrialization and social decline. For Korowicz, though, these gradual scripts all suffer from a crucial omission: they ignore the operational fabric of capitalism, and that oversight leads them to the wrong conclusion.

Global production, he says, is mediated through highly complex and deeply intertwined critical infrastructures – including money, trade, transportation, communications, water, and electricity, among others. The operation of these integrated infrastructures rests on and presupposes the ongoing expansion of credit and debt. And that expansion is possible only because investors believe that the additional credit and debt will be serviced and ultimately repaid. According to Korowicz, though, this latter belief – and therefore the entire operational fabric that rests on it – can only hold in a growing economy. And here lies the trap.

Once humanity passes the threshold of peak oil, economic growth must turn negative – and, at that point, the assumption of ever-growing credit and debt breaks down. Investors suddenly realize that, looking forward, their assets have an inherently negative yield. And since this realization inverts the basis on which the whole society operates, the result is not a gradual decline but sudden collapse. The first to tank are the equity and debt markets; these are followed by mutually reinforcing reverberations and the eventual rupture of money, trade, investment, communications and other critical infrastructures; and the process is then sealed by conflict, war and die-off (as argued for example by Jay Hanson).[31]

Note that the collapse here begins with a seemingly inconspicuous change. Roughly half of the oil is still under ground, and its extraction rate is still positive. But that rate, instead of accelerating, is now decelerating, and this deceleration is enough to set the social avalanche in motion. Because the operational fabric of capitalism is highly complex and mediated by forward-looking debt and credit, the mere realization that this is the beginning of a long, secular decline in oil output causes a contiguous implosion of the entire society.

Korowicz’s collapse scenario focuses on peak oil, but its dynamics can be readily generalized. Regardless of whether the capitalist of mode of power is expanding, declining or collapsing, the forces that drive it – social as well as ecological – are always mediated through the ritual of capitalization. This ritual is unlike any the world has ever known. It endows every member of society with a miraculous power previously reserved to wizards, oracles and prophets: the ability to “transform” the future into the present. By discounting expected future earnings and risk, capitalization encapsulates their complex social and ecological causes into a single value – and then sends it back to the present.

Under normal circumstances, this all-encompassing “time transformer” enables capitalists to mange their fears and exert their power in ways that previous rulers could only have dreamed of. But the ritual also has a dark side, a lightning-like menace that prior rulers could not even fathom. As long as capitalists take their mode of power for granted, capitalization makes their power appear unassailable. But when they begin to doubt their own ability to rule, any serious future threat – from peak oil and climate change to the inability to further redistribute income and reduce earning volatility – can be time-transformed into an immediate collapse.

Warning Signs?

This threat perhaps explains, at least in part, the growing literature on systemic collapse: Why do complex systems implode? Is the disintegration patterned? And if so, is there a clear “writing on the wall”? Can we find warning signs to help us anticipate and perhaps prevent the calamity?[32] Analytical and empirical modeling of natural phenomena suggests that “collapse” – formally defined as a rapid or quantum-like shift of the system from a high to a low level of complexity – tends to have fairly clear patterns. Moreover, very often collapse is preceded by quantitative warning signs: the key variables of the system may begin to flicker between alternate states; they may become slow to recover from small perturbations; they may exhibit a surge of path dependency in the form of rising autocorrelation; and they may display rising cross-correlations between different components of the system. Most remarkably, through, these warnings signs seem to be generic – i.e., they tend to occur independently of the concrete features of the system in question.[33]

However, identifying similar warnings signs in complex social system is far more difficult. There are two reasons for this difficulty. First, until capitalism, most modes of power generated very little quantitative information, so it is hard to see how universal warnings signs can be constructed in the first place. Second, unlike natural systems, society contains an inescapable entanglement: its actual trajectory is inextricably bound up with its dominant dogmas, ideologies and theories.[34] Under normal circumstances, the latter seems useful in describing and even “predicting” the former. But as the system approaches collapse, so do its leading dogmas, ideologies and theories – and at that point, prediction and even description based on these dogmas, ideologies and theories becomes difficult if not impossible. Let’s unzip these reasons, staring with quantities.

Quantification