Research Note

How Capitalists Learned to Stop Worrying and Love the Crisis

by Shimshon Bichler and Jonathan Nitzan [1]

Jerusalem and Montreal, November 22, 2013

![]()

Economic, financial and social commentators from all directions and of all persuasions are obsessed with the prospect of recovery. The world remains mired in a deep, prolonged crisis, and the key question seems to be how to get out of it.

There is, however, a prior question that few if any bother to ask: Do capitalists want a recovery in the first place? Can they afford it?

On the face of it, the question sounds silly: of course capitalists want a recovery; how else can they prosper? According to the textbooks, both mainstream and heterodox, capital accumulation and economic growth are two sides of the same process. Accumulation generates growth and growth fuels accumulation, so it seems bootless to ask whether capitalists want growth. Growth is their lifeline, and the more of it, the better it is.

Or is it?

Accumulation of What?

The answer depends on what we mean by capital accumulation. The common view of this process is deeply utilitarian. Capitalists, we are told, seek to maximize their so-called ‘real wealth’: they try to accumulate as many machines, structures, inventories and intellectual property rights as they can. And the reason, supposedly, is straightforward. Capitalists are hedonic creatures. Like every other ‘economic agent’, their ultimate goal is to maximize their utility from consumption. This hedonic quest is best served by economic growth: more output enables more consumption; the faster the expansion of the economy, the more rapid the accumulation of ‘real’ capital; and the larger the capital stock, the greater the utility from its eventual consumption. Utility-seeking capitalists should therefore love booms and hate crises. [2]

But that is not how real capitalists operate.

The ultimate goal of modern capitalists – and perhaps of all capitalists since the very beginning of their system – is not utility, but power. They are driven not to maximize hedonic pleasure, but to ‘beat the average’. This aim is not a subjective preference. It is a rigid rule, dictated and enforced by the conflictual nature of the capitalist mode of power. Capitalism pits capitalists against other groups in society, as well as against each other. And in this multifaceted struggle for power, the yardstick is always relative. Capitalists are compelled and conditioned to accumulate differentially, to augment not their absolute utility but their earnings relative to others. They seek not to perform but to out-perform, and outperformance means re-distribution. Capitalists who beat the average redistribute income and assets in their favour; this redistribution raises their share of the total; and a larger share of the total means greater power stacked against others.

Shifting the research focus from utility to power has far-reaching consequences. Most importantly, it means that capitalist performance should be gauged not in absolute terms of ‘real’ consumption and production, but in financial-pecuniary terms of relative income and asset shares. And as we move from the materialist realm of hedonic pleasure to the differential process of conflict and power, the notion that capitalists love growth and yearn for recovery is no longer self evident.

The accumulation of capital as power can be analyzed at many different levels. The most aggregate of these levels is the overall distribution of income between capitalists and other groups in society. In order to increase their power, approximated by their income share, capitalists have to strategically sabotage the rest of society. And one of their key weapons in this struggle is unemployment.

The effect of unemployment on distribution is not obvious, at least not at first sight. Rising unemployment, insofar as it lowers the absolute (‘real’) level of activity, tends to hurt capitalists and employees alike. But the impact on money prices and wages can be highly differential, and this differential can move either way. If unemployment causes the price/wage ratio to decline, capitalists will fall behind in the redistributional struggle, and this retreat is sure to make them impatient for recovery. But if the opposite turns out to be the case – that is, if unemployment helps raise the price/wage ratio – capitalists would have good reason to love crisis and indulge in stagnation.

So which of these two scenarios pans out in practice? Do stagnation and crisis increase capitalist power? Does unemployment help capitalists raise their distributive share? Or is it the other way around?

Unemployment and the Capitalist Income Share

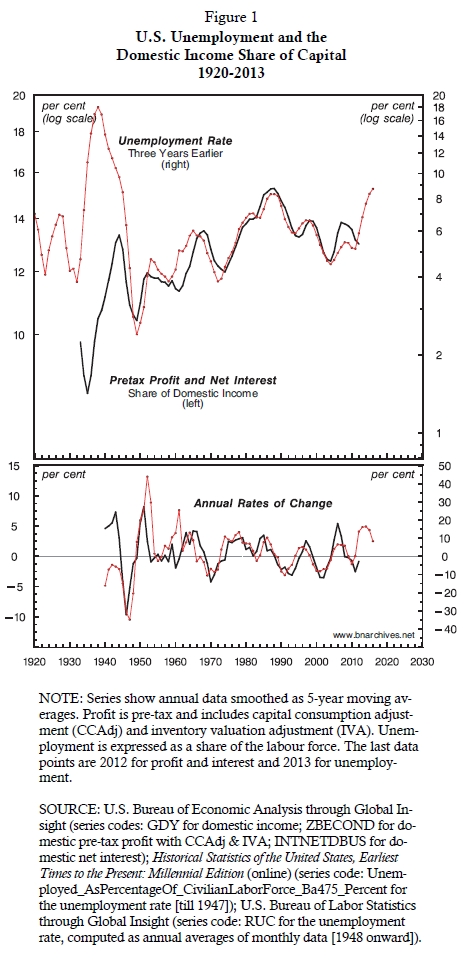

Figures 1 and 2 examine this process in the United States, showing the relationship between the share of capital in domestic income and the rate of unemployment since the 1930s. The top panel of Figure 1 displays the levels of the two variables, both smoothed as 5-year moving averages. The solid line, plotted against the left log scale, depicts pre-tax profit and net interest as a percent of domestic income. The dotted line, plotted against the right log scale, exhibits the rate of unemployment as a share of the labour force. Note that the unemployment series is lagged three years, meaning that every observation shows the situation prevailing three years earlier. The bottom panel displays their respective annual rates of change of the two top variables, beginning in 1940.

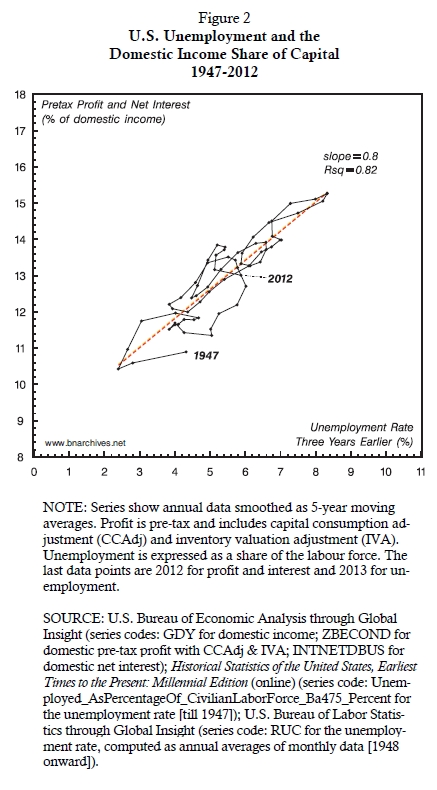

The same relationship is shown, somewhat differently, in Figure 2. This chart displays the same variables, but instead of plotting them against time, it plots them against each other. The capitalist share of domestic income is shown on the vertical axis, while the rate of unemployment three years earlier is shown on the horizontal axis (for a different examination of this relationship, including its theoretical and historical nonlinearities, see Nitzan and Bichler 2009: 236-239, particularly Figures 12.1 and 12.2).

Now, readers conditioned by the prevailing dogma would expect the two variables to be inversely correlated. The economic consensus is that the capitalist income share in the advanced countries is procyclical (see for example, Giammarioli et al. 2002; Schneider 2011). Expressed in simple words, this belief means that capitalists should see their share of income rise in the boom when unemployment falls and decline in the bust when unemployment rises.

But that is not what has happened in the United States. According to Figures 1 and 2, during the post-war era, the U.S. capitalist income share has moved countercyclically, rising in downturns and falling in booms.

The relationship between the two series in the charts is clearly positive and very tight. Regressing the capitalist share of domestic income against the rate of unemployment three years earlier, we find that for every 1 per cent increase in unemployment, there is 0.8 per cent increase in the capitalist share of domestic income three years later (see the straight OLS regression line going through the observations in Figure 2). The R-squared of the regression indicates that, between 1947 and 2012, changes in the unemployment rate accounted for 82 per cent of the squared variations of capitalist income three years later. [3]

The remarkable thing about this positive correlation is that it holds not only over the short-term business cycle, but also in the long term. During the booming 1940s, when unemployment was very low, capitalists appropriated a relatively small share of domestic income. But as the boom fizzled, growth decelerated and stagnation started to creep in, the share of capital began to trend upward. The peak power of capital, measured by its overall income share, was recorded in the early 1990s, when unemployment was at post-war highs. The neoliberal globalization that followed brought lower unemployment and a smaller capital share, but not for long. In the late 2000s, the trend reversed again, with unemployment soaring and the distributive share of capital rising in tandem.

Box 1

Underconsumption

The empirical patterns shown in Figures 1 and 2 seem consistent with theories of underconsumption, particularly those associated with the Monopoly Capital School. According to these theories, the oligopolistic structure of modern capitalism is marked by a growing ‘degree of monopoly’. The increasing degree of monopoly, they argue, mirrors the redistribution of income from labour to capital. Upward redistribution, they continue, breeds underconsumption. And underconsumption, they claim, leads to stagnation and crisis. The observed positive correlation between the U.S. capitalist share of income and the country’s unemployment rate, they would conclude, is only to be expected (cf. Kalecki 1933; 1939; 1943; Steindl 1952; Tsuru 1956; Baran and Sweezy 1966; Magdoff and Sweezy 1983; Foster and Szlajfer 1984; for a survey of recent arguments and evidence, see van Treeck and Sturn 2012; Lavoie and Stockhammer 2013).

There is, however, a foundational difference between the underconsumptionist view and the claims made in this research note. In our opinion, the end goal of capitalists is the augmentation of power. This goal is pursued through strategic sabotage and is achieved when capitalists manage to redistribute income and assets in their favour. The underconsumptionists, by contrast, share with mainstream economists the belief that capitalists are driven to maximize their ‘real’ capital stock. From this latter perspective, favourable redistribution is in fact detrimental to capitalist interests: the higher the capitalist income share, the stronger the tendency toward underconsumption and stagnation; and the more severe the stagnation, the greater the likelihood of capitalists suffering a ‘real’ accumulation crisis.

Employment Growth and the Top 1%

The power of capitalists can also be examined from the viewpoint of the infamous ‘Top 1%’. This group comprises the country’s highest income earners. It includes a variety of formal occupations, from managers and executives, to lawyers and doctors, to entertainers, sports stars and media operators, among others (Bakija, Cole, and Heim 2012), but most of its income is derived directly or indirectly from capital.

The Top 1% features mostly in ‘social’ critiques of capitalism, echoing the conventional belief that accumulation is an ‘economic’ process of production and that the distribution of income is merely a derivative of that process. [4] This belief, though, puts the world on its head. Distribution is not a corollary of accumulation, but its very essence. And as it turns out, in the United States, the distributional gains of the Top 1% have been boosted not by growth, but by stagnation.

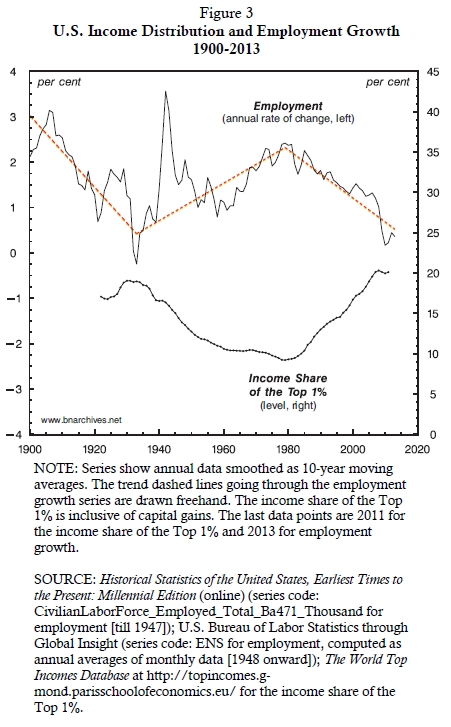

Figure 3 shows the century-long relationship between the income share of the Top 1% of the U.S. population and the annual growth rate of U.S. employment (with both series smoothed as 10-year moving averages).

The overall relationship is clearly negative. When stagnation sets in and employment growth decelerates, the income share of the Top 1% actually rises – and vice versa during a long-term boom (reversing the causal link, we get the generalized underonsumptionist view, with rising overall inequality breeding stagnation – see Box 1).

Historically, this negative relationship shows three distinct periods, indicated by the dashed, freely drawn line going through the employment growth series. The first period, from the turn of the century till the 1930s, is the so-called Gilded Age. Income inequality is rising and employment growth is plummeting.

The second period, from the Great Depression till the early 1980s, is marked by the Keynesian welfare-warfare state. Higher taxation and spending make distribution more equal, while employment growth accelerates. Note the massive acceleration of employment growth during the Second World War and its subsequent deceleration bought by post-war demobilization. Obviously these dramatic movements were unrelated to income inequality, but they did not alter the series’ overall upward trend.

The third period, from the early 1980s to the present, is marked by neoliberalism. In this period, monetarism assumes the commanding heights, inequality starts to soar and employment growth plummets. The current rate of employment growth hovers around zero while the Top 1% appropriates 20 per cent of all income – similar to the numbers recorded during Great Depression.

How Capitalists Learned to Stop Worrying and Love the Crisis

If we follow the conventional macroeconomic creed, whether mainstream or heterodox, U.S. capitalism is in bad shape. For nearly half a century, the country has watched economic growth and ‘real’ accumulation decelerate in tandem – so much so that that both measures now are pretty much at a standstill (Bichler and Nitzan 2013: 24, Figure 12). To make a bad situation worse, policy attempts to ‘get the economy going’ seem to have run out of fiscal and monetary ammunition (Bichler and Nitzan 2013: 2-13). Finally, and perhaps most ominously, many policymakers now openly admit to be ‘flying blind when steering their economies’ (Giles 2013).

And yet U.S. capitalists seem blasé about the crisis. Instead of being terrified by zero growth and a stationary capital stock, they are obsessed with ‘excessive’ deficits, ‘unsustainable debt’ and the ‘inflationary consequences’ of the Fed’s so-called quantitative easing. Few capitalists if any call on their government to lower unemployment and create more jobs, let alone to rethink the entire model of economic organization.

The evidence in this research note serves to explain this nonchalant attitude: Simply put, U.S. capitalists are not worried about the crisis; they love it.

Redistribution, by definition, is a zero-sum game: the relative gains of one group are the relative losses of others. However, in capitalism, the end goals of those struggling to redistribute income and assets can differ greatly. Workers, the self-employed and those who are out of work seek to increase their share in order to augment their well being. Capitalists, by contrast, fight for power. Contrary to other groups in society, capitalists are indifferent to ‘real’ magnitudes. Driven by power, they gauge their success not in absolute units of utility, but in differential pecuniary terms, relative to others. Moreover – and crucially – their differential performance-read-power depends on the extent to which they can strategically sabotage the very groups they seek to outperform.

In this way, rising unemployment – which hammers the well-being of workers, unincorporated businesses and the unemployed – serves to boost the overall income share of capitalists. And as employment growth decelerates, the income share of the Top 1% – which includes the capitalists as well as their protective power belt – soars. Under these circumstances, what reason do capitalists have to ‘get the economy going’? Why worry about rising unemployment and zero job growth when these very processes serve to boost their income-share-read-power?

The process, of course, is not open-ended. There is a certain limit, or asymptote, beyond which further increases in capitalist power are bound to create a backlash that might destabilize the entire system (Bichler and Nitzan 2010; Kliman, Bichler, and Nitzan 2011; Bichler and Nitzan 2012). Capitalists, though, are largely blind to this asymptote. Their power drive conditions and compels them to sustain and increase their sabotage in their quest for an ever-rising distributive share. Like other ruling classes in history, they are likely to realize they have reached the asymptote only when it is already too late.

For our full paper on the subject, see:

Shimshon Bichler and Jonathan Nitzan, ‘Can Capitalist Afford Recovery? Economic Policy When Capital is Power’, Working Papers on Capital as Power, No. 2013/01, October 2013, pp. 1‑36. (http://bnarchives.yorku.ca/377/)

End Notes

[1] Shimshon Bichler teaches political economy at colleges and universities in Israel. Jonathan Nitzan teaches political economy at York University in Canada. All of their publications are available for free on The Bichler & Nitzan Archives (http://bnarchives.net). Research for this paper was partly supported by the SSHRC.

[2] For Marx, the end goal of accumulation is accumulation itself: ‘Accumulate, Accumulate! That is Moses and the Prophets! . . . Accumulation for accumulation's sake, production for production’s sake’ (Marx 1867: 652). Contemporary Marxists, however, equate accumulation with the growth of the so-called ‘real’ capital stock, as published by the (neoclassical) national accounts. And since the latter accounts (supposedly) measure the util-generating capacity of said capital (OECD 2001), the ‘Marxist capitalist’, just like her mainstream counterpart, ends up pursuing hedonic pleasure. . . .

[3] The three-year lag means that the redistributional consequences of unemployment are manifested only gradually. The exact nature of this gradual process requires further research.

[4] Following J.B. Clark (1899), neoclassical manuals assert that, under perfect competition, the income of every ‘factor of production’ is equal to its (marginal) productive contribution. In this way, capitalists, workers and the owners of raw materials receive in income what they add to the economy’s output and therefore to the well-being (i.e. utility) of society. The inequality arising from this process may create ‘social problems’ and ‘political instability’, but these unfortunate side effects are usually seen as lying safely outside the objective domain of economics proper.

References

Bakija, Jon, Adam Cole, and Bradley T. Heim. 2012. Jobs and Income Growth of Top Earners and the Causes of Changing Income Inequality: Evidence from U.S. Tax Return Data. Working Paper.

Baran, Paul. A., and Paul M. Sweezy. 1966. Monopoly Capital. An Essay on the American Economic and Social Order. New York: Modern Reader Paperbacks.

Bichler, Shimshon, and Jonathan Nitzan. 2010. Systemic Fear, Modern Finance and the Future of Capitalism. Monograph, Jerusalem and Montreal (July), pp. 1-42.

Bichler, Shimshon, and Jonathan Nitzan. 2012. The Asymptotes of Power. Real-World Economics Review (60, June): 18-53.

Bichler, Shimshon, and Jonathan Nitzan. 2013. Can Capitalists Afford Recover? Economic Policy When Capital is Power. Working Papers on Capital as Power (2013/01, October): 1-36.

Clark, John Bates. 1899. [1965]. The Distribution of Wealth. New York: Augustus M. Kelley.

Foster, John Bellamy, and Henryk Szlajfer, eds. 1984. The Faltering Economy. The Problem of Accumulation Under Monopoly Capitalism. New York: Monthly Review Press.

Giammarioli, Nicola, Julian Messina, Thomas Steinberger, and Chiara Strozzi. 2002. European Labor Share Dynamics: An Institutional Perspective. EUI Working Paper ECO No. 2002/13, Department of Economics, European University Institute, Badia Fiesolana, San Domenico (FI).

Giles, Chris. 2013. Central Bankers Say They Are Flying Blind. Financial Times, April 17.

Kalecki, Michal. 1933. [1971]. The Determinants of Profits. In Selected Essays on the Dynamics of the Capitalist Economy, edited by M. Kalecki. Cambridge: Cambridge University Press, pp. 78-92.

Kalecki, Michal. 1939. [1971]. Determination of National Income and Consumption. In Selected Essays on the Dynamics of the Capitalist Economy, edited by M. Kalecki. Cambridge: Cambridge University Press, pp. 93-104.

Kalecki, Michal. 1943. [1971]. Costs and Prices. In Selected Essays on the Dynamics of the Capitalist Economy, 1933-1970. Cambridge: Cambridge University Press, pp. 43-61.

Kliman, Andrew, Shimshon Bichler, and Jonathan Nitzan. 2011. Systemic Crisis, Systemic Fear: An Exchange. Special Issue on 'Crisis'. Journal of Critical Globalization Studies (4, April): 61-118.

Lavoie, Marc, and Engelbert Stockhammer. 2013. Wage-Led Growth: Concepts, Theories and Policies. ILO Conditions of Work and Employment Series (41): 1-32.

Magdoff, Harry, and Paul M. Sweezy. 1983. [1987]. Stagnation and the Financial Explosion. New York: Monthly Review Press.

Marx, Karl. 1867. [1906]. Capital. A Critique of Political Economy. Vol. 1: The Process of Capitalist Production. Translated From the Third German Edition, By Samuel Moore and Edward Aveling and Edited by Frederick Engels. Revised and Amplified According to the Fourth German Edition by Enrest Untermann. Chicago: Charles H. Kerr & Company.

Nitzan, Jonathan, and Shimshon Bichler. 2009. Capital as Power. A Study of Order and Creorder. RIPE Series in Global Political Economy. New York and London: Routledge.

OECD. 2001. Measuring Capital. Measurement of Capital Stocks, Consumption of Fixed Capital and Capital Services. OECD Manual. Paris: OECD Publication Services.

Schneider, Dorothee. 2011. The Labor Share: A Review of Theory and Evidence. Discussion Paper 2011-069. SFB 649 "Economic Risk": 1-38.

Steindl, Josef. 1952. [1976]. Maturity and Stagnation in American Capitalism. New York: Monthly Review Press.

Tsuru, Shigeto. 1956. Has Capitalism Changed? In Has Capitalism Changed? An International Symposium on the Nature of Contemporary Capitalism, edited by S. Tsuru. Tokyo: Iwanami Shoten, pp. 1-66.

van Treeck, Till, and Simon Sturn. 2012. Income Inequality as a Cause of the Great Recession? A Survey of Current Debates. ILO Conditions of Work and Employment Series (39): 1-93.