Preamble

Over the past few years, we have written a series of articles about the global crisis.1 These papers try to break the conventional constrains of liberalism and Marxism, examining the crisis from the new theoretical viewpoint of capital as power. Capitalists and corporations, we argue, are driven not to maximize profit, but to ‘beat the average’ and increase their differential power. In this approach, the redistribution of income and assets is not a ‘societal’ side effect of the economy, but the central conflict that propels modern capitalism. And the main weapon in this struggle, we claim, is not investment and growth, but what the American political economist Thorstein Veblen called ‘strategic sabotage’ – the restrictions, limitations, hazards and pains that capitalists impose on the rest of society in order to sustain and augment their differential power.

Now, until 2011, distribution was a non-issue. Save for a few ivory-tower experts and justice-seeking activists, nobody spoke about it. It received little media coverage, let alone headlines, and elicited no meaningful debate. But with the global crisis lingering and upward redistribution continuing unfazed, the Occupy slogan ‘We are the 99 percent’ has finally gained traction. Suddenly, inequality and the excesses of the Top 1% are hot commodities, broadcast, discussed and written about all over the media.

The debate itself, though, remains largely conservative. The protest movements succeeded in putting distribution on the political table, but they haven’t figured how to take this achievement forward. So far, they have produced no new policy template, let alone a new theoretical framework, and this vacuum has left the political centre-stage open for policymakers, leading academics and Noble Laureates to recycle their worn-out platitudes.

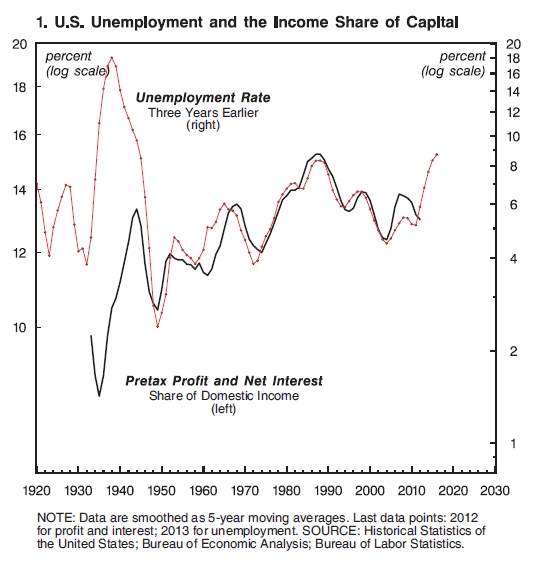

In order to buck this trend, however symbolically, we wrote a short, pointy article titled ‘Why Capitalists Do Not Want Recovery, and What That Means for America’. The paper delivered a clear massage, backed by two highly contrarian graphs. The graphs showed that, contrary to the conventional creed, both mainstream and heterodox, accumulation thrives on crisis and sabotage. They demonstrated that, over the past century, the capitalist share of U.S. domestic income and the income share of the Top 1% have been tightly correlated not with growth and prosperity, but with unemployment and stagnation.

Looking for a publisher, we started with the two bastions of American liberalism: The New York Times and the Los Angeles Times. We sent them the article, free of charge, but neither replied. We then moved to England, emailing the paper to the Guardian. Again, silence. Our last stop was the London Review of Books. This time we got a polite response, stating that the article ‘isn’t quite right for us’.

Clearly, the enlightened capitalist press wasn’t particularly keen on showcasing the power basis of accumulation. The article was too counterintuitive for readers to digest and too politically incorrect for advertisers to subsidize. It suggested that upward redistribution and its associated sabotage were not unfortunate manifestations of ‘social injustice’, but the twin drivers of capital accumulation. And that message, apparently, was unpublishable.

There was no point banging our heads against the wall. It was time to head elsewhere. And since salvation always comes from the East, we turned to the emerging market of India. Unlike in the United States and England, capitalism in India is still being debated, including in the mainstream press. So we submitted the article to Frontline, a fortnightly magazine published by The Hindu Group. And to our pleasant surprise, it was promptly accepted, as is, and appeared in the very next issue (Nitzan and Bichler 2014).2 One must admit that globalization does have its upsides.

The Letter

- Scarcely had a day passed from the article’s publication that we got an angry email from an asset manager whom we’ll call ‘Mr. X’. Mr. X is an enlightened capitalist, and reading our piece had set him on fire. Our article, he protested, was ‘terribly flawed’. It ‘failed miserably’ in understanding capitalism, and its allegation that capitalists do not want recovery is doing ‘tremendous harm’:

-

Jonathan,

Your most recent paper is terribly flawed. Like many political and economic analysts you have failed miserably in your understanding of capitalism. You have also made the classic mistake of confusing correlation for causation.

As I read your paper I sit in between sessions at an impact investing conference filled with ‘capitalists’. Are they interested in ‘beating averages’ and ‘increasing power over others’? No not at all. The focus here is improving income equality, improving the environment, and greatly reducing poverty and hunger.

I sincerely believe that there is almost no field in higher education that has completely screwed up ordinarily bright minds like the field of economics.

Capitalism is not a zero sum game where for one group to gain another must lose. In fact it is quite the opposite where for mutual exchange to flourish both counterparites must benefit.

Capitalism is so misused a term today (as is fascism, socialism, and communism) that nobody seems to understand what it means.

The primary cause of redistribution is through corporate statism not capitalism. With your continual focus on differential power I think it is paramount that you make this distinction in your work lest you confuse the next generation of students.

As I read your papers I still see no mention of the effects of private banks and the government central bank monopolizing the creation of credit. When power and redistribution are taking place this is the root cause. Redistribution is easily facilitated, especially during a crisis, as those in line closest to the credit creation benefit directly at the expense of the rest of society. Not surprisingly those first in line are banks, investment houses, and large corporations, and they all have heavy government influence. You are correct that ‘what is good for GM is good for America’ is completely hollow. To be clear capitalism does not support this. This is not capitalism and the executives of these firms that rely on special favors, laws, and bail outs by governments are not capitalists.

Real capitalists fail, and usually quite often. That is the beauty of a capitalist system where capital decomposition is just as important as it is in nature. Furthermore many capitalists are perfectly happy in homeostasis i.e. they do not desire nor pursue constant economic growth. As an easy example look at the thousands of restaurant owners that simply own one restaurant, are satisfied with the living they make from that, and have no desire or ambition to be a McDonalds. Even when economic growth is pursued, that is often stimulated by a need to retain purchasing power. This is often the cause for constant seeking of returns on investment. If purchasing power remained consistent instead of being diluted by false credit and money supply creation the demand for constant returns would be greatly diminished. It is not the returns that most investors are chasing, it is homeostasis.

I think that you are doing tremendous harm by publishing articles that mislead the public into thinking that capitalists do not want recovery.

I founded a non-profit for Venezuela and one of the tools consistently used by the government there is to publicly blame capitalists for their economic woes. Meanwhile their murder rate now exceeds that of Iraq, they are top in the world for misuse of public funds, bottom of the world for private property, and on the brink of a full meltdown. And as this is happening half the country thinks that it is the fault of the average businessman that must only be making a profit at their expense. Small businesses are being looted and taken over by the government while shortages increase and inflation soars at over 60%. Are capitalists profiting from this crisis? No just corrupt politicians and businessmen that collude with state run enterprises all of whom would never survive in a capitalist economy.

Please be careful whom you label a capitalist.

Sincerely,

X

Traditionally, comedy, parody and satire were the sophisticated weapons of the weak, methods through which the subjects could poke fun at their rulers and ridicule their entourages. Great artists, from Aristophanes to Moliere and Balzac to Charlie Chaplin, laboured to dissect the human comedy, to expose its ugliness, stupidity and futility for everyone to see. They laughed at the rich and powerful, jesting at their pitiful attempts to justify the unjustifiable. Using extreme situations, they cornered their protagonists into absurd positions, showing them as dogmatic knuckleheads, unable to understand, let alone transcend, the confines of their social roles.

Reading Mr. X’s email, we thought that maybe this model has now run its course. Aristophanes and his followers offered us a highly sophisticated account of human folly. But their creation, although highly artistic, was still a mere imitation, a fancy forgery of reality. Nowadays, though, it seems that we no longer need such imitations. We have the real thing: penetrating, authentic satires of the dominant reality produced and directed by the gatekeepers themselves.

Now, every work of art, whether high or low, deserves critical assessment. It must be put in context, translated, clarified, explicated and interpolated. It has to be elevated for the experts and simplified for the laity. It needs to be ‘deconstructed’. So let us begin.

Deconstruction

Mr. X’s emotional email reflects a broader capitalist anxiety. The world is rapidly changing, and not for the better. First, the liberal economic model is now being questioned. The global financial crisis and the Great Recession have revealed not only that the market is not self-correcting, but also that policymakers might be unable to fix what markets have broken. Second, the material outlook for much of humanity remains dim. Despite the victory of capitalism over communism, large segments of the world’s population live in utter poverty, with little prospect for change, while many of the so-called middle classes, particularly the younger generations, are threatened by chronic unemployment and dead-end jobs. And third, capitalism seems to be destabilizing the natural environment. Pollution is intensifying, habitats are being destroyed, resources are being depleted, and the overall climate might be changing, possibly for the worse.

And yet, despite this triple calamity – or perhaps because of it – the upward redistribution of income and assets continues unabated. While much of the world’s population is stuck in the doldrums, dominant capital seems to be growing ever more powerful. The leading capitalists and their investment organs are taking over larger and larger chunks of our natural resources, human-made artefacts and collective knowledge; they formulate and steer public policy to their own advantage; and they dominate ideology, education and the mass media.

Some capitalists, particularly the bigger ones, are beginning to fear that this divergence is untenable. They realize that if this sabotage-led redistribution continues, something will have to give; and when that happens, they might find themselves heading for the hills.

As a class, though, capitalists are unable to do much about this systemic risk. First, no ruling class voluntarily gives up its power, particularly not at the hubris stage, when that power seems unassailable. Second, the very power logic of accumulation – the need to strategically sabotage others in order to increase one’s own share of the total – forces capitalists to continue and dig their own graves, so to speak.

Now, of course, most capitalists, particularly the smaller ones, are unaware of and certainly won’t admit these power underpinnings of capitalism. Although they feel the global reverberations and sense the mounting anxiety, they scarcely connect these with their own experience. As far as they are concerned, their own goal – and by extension, the goal of the entire system – is more production, more profit and, eventually, more utility. This liberal mind-set, propagated by economists since Adam Smith, enables them to bifurcate their world into two separate spheres – economics and politics – and by so doing to deny the power basis of capital in the first place.

Accumulation in this dual world is a free ‘economic’ act and as such cannot harbour power, by definition. Investment, production, trade and consumption are all seen as voluntary individual undertakings and therefore devoid of coercion, force and sabotage. It is of course true, say the dualists, that the economy in general and accumulation in particular could be contaminated by power. But power is an external distortion, coming from outside the economy proper. It originates not in the flat world of economics, but in the vertical world of politics. It emanates not from the productive acts of businessmen and investors, but from the mischief of villainous governments, corrupt public officials, greedy labour unions, state-sanctioned monopolies and violent criminals. That, in any event, is the conventional creed.

According to this conventional creed, the only hope for our world was and remains the free market. Private investment – provided we keep it free of political intervention – is the safest way to undo power and unleash prosperity. There is a little fly in the ointment, though. As it turns out, profit-maximizing agents could – unintentionally of course – undermine the interests of others. These unwilled consequences are called ‘externalities’ (external to the market transactions that created them), and, in principle, could include anything – from pollution and climate change, to unemployment and crime, to financial crises and great depressions. Fortunately, though, this problem too can be fixed – and not by outside intervention, but by the market itself. Instead of society interfering with the market, the right thing to do is to marketize society, to bring it into the pecuniary fold of accumulation.

In business lingo, this solution is called ‘socially responsible’, or ‘ethical’ investing, and it is here that Mr. X comes onto the stage.

Ethical investing

Mr. X is an ‘ethical asset manager’. His fund, based in a reputable tax haven, is committed to the common good and donates money to help the planet. The managers of the fund believe that humans can find a balance with the environment, and they urge us all to work together in order to promote – and profit from – this new ethical/sustainable equilibrium.

For politically correct capitalists with substantial money to invest, Mr. X’s fund offers a carefully hedged, two-pronged strategy: buying and holding do-good companies that profit from saving the planet while shorting firms that harm the environment and governments that misallocate the world’s resources. Now, assuming that the world is about to become a better place, this is a win-win strategy and, therefore, likely to ‘beat the average’ and outperform the leading global indices. And since outperformers by definition come out on top, we have a self-fulfilling prophecy: the sustainable and therefore more profitable capitalists will gradually replace the unsustainable, less profitable ones.

So in the end, capitalism is self-correcting. All you need to do is harness the existing rituals of differential accumulation to the common good, and the rest will take care of itself.

The parody

With this theoretical framework in mind, it is easy to see that the world we live in isn’t capitalistic at all. It is statist.

Real capitalism has no distorting entities. It has no government, no central bank, no judicial system, no courts, no police and no jails. It has no army, no ideology, no public education or public transportation. It has no paper money, no enforced units of measure and probably no common language. It also has no corporate coalitions, labour unions and NGOs. And, as educators, it is our duty to present this true vision of capitalism to our students. Otherwise, they might end up confusing the world around them for reality.

The original state of nature. Now, once upon a time there existed a real, undistorted capitalist system as outlined above. In this true system, money was weighed in gold and the price of a commodity reflected its true value. Regrettably, though, true capitalism no longer exists. Somewhere along the way, and for totally exogenous reasons, it gave way to a distorted statist system. In this new system, money is monopolized by the government and private banks. Together, they create private credit out of thin air and then force the rest of us to use this credit as if it were ‘real money’.

Unlike true capitalism, distorted statism is manifestly unfair. Statism favours large corporations, which in turn influence governments and the banks to give them cheap credit – while at the same time screwing the ‘unconnected’ little guy. The situation is particularly bad during crises, when the banks don’t create enough credit for everyone. Now, to repeat, this setup has absolutely nothing to do with true capitalism. In fact, and here you might want to hold onto your seat, the executives and owners of firms that rely on the government – i.e., the S&P 500 that Mr. X tries so hard to outperform – are not capitalists at all!

So who are the real capitalists? If you haven’t guessed it by now, real capitalists are those who never accumulate. To be a real capitalist, you have to either lose money or break even with enough income to survive. You see, capitalism is just like nature: it thrives on growth as well as decomposition (a Marshallian metaphor that Chauncey Gardiner, the protagonist of Jerzy Kosinski’s 1971 book Being There, would merrily concur with). Moreover, many real capitalists are perfectly happy with a steady state (fixed profit?). The only reason they might seek growth (more profit?) is to offset the inflation created by the false system of private credit money. Remove the curse of false money (along with the other distortions), and capitalism would immediately converge to a stable metabolic equilibrium.3

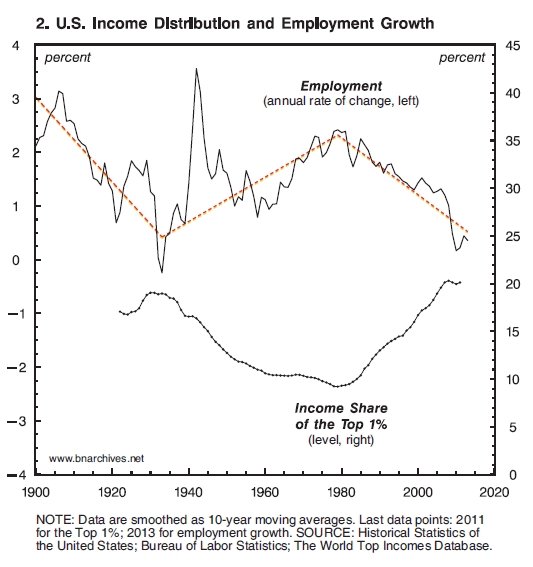

Mistaking correlation for causation. Now, in the meantime, there is no denying that, for the past 70 years, the U.S. rate of unemployment and the domestic income share of capital were positively and very tightly correlated (Figure 1); and it is equally true that, over the past 90 years, the income share of the Top 1% and the growth rate of employment were negatively correlated (Figure 2). Moreover, these facts make perfect sense – they show how statist policymakers and central bankers skew, distort and undermine the system in favour of their big-business buddies. But then remember that none of this is related in any way to real capitalism, real capital, and real capitalists.

Saving the planet. To see real capitalists in action, you need go to their ‘impact investing’ gatherings, where they deliberate saving the world, capitalist style. In these conventions – which unfortunately have to host detested government officials who subsidize the proceedings, as well as confused academic economists and token civil-society representatives – the discussion focuses exclusively on the world’s gravest problems (caused, no doubt, by government distortions, market imperfections and assorted externalities). The mood in these conferences is happily collective. The goal is usually practical: to come up with ‘business ideas’ and ‘market solutions’ that ‘actually work’ (needless to say, non-business/non-market platforms are viewed with great suspicion, while anti-business and anti-market ideas are rarely if ever allowed in the door). In this context, there is obviously no need to speak about ‘beating the average’ and certainly not about ‘gaining power over others’.

Outperforming. However, when the conference is over and the participants return to their offices, the imperatives of accumulation take over. Unlike the collective/cooperative language of the convention hall, here the parameters are entirely differential and totally unsentimental. Whether it ends up saving the world or not, the key imperative here is to outperform. The mandate of the ‘ethical fund manager’ is simple: leverage the world’s distortions and imperfections by selling short and buying long future variations of inequality, the ups and downs of expected hunger, anticipated ecological degradation and regeneration and other assorted disasters and triumphs – and do it all in such a way that we, your capitalist clients, end up beating the holy average.

There will be blood. Now, in the best of all possible worlds (real capitalism) there would be no contradiction between these two activities, or so we are told. Beating the average would help save the world, and saving the world would help beat the average (‘positive-sum game’). The problem is that, according to the enlightened capitalist, we don’t live in the best of all possible worlds, but in one of the worst (statism). And here the benchmark is totally ‘rigged’. It reflects not the flat returns on homeostatic productivity, but the steep returns on power and sabotage. So in the end, the only way to beat the big unreal capitalists of the distorted world is to joint them. Just don’t tell anyone, or there will be blood.

- See, for example, Bichler, Shimshon, and Jonathan Nitzan. 2008. Contours of Crisis: Plus ça change, plus c’est pareil? Dollars & Sense, December 29.

Bichler, Shimshon, and Jonathan Nitzan. 2009. Contours of Crisis II: Fiction and Reality. Dollars & Sense, April 28.

Bichler, Shimshon, and Jonathan Nitzan. 2010. Systemic Fear, Modern Finance and the Future of Capitalism. Monograph, Jerusalem and Montreal (July): 1-42.

Kliman, Andrew, Shimshon Bichler, and Jonathan Nitzan. 2011. Systemic Crisis, Systemic Fear: An Exchange. Special Issue on ‘Crisis’. Journal of Critical Globalization Studies (4, April): 61-118.

Bichler, Shimshon, and Jonathan Nitzan. 2012. The Asymptotes of Power. Real-World Economics Review (60, June): 18-53.

Bichler, Shimshon, and Jonathan Nitzan. 2013. Can Capitalists Afford Recovery? Economic Policy When Capital is Power. Working Papers on Capital as Power (2013/01, October): 1-36.

Bichler, Shimshon, and Jonathan Nitzan. 2014a. How Capitalists Learned to Stop Worrying and Love the Crisis. Real-World Economics Review (66, January): 65-73.

Bichler, Shimshon, and Jonathan Nitzan. 2014b. No Way Out: Crime, Punishment and the Limits to Power. Crime, Law and Social Change. 61 (3, April): 251-271.

Bichler, Shimshon, Jonathan Nitzan, and Tim Di Muzio. 2012. The 1%, Exploitation and Wealth: Tim Di Muzio interviews Shimshon Bichler and Jonathan Nitzan. Review of Capital as Power 1 (1): 1-22.

Bichler, Shimshon, Jonathan Nitzan, and Piotr Dutkiewicz. 2013. Capitalism as a Mode of Power: Piotr Dutkiewicz in Conversation with Shimshon Bichler and Jonathan Nitzan. In 22 Ideas to Fix the World: Conversations with the World’s Foremost Thinkers, edited by P. Dutkiewicz and R. Sakwa. New York: New York University Press and the Social Science Research Council: 326-354. [↩]

- Nitzan, Jonathan, and Shimshon Bichler. 2014. Profit from Crisis: Why Capitalists Do Not Want Recovery, and What That Means for America. Frontline, May 2: 129-131. [↩]

- The interesting side-plot here is that, although real capitalists ‘do not desire nor pursue constant economic growth’, this self-evident truth of steady-state capitalism should never be publicized. And why not? Because such a revelation, says the ecological capitalist, would allow corrupt politicians and their crony big businessmen to discredit the no-growth capitalists, thus killing the very chance of ever achieving the homeostatic bliss…. [↩]

1 2 55

{kind=link}

{kind=link}