… the value of a commodity is determined

by the quantity of labour spent on it …

In the 1860s, Karl Marx declared that all value stemmed from labor. A century-long firestorm ensued.

On its own, Marx’s claim seems innocent enough. But what made it incendiary was how he used it. Starting from the idea that labor creates value, Marx built a seductive critique of capitalism. If workers alone create value, then capitalists are ultimately parasites — engorged ticks living off the blood of their unwitting hosts.

Marx’s arguments were impeccable and his theoretical edifice towering. But there’s just one problem. The whole thing was based on a foundation of quicksand.

Marx proclaimed that value is proportional to labor time. But he never bothered to check if this was correct. He simply defined it to be true, and got on building his theory of capitalism. Nor did Marx think about what his theory implied about human nature. If Marx’s theory is true, why do humans judge value in terms of labor time? Do we possess some universal value-judging faculty? If so, how did it evolve? Marxists rarely ask these questions, probably because the answers are uncomfortable.

When he wrote Capital, Marx thought he was making a seminal contribution to science. The reality is sadly different. While the ideological component of his work has thrived, the scientific component has withered. Beaten back by contradicting evidence, Marxists have largely abandoned the idea that the price of a commodity is proportional to labor time. What remains is a thin husk of Marx’s original theory.

To ‘validate’ the labor theory of value, Marxists now look not at commodities, but at vast chunks of the economy. There they find that monetary value correlates strongly with labor time. This correlation, Marxists claim, is robust evidence for the labor theory of value.

I argue that it is not.

The purpose of this essay is to put the last vestiges of the labor theory of value to rest. My goal is to explain why when we look at large sections of the economy, we find that value added correlates with labor time. The correlation comes not from some universal law of value. Instead, I argue that it results from a simple heuristic: humans seek income that is equivalent to their peers’. I call this principle the ‘egalitarian heuristic’. If it holds, even in rough form, then value added will correlate strongly with labor time. In short, we do not need the labor theory of value to explain the evidence.

In a sense, my argument is tragic because it brings us back to Marx’s starting point. Looking at human society through the lens of egalitarianism, Marx concluded that capitalism was unjust. But instead of admitting that this was a value judgment, Marx attempted to enshrine his values as an objective truth. By doing so, he used the cloak of science to create a rapturous ideology.

Marx’s armchair

Economists are often accused of doing armchair philosophy. From the comfort of their academic thrones, they postulate ideas about human behavior. But they don’t follow up with the grunt work of science — the messy business of testing ideas against real-world evidence.

The armchair method was pioneered by political economists like Adam Smith and David Ricardo. Both men claimed that prices were proportional to labor time. But neither economist bothered to check the data. When Marx began writing about political economy, he adopted the same armchair method (admittedly on a ‘throne’ that was less comfortable than Smith’s or Ricardo’s). In what would become his seminal work, Marx began Capital by reasserting Smith and Ricardo’s principle that value is proportional to labor time. And like these earlier thinkers, Marx provided no evidence that this claim was true. But what followed was entirely different.

Marx took the labor theory of value in an unanticipated direction, using it to create a devastating critique of both capitalism and of mainstream political economy. The results live with us today. While Smith and Ricardo are remembered as important thinkers, there are few self-professed ‘Smithian’ or ‘Ricardian’ economists. But there are plenty of economists who call themselves ‘Marxists’.

Ernest Mandel was one of them. A Holocaust survivor and Nazi resistance fighter, Mandel was a tireless advocate of Marxist principles. But while his life as an activist was exemplary, his work as a scientist was less so. The problem boils down to the armchair method. Is it okay to build a theory on a hypothesis that goes untested? Mandel seemed to think so. In fact, he celebrated it. The labor theory of value, he argued, was not a hypothesis. It was a definition:

For Marx, labour is value.

(Ernest Mandel, 1990; emphasis in original)

Other Marxists have come to similar conclusions. The economic historian (and self-professed Marxist) E.K. Hunt concludes that the labor theory of value is “not a theory in any usual sense”. It is a definition, plain and simple. And because it is a definition, Hunt argues, the labor theory of value can’t be evaluated in the normal way (say, by testing its assumptions). Instead, we must judge the theory by asking whether it gives ‘insight’ into the nature of capitalism:

[T]he labour theory’s scientific merit rests entirely on the usefulness of the insights gained by looking at capitalism in this [Marxist] way.

Given this standard for ‘scientific merit’, Hunt argues that the labor theory of value is wildly successful:

[W]hile this conception of value is definitional, it represented, for Marx, a profound scientific discovery whereby one could go behind the superficial appearance of market exchange to discover the hidden essence of capitalism.

Generations of Marxists have been hypnotized by this type of euphoric thinking. But there’s a glaring problem. If you don’t test your assumptions, how do you know if your theory gives ‘useful insights’?

And there’s the rub. E.K. Hunt is doing the Marxist equivalent of Milton Friedman’s ‘F-twist’. In an attempt to defend absurd neoclassical assumptions, Milton Friedman proclaimed that assumptions are irrelevant. If the theory is ‘useful’, Friedman argued, that’s good enough. The trouble is that ‘usefulness’ is in the eye of the beholder. In other words, it is a value judgment.

In this light, the labor theory of value is an exercise in circular values. Marx used anti-capitalist sentiment to define a theory of value that he then judged by the apparent ‘rigor’ it gave to his anti-capitalist sentiment. What Hunt and Mandel seem not to realize is that this is bad science. You cannot judge a hypothesis using the same criteria that were used to create it.

Why do Marxists always go up?

Misgivings aside, suppose that we accept Hunt’s claim that we can judge the labor theory of value based on the insight it gives into the ‘hidden essence of capitalism’. There is still a problem. Scientists are not allowed to put boundaries on how others should test their theory.

Imagine if after proposing his theory of gravity, Isaac Newton declared that it could only be tested using the orbit of Mars. If scientists had obeyed such a command, no one would have discovered that Newton’s theory failed for the planet Mercury. And without this well-known aberration, there would have been no motivation for a better theory. Hence, there would be no general relativity (and today, no debate over dark matter).

If we look carefully at Hunt’s words, we see that he is doing something similar to our counterfactual Newton: Hunt is defining the terms by which we are ‘allowed’ to test the labor theory of value. Unsurprisingly, those terms place the theory in a good light. The theory, Hunt claims, reveals the ‘hidden essence of capitalism’. And it is based ‘entirely’ on this insight that we are to judge the labor theory of value.

Fortunately (for critics like me), science does not work like that. Once a theory is proposed, other scientists can test it anyway they like. Sure, Marx took the labor theory of value ‘up’ to the nature of capitalism. But we can equally take it ‘down’ and see what it implies about human nature. The problem, though, is that taking the labor theory of value ‘down’ leads to uncomfortable questions.

Marxists like E.K. Hunt argue that we should evaluate the labor theory of value based on the insight it gives into the ‘hidden essence of capitalism’. But we are not obliged to do so. We can also judge the labor theory of value by the insight it gives into human nature. The trouble is that doing so yields nonsense.

Suppose that Marx is correct, and that ‘value’ is universally proportional to labor time. How could this be?

After having admitted that the labor theory of value is based on a ‘definition’, Marxists are immediately in a tough spot. If this definition is arbitrary (as most definitions are), then the labor theory of value is not science … it is a branch of ethics. It represents Marx’s ethical claim about value, and nothing more. But if we admit this arbitrariness, then we admit that the labor theory of value says nothing about the ‘hidden essence of capitalism’. It merely tells us what we already knew: that based on his ethics, Marx thought capitalism was unjust.

The alternative is to claim that Marx’s ‘definition’ of value is not arbitrary, but instead reveals a ‘hidden essence’ of the human mind. That is a bold claim with bold consequences. It implies that all humans are somehow endowed with a ‘value-judging faculty’ that determines value by calculating the labor embodied in a commodity. Supposing this claim is true, many questions arise:

- Is the ‘value-judging faculty’ omnipotent? Is it the equivalent of the neoclassical agent with ‘perfect information’? If so, how do humans acquire this information?

- If the ‘value-judging faculty’ is not omnipotent, does it make mistakes? If so, are they pervasive enough to render the labor theory of value moot?

- How did the ‘value-judging faculty’ evolve? What evolutionary problem did it solve? How long has it been with us?

- Is the ‘value-judging faculty’ encoded at birth? Or is it a product of cultural evolution?

- If the ‘value-judging faculty’ is influenced by culture, do some cultures value labor differently than others? Do some cultures value things other than labor? If so, does this variation undermine the labor theory of value?

- Does the ‘value-judging faculty’ differ between people? If so, why?

- If the ‘value-judging faculty’ is universal, why do capitalists not seem to recognize it? Why don’t they ‘price’ wages using the same method that they price commodities?

- If some people (like capitalists) are able to ignore the ‘value-judging faculty’, does everyone have this ability? If so, when (if ever) is the labor theory of value valid?

Looking closely at these questions, they imply one of two things. Either the human mind is endowed with a remarkably uniform method for judging value, in which case the labor theory of value is a ‘law’ of human nature. Or the human mind does not come with such a faculty, in which case ‘value’ is a complex outcome of culture, and the labor theory of value is false.

We can see, then, why Marxists rarely take the labor theory of value in this direction. Doing so gives the wrong ‘insight’. But while Marxists avoid questions of human nature, a scientific theory of value cannot. That’s because any claim about how human’s judge ‘value’ is also a claim about human nature.

Marx’s mistake was to suppose that value is underwritten by some universal substance. It is not. Instead, what seems likely is that value is the outcome of a rough heuristic. The irony is that it is a heuristic that Marx himself used when formulating his theory. It is the heuristic of egalitarianism. Humans strive for income that is similar to their peers’.

Because this is a loose heuristic, it tells us virtually nothing about the price of individual commodities. But what it does tell us is that across large sections of society, monetary value ought to correlate with labor time. Yes, that is a rather weak claim. But it is the only remaining empirical claim that the labor theory of value makes.

Evidence for the labor theory of value

If the labor theory of value were true, one would expect a striking correlation between prices and labor time. The trouble is, this correlation has always been strikingly absent. Everywhere we look, we find exceptions.

Take art as an example. A painting that took a month to create might sell for $1000. Another month-long painting might sell for $1 million. And when artists die, the price of their art usually goes up, yet the work embodied in their paintings doesn’t change. And speaking of that, why does the price of high art fluctuate wildly with time? The painters are long dead, and the work embodied in their paintings is fixed for all time. What gives? We can dismiss these examples as ‘exceptions’ to the labor theory of value. But if we take that route, we quickly realize that the exception is the norm.

Realizing this problem, Marxists have largely given up trying to test Marx’s claim that commodity prices are proportional to labor time. Instead, they’ve switched to a far weaker test of the labor theory of value. Instead of looking at individual commodities, Marxists look at sectors of the economy.1 And there they find what they are looking for — a striking correlation between value added and labor time.

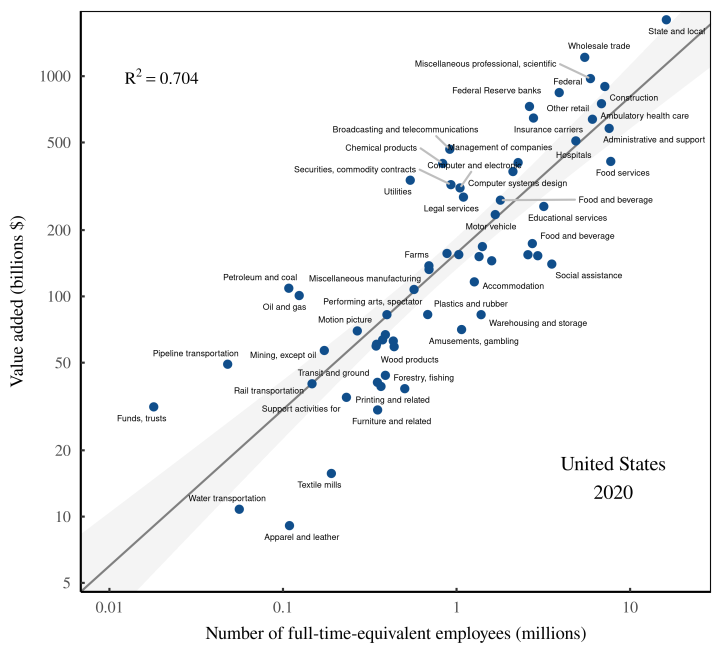

Figure 2 shows an example. I’ve plotted here the correlation between value added and employment across US sectors in 2020. Variation in sector employment explains about 70% of the variation in value added. This strong correlation holds in other years (in the US), and in other countries. It appears to give striking support for the labor theory of value.

Note: Each point represents a US sector in 2020. [Sources and methods]

Bichler and Nitzan balk

Looking at the sector-level evidence for the labor theory of value, political economists Shimshon Bichler and Jonathan Nitzan are unimpressed. The problem, they point out, is that Marx stated that his theory of value applied not to sectors, but to individual commodities.

Now, if prices correlate with labor time at the commodity level, they will also correlate at the sector level. But what about the reverse? If prices correlate with labor time at the sector level, must they correlate at the commodity level?

The answer is no.

To illustrate why, Bichler and Nitzan construct a simple thought experiment, visualized in Figure 3. Imagine that at the commodity level, there is no correlation between prices and labor time. Panel A shows what this lack of correlation might look like (a blob of data with no trend). This commodity-level evidence spells trouble for the labor theory of value. Yet when we look at the sector-level data (Panel C), we find a striking correlation between monetary value and labor time. How can this be?

Note: Panel A plots the labor time and unit price of individual commodities. Since there is no correlation, at the commodity level the labor theory of value fails. Panel B shows sector size (the number of commodities in each sector) plotted against itself. The correlation is (obviously) perfect. When we multiply unit prices and unit prices by sector size, we suddenly get a strong correlation between monetary value and labor time (Panel C). But this results from autocorrelation — sector size correlating with itself. (You can download Bichler and Nitzan’s original presentation of this argument here.)

The answer to this apparent paradox is contained in Panel B. Here I’ve plotted a perfect correlation. It is perfect because it plots the same variable on both axes — the number of commodities produced by each sector. It is this autocorrelation that produces the trend between value added and labor time.

Here’s the math. To get the labor time within each sector, we multiply the number of commodities by the labor time per commodity. But the latter is just statistical noise:

Likewise, to get the monetary value of each sector, we multiply the number of commodities by commodity price. But the latter is just statistical noise:

Notice what happens when we compare monetary value with labor time. We get a striking case of autocorrelation — the number of commodities correlated with itself:

The result, Bichler and Nitzan argue, is that testing the labor theory of value at the sector level tells us nothing about behavior at the commodity level — the level that Marx intended. Any correlation between sector value added and sector labor time could easily be spurious — the result of sector size correlating with itself.

Cockshott’s D-twist

Faced with Bichler and Nitzan’s critique, Marxist political economist Paul Cockshott (and colleagues) responded with an argument that I’ll call the ‘D-twist’. The only valid way to test the labor theory of value, Cockshott claims, is at the sector level. That’s because a commodity-level test violates the principles of ‘dimensional analysis’.

Cockshott’s thinking works as follows. When we compare things quantitatively, they must have the same dimension. This is a measurement truism. Cockshott’s D-twist is to claim that this truism makes it invalid to compare the prices (or labor times) of different commodities.

The reason, he argues, is that all prices come with a different dimension. The price of a pencil has dimensions of $/pencil. And the price of a shirt has dimensions of $/shirt. Faced with these different dimensions, we are not allowed to test the labor theory of value at the commodity level. Dimensions forbid it.

What Cockshott seems not to realize is that this argument does much more than he claims. If we accept his reasoning, it follows that the entire price system is dimensionally invalid. That’s because the purpose of prices is to compare them to other prices. It’s this relative value that gives prices meaning. But according to Cockshott, such a comparison is unsound. By the dictates of dimensional analysis, humans must only compare the prices of identical commodities.

Luckily, no one heeds Cockshott’s advice, because doing so would make prices meaningless. The whole point of prices is to compare the otherwise incommensurable. By virtue of having a price, non-identical commodities are reduced to an identical dimension: money. The purpose of a theory of value is to explain how this reduction happens.

In this light, Cockshott’s D-twist is self-refuting. Cockshott rescues the labor theory of value by arguing that the price system (which the labor theory of value tries to explain) is dimensionally invalid. In his attempt to save the bathwater, Cockshott kills the baby.2

Show me the third factor

After arguing for the ‘D-twist’, Cockshott and colleagues lay out their ground rules for debunking the sector-level evidence for the labor theory of value. If the correlation between labor time and value added is indeed spurious (as Bichler and Nitzan claim), then we must find a third factor that causes the correlation:

The argument that the correlations [between sectoral labor time and value added] are spurious depends on the idea that there exists an independent third factor that is the cause of concomitant variation in the persons and monetary flow vectors. … [F]or an allegation of spurious correlation to be borne out, one must both identify this third factor and show that it actually does induce the correlations observed. So what could this third factor be?

(Cockshott, Cottrell and Valle Baeza, 2014)

At first glance, Cockshott’s argument sounds reasonable. If the correlation between two variables is spurious, we should find the third factor that actually causes the correlation. The problem with this reasoning is that sometimes there is no single ‘third factor’. Instead, there are many ‘third factors’, each of which contributes partially to cause and affect.

Human height is a good example. Suppose that in an effort to explain human height, I measure differences in skeletal length. I find a striking correlation between individuals’ height and the length of their skeleton. I then claim to have explained human height.

You are unimpressed. You respond: ‘The height vs. skeletal-length correlation tells us nothing about why some people are taller than others. It simply restates the data it was given (human height), with some added noise.’

I retort: ‘If my correlation is meaningless, show me the third factor that causes height.’

If you accept my premise, you have lost the argument. That’s because there is no single factor that explains variation in height. Instead, height is a complex outcome of many factors (genes, nutrition, life history, etc.). The same principle is true of prices. Like human height, prices are caused by many different factors. As such, there is likely no ‘third factor’ that explains the correlation between value added and labor time.

On that front, Bichler and Nitzan’s example of ‘spurious correlation’ is a nice thought experiment. But Cockshott and colleagues correctly note that we cannot objectively measure the proposed ‘third factor’ — the quantity of commodities produced in each sector. (Doing so would require an objective dimension for aggregating the various commodities produced by each sector — a dimension that does not exist.)

Having shot down Bichler and Nitzan’s third factor, Cockshott concludes that we must accept the labor theory of value. The reason? Nothing measurable correlates more strongly with value added than does labor time. Case closed.

I don’t buy this argument. While there is no third factor that explains value added, there is a process that does. If we assume that humans are egalitarian, then a value-labor correlation is unavoidable, and the labor theory of value is unnecessary.

The egalitarian heuristic

Let’s assume that the labor theory of value is wrong. If so, why does value added correlate strongly with labor time. The answer, I propose, is because of human egalitarianism.

This idea may seem like a non-sequitor, and in some sense it is. It’s not obvious how humans’ desire for equality would produce a correlation between labor time and value added. But I’m going to show you that it can. The basic idea is that the desire for egalitarianism places (rough) limits on income. And these limits, in turn, put constraints on value added. The result is that unless humans live with oppressive inequality, value added will strongly correlate with labor time.

We’ll get to the math in a moment. But for now, let’s look at some examples of how egalitarianism relates to income. Suppose you hire your friend Alice to paint your house. The job will take about 1 month. How much would you offer to pay her?

Although in principle you could offer any amount, in practice you will not offer her $1 for the job. But why not? One reason is that $1 per month is a starvation wage. Since Alice is your friend, you don’t want her to starve. So you’ll offer her a living wage. I call this sentiment cooperative egalitarianism. When valuing a job done by someone you care about, you offer to pay a wage that is similar to your own.

What about when you buy things from a stranger? Then cooperative egalitarianism becomes less important. Most people won’t low-ball their friends. But many people will low-ball a stranger. Still, if you hire a stranger to paint your house, you’re unlikely to get someone to do it for $1. Why? Because of competitive egalitarianism.

If you ask a neoclassical economist, they’ll tell you that an unemployed person should take any job they can get, since some income is better than no income. But this is not how humans behave. If a job pays far below the social norm, many people will refuse to do it, even if doing so means earning nothing. That’s competitive egalitarianism. Its effect is to put a lower bound on income.

The same principles of cooperative and competitive egalitarianism put an upper limit on income. For instance, few people would offer to pay Alice (the painter) a wage that is hundreds of times their own. And if they did, they’d have a horde of painters at their door offering to do the job for a smaller (but still handsome) sum.

The effect of the egalitarian heuristic, then, is to put a loose bound on income. And this loose bound is all we need to get a strong correlation between value added and labor time.

Exchange without labor, prices without ‘value’

Having proposed the ‘egalitarian heuristic’, let’s look at some evidence of its use. The evidence described below is particularly relevant since it contradicts the labor theory of value.

According to the labor theory of value, monetary value is proportional to labor time. It follows that when people participate in an exchange that has no embodied labor, they ought to price it a zero. But it turns out that humans don’t behave this way. Instead, they use the egalitarian heuristic.

We know this because of a widely-studied scenario called ‘ultimatum game’. It works as follows. The game has two participants, who we’ll call Alice and Bob. To start the game, we give Alice a small sum of money (say $20). Then we ask her to split the money with Bob. Alice makes an offer, which Bob either accepts or rejects. If Bob accepts the offer, the split goes ahead and both participants keep the money. But if Bob rejects the offer, both participants get nothing.

Notice that in the ultimatum game, there is no exchange of labor. (Neither Alice nor Bob do any work.) Hence if both Alice and Bob adhere to the labor theory of value, Alice should offer Bob nothing. Why? Because she knows that Bob has done no labor, and hence, created no value. And Bob knows that he has done no work, and so accepts the offer of nothing.

Unfortunately, when real people play the ultimatum game, they don’t heed this prediction. Instead of offering nothing, the Alices offer the Bobs a (roughly) fair share of the pie. In other words, the participants follow the egalitarian heuristic.

Figure 4 shows the pattern. I’ve plotted here data from Joseph Henrich and colleagues’ seminal study of the ultimatum game. The horizontal axis shows the offer made by the Alices, expressed as a percentage of the original sum. The black points represent the average offer within different cultures. Unsurprisingly, there is variation across societies — an indication that culture affects how people judge value. More surprising is the fact that ultimatum offers clump tightly around an average value of about 40% (as illustrated by the blue density estimate).

Note: The horizontal axis shows offers made by participants in the ultimatum game (the portion of the money the Alices offer to the Bobs). Black points show average offers made within different small-scale societies. The blue curve shows the density estimate. Data is from Joseph Henrich and colleague’s paper ‘Cooperation, Reciprocity and Punishment in Fifteen Small-scale Societies’.

This evidence illustrates the heuristic of ‘cooperative egalitarianism’. Given a sum of money, people offer to split it in a way that is (roughly) egalitarian. The fact that no labor has been done seems to be irrelevant.

Henrich and colleagues also found evidence for what I’ve called ‘competitive egalitarianism’. Every now and then, the Alices would lowball the Bobs, offering them less than 20% of the pie. When that happened, the Bobs rejected the offer about 40% of the time. In other words, these spiteful Bobs would rather take nothing than accept an offer they considered unfair. That’s competitive egalitarianism.

The simplest interpretation of this evidence is that humans don’t judge value based on labor time. Instead, they judge value based on the ethic of fairness.

Accounting for ‘value added’

With the human desire for equality in mind, let’s do some math. I’m going to explain how the tight correlation between value added and labor time can result from egalitarianism.

To make the case, we’ll start with the concept of ‘value added’ itself. The name suggests a contribution to society … as in ‘Bob added value’. That’s no coincidence. Mainstream economists conceive value added as exactly that — a measure of economic contribution. But beneath the sanguine name lies a more banal definition. Value added is really just net income.

‘Value added’ is defined as the difference between a firm’s sales and the expenses it pays to other firms. This is net income by another name. Once paid to the firm, this net income then gets split between the firm’s owners (capitalists) and the firm’s employees (laborers). So value added is the sum of two types of income:

Mathematicians call this kind of equation an ‘identity’, because it is something we’ve defined to be true. It is the definition of value added.

Let’s use this identity to relate value added to labor time. To do so, we’ll split labor income into two components. Labor income is the product of labor time multiplied by the average wage. Noting this fact, we can rewrite our identity as:

Using more compact notation, we can write:

This identity tells us that value added (Y) is proportional to labor time (L), with some statistical ‘noise’ mixed in:

The statistical ‘noise’ is produced by variation in wages (W) and capitalist income (K). In principle, the noise could be huge, and hence drown out the correlation between labor time and value added. But in practice, the noise is negligible. To see why, we must leave the realm of pure mathematics and look at the messy world of human behavior.

A strong signal with weak noise

In mathematical terms, the value-added identity remains valid no matter what numbers we throw in for L, W, or K. But in the real world, these numbers represent configurations of human societies. And human societies cannot take just any form.

Let’s start with labor time L. Interestingly, this is the most arbitrary number in the value-added identity. No, it’s not because human work is itself arbitrary. It’s because here we’re dealing with the labor time within economic sectors, and these sectors have arbitrary boundaries. Some sectors (like ‘wholesale trade’) contain many workers. Other sectors (like ‘pipeline transportation’) contain few workers. This size difference is an artifact of how the various sectors have been defined. But it has an important mathematical consequence — it ensures enormous variation in labor time between sectors.

This labor-time variation is our ‘signal’. It is what will produce the correlation between value added and labor time. But this signal is corrupted by ‘noise’ caused by variation in wages and capitalist income. If the signal is to get through, the noise must be small.

What is key is that this noise is produced by variation in income. And this income variation, in turn, is limited by the human desire for equality. With the US as our example, let’s have a look at this egalitarian heuristic.

The egalitarian heuristic among US workers

In the United States, there is tremendous wage inequality. Superstar employees (such as CEOs) can earn hundreds of times more than minimum-wage workers. But when it comes to the value-added identity (below), it’s not wage differences between individuals that matters. What we care about is wage variation between sectors. That’s what W represents:

This sector variation in wages turns out to be rather small. Figure 5 tells the story. Here I’ve taken the average wage in each US sector (the annual income of a full-time-equivalent employee). Then I’ve calculated the Gini index of these average wages, and plotted the trend over time. Over the last two decades, wage inequality between sectors had an average Gini index of 0.25. On the spectrum of conceivable inequality, that’s quite low.

Note: I have plotted here the Gini index of wage inequality between US sectors. To calculate this index, I input into the Gini formula the average wage in each sector. Inter-sector wage inequality has increased slightly since 1998, but remains low when judged on the 0–1 scale of possible inequality. [Sources and methods]

Returning to our value-added identity, wage inequality between sectors creates noise in the value-labor relation. But in the US, this noise is small.

In other countries, could the wage noise be slightly larger? Almost certainly. But could it be significantly large? That’s doubtful. Given the human desire for income parity, it is extremely difficult to maintain huge wage differences between sectors. Doing so would require barring low-wage workers from moving to high-wage sectors. To some extent, trade guilds create such a barrier. Apartheid regimes do it even better. But unless there is an armed barrier between sectors (i.e. a state border), people will move where the money is, and thus limit inequality. That’s the principle of competitive egalitarianism.

The egalitarian heuristic between US workers and capitalists

When Marx wrote Capital his goal was to explain capitalist income. More specifically, he wanted to explain the capitalist share of income, which he argued was the outcome of class struggle.

Here, I think Marx was on the right track. Unfortunately, he was mute on how this class struggle should play out, other than to claim that it would culminate in the overthrow of capitalism. In most cases, that prediction didn’t pan out. Instead, capitalism has persisted, as has the capitalist share of income.

In the US, for instance, the capitalist share of income has fluctuated between about 5% and 20% of national income (Figure 6). Admittedly, these fluctuations have corresponded to seismic shifts in society. But at least in principle, we can imagine the fluctuations being much larger. There’s no mathematical law that forbids capitalists from taking 90% of income. And yet capitalists seem to take only a small minority of the pie. Why? Marx gives us no answers. But the egalitarian heuristic offers a clue.

Note: The capitalist income share is the sum of before-tax profits and net interest, expressed as a fraction of national income. [Sources and methods]

A defining feature of stratified societies is that there are far fewer elites than there are commoners. The exact ratio is a matter of debate. But in modern societies, capitalist elites makeup about 1% of the population.3 Let’s take this number and see what it implies about individual income.

The income of the average capitalist is proportional to the capitalist share of income (K/Y), divided by the portion of the population who are capitalsts (1%):

Likewise, the income of the average worker is the labor share of income (1

Putting the two equations together, we can see that the capitalist share of income affects inequality between capitalists and workers. For example, if the capitalist share of income is 2%, the average capitalist earns about 2 times more than the average worker. But if the capitalist share of income is 20%, the average capitalist earns about 25 times more than the average worker.

In Figure 7, I’ve plugged these values into the Gini index to illustrate how capitalist-vs-worker inequality varies with the capitalist share of income.4 What’s interesting is that the trend is extremely non-linear. Almost all of the inequality action happens when the capitalist share of income is below 20% — a region I’ve dubbed the ‘class struggle sweet spot’.

Note: This figure plots a model in which I assume that capitalist income flows exclusively to the top 1%. I then measure how the capitalist share of income (horizontal axis) affects inequality between the average income of capitalists and the average income of workers (vertical axis). The vast majority of the inequality action occurs when the capitalist share of income is below 20%, a region I’ve dubbed the ‘class struggle sweet spot’. [Sources and methods]

This simple model gives a plausible reason why the capitalist share of US income has never exceeded 20%. If workers desire equality between themselves and their capitalist peers, then the battle is to keep the capitalist income share below 20% — and preferably much lower. So while the capitalist share of income could (in principle) be anything, in practice, the human desire for egalitarianism limits the capitalist share of the pie to a small minority.

Back to our value-added identity:

Although the identity is true for all conceivable values of capitalist income K, only a tiny subset of these values describe real-world societies. In practice, societies restrict capitalist income so that it constitutes a small portion of total income, Y. And this restriction, in turn, limits the amount of statistical noise between labor time and value added.

The egalitarian heuristic among US capitalists

In Capital, Marx’s favorite character is a fellow named ‘Mr. Moneybags’. He is Marx’s caricature of the money-grubbing capitalist who cares only for profits. This satire has a strong element of truth. The capitalists of Marx’s day (the Vanderbilts, Rockefellers, and Carnegies) did not have a reputation for being generous to workers. Nor, for that matter, do the capitalists of today. So it would seem a bit crass to argue that capitalists (then and now) follow the egalitarian heuristic. But that is exactly what I’ll claim.

The key is that the egalitarian heuristic has two sides: a cooperative side and a competitive side. Most capitalists suppress the cooperative side, at least when it comes to solidarity with workers. But all capitalists vehemently believe in competitive egalitarianism. Indeed, it is the core of their ideology. Capitalists’ goal, Jonathan Nitzan and Shimshon Bichler observe, is to meet (or beat) the normal rate of return. In other words, capitalists want a return that is similar to their peers. That’s competitive egalitarianism.

With this egalitarianism in mind, let’s return to our value added identity:

We’ve already seen that capitalist income K is restricted so that the capitalist share of total income is fairly small. The principle of competitive egalitarianism further restricts this income. Because capitalists try to meet or beat the normal rate of return, the capitalist share of income tends to be quite uniform across sectors.

Figure 8 tells the story. I plot here the results of a 2-step analysis. I first calculate the capitalist share of income (K/Y) in each US sector. I then plug this capitalist income share into the Gini index, and plot its inequality over time. Since 1998, the Gini index has averaged about 0.3. In other words, capitalist margins are fairly equal across sectors.

Note: This figure plots results from a 2-step calculation. In step 1, I measure the capitalist share of value added (K/Y) in each US sector. In step 2, I calculate the Gini index of this income share across all sectors. [Sources and methods]

The effect of this capitalist-income-share equality is to limit noise in our value-added identity. Yes, capitalist income could conceivably be anything. But in practice it is not. The capitalist share of total income tends to be below 20%. And this income share does not vary much between sectors.

From egalitarianism comes a value-labor correlation

We’re now ready to explain the tight correlation between value added and labor time. Marxists argue that this correlation is strong evidence for the labor theory of value. I propose that the correlation stems purely from the egalitarian heuristic.

To test the latter idea, I’m going to throw random numbers into the value-added identity. Then I’ll discard outcomes that are inconsistent with egalitarianism (as we observe it in the United States). I call this thought experiment the ‘random-egalitarian model’.

I’ve explained the model in detail in Box 1. But here’s a quick summary. I start by taking real-world labor times (the sector labor times observed in the US) and putting these numbers into the value-added identity. Then I input random numbers for wages and capitalist income. Next, I look at the distribution of income that results, and discard outcomes that look nothing like the real world. Finally, I measure the correlation between value added and labor time and see what I find.

Box 1: The random-egalitarian model

Randomly generated societies, selected for egalitarianism

- Start with the value-added identity, which relates value add (Y), labor time (L), wages (W) and capitalist income (K). We’ll apply it to each sector s:

- Into Ls, input the actual labor times worked in US sectors in 2020. I measure labor time in terms of the number of full-time-equivalent employees, as shown in Figure 2;

- Generate random numbers for sector wages Ws and capitalist income Ks. (For details about the generation method, see Sources and methods);

- Discard (as follows) outcomes that violate the egalitarian heuristic:

- Discard outcomes in which between-sector wage inequality exceeds a Gini index of 0.3 (the US maximum in Fig. 5);

- Discard outcomes in which the society-wide capitalist share of income (

) is greater than 20% (the US maximum in Fig. 6);

- Discard outcomes in which the capitalist income share (Ks/Ys) has a between-sector Gini index greater than 0.5 (the US maximum in Fig. 8);

- For the societies that remain, measure the sector correlation between value added and labor: Ys ~ Ls.

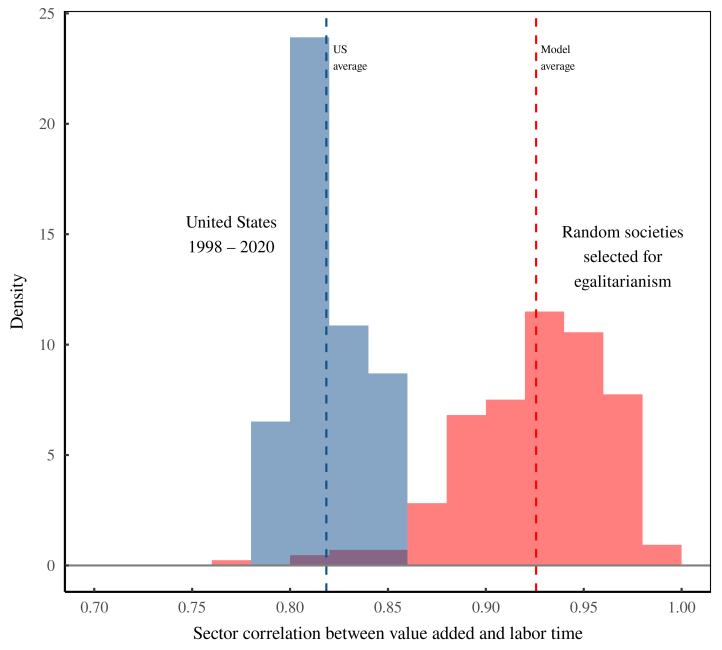

The results of the random-egalitarian model are shown in Figure 9. Let’s break down what you see. I’ve plotted here the outcome of a 2-step calculation. I first measure the sector correlation between value added and labor time in both the random-egalitarian model and the real-world US. The resulting correlation varies over time (in the US) and over different iterations (in the model). Then I take this correlation and plot its histogram, shown in blue for the US and red for the random-egalitarian model.

You can see that on average, the random-egalitarian model produces a value-labor correlation that is stronger than the one found in the United States. And it does so without a labor theory of value. It is merely randomness, selected for egalitarianism.

Note: This figure visualizes a thought experiment in which I test if egalitarianism can create a value-labor correlation. The red histogram shows the results of a model in which I put random numbers into the value-added identity, and then discard outcomes that are non-egalitarian. (See Box 1 for details.) I’ve plotted here the distribution of correlation coefficients for the relation

This result does not bode well for devout Marxists. Contrary to what they claim, the strong correlation between value added and labor time may not be evidence for the labor theory of value. Instead, it could be evidence for a more fundamental feature of human nature: the desire for equality.

If we restrict inequality to a range found in the real world, then otherwise purely random numbers will generate a value-labor correlation … and a strong one at that. The idea that labor creates value is unnecessary.

Selecting against the labor theory of value

Having shown that when we select for equality, a value-labor correlation emerges, let’s now do the opposite. Let’s select for no value-labor correlation and see what happens to inequality. I call this thought experiment the ‘random-anti-Marx’ model. It is ‘anti-Marx’ because in the hypothetical societies that remain, the labor theory of value is overwhelmingly contradicted by evidence.

The random-anti-Marx model starts the same way as the random-egalitarian model. We take our value-added identity and input real-world values for labor time. Then we throw in random numbers for wages and capitalist income. Finally, we select outcomes where value added does not correlate with labor time. Box 2 outlines the steps.

Box 2: The random-anti-Marx model

Random societies, selected so that value added does not correlate with labor time

Repeat steps 1–3 from Box 1.

- Measure the correlation (r) between sector value added and sector labor time

;

- Discard (as follows) outcomes in which value added correlates with labor time:

- Discard outcomes where

;

- Discard outcomes where the correlation p-values are less than 0.5;

- Discard outcomes where

- Observe inequality in the societies that remain.

The point of the random-anti-Marx model is to generate counterfactual societies that do not exist and will never exist. At first, this goal sounds odd. Why would we want to simulate societies that have nothing to do with reality? Because doing so helps us understand why these societies don’t exist.

Think of it as the Sherlock Holmes principle. One way to understand the path taken is to rule out the paths that were avoided:

When you have eliminated the impossible, whatever remains, however improbable, must be the truth.

The random-anti-Marx model gives clear reasons why we always find a value-labor correlation. To understand why, let’s return to our value-added identity:

The question we’re asking is — under what conditions will value added (Y) not correlate with labor time (L)? The mathematical conditions are simple: the ‘signal’ must be drowned out by the ‘noise’.

In our value-added identity, the ‘signal’ is the variation in L (here taken to be variation in the labor time between sectors). The ‘noise’ is the variation in wages (W) and capitalist income (K). As we dial up this noise, we remove the correlation between labor time and value added.5

The purpose of the random-anti-Marx model is to reveal what it takes for value added to be utterly uncorrelated with labor time. The requirements, it turns out, are rather bizarre. I’ll divide them into two scenarios, shown in Box 3.

Box 3: Scenarios in which sector value added does not correlate with labor time.

The fat-capitalist/starving-capitalist scenario:

- There is no value-labor correlation, but wage variation is in a normal range. (Condition: wage inequality between sectors has a Gini index less than 0.3.)

The fat-worker/starving-worker scenario:

- There is no value-labor correlation, but capitalist income is in a normal range. (Conditions: the capitalist share of total income is less than 20%, and the capitalist income share has a between-sector Gini index less than 0.5.)

The fat-capitalist/starving-capitalist scenario

In the fat-capitalist/starving-capitalist scenario, there is no value-labor correlation, but wage variation between sectors is ‘normal’ (meaning it is not more extreme than found in the US). By selecting for these conditions, we create a distribution of capitalist income that is bizarre.

Figure 10 shows what these imaginary societies look like. I’ve plotted here the distribution of the capitalist share of income by sector. The blue histogram is actual US data, which has a familiar bell-curve shape. Capitalist margins clump around an average value of about 15%. In contrast, when we select for a lack of value-labor correlation (alongside a realistic wage distribution), we get a strikingly different pattern. The resulting societies (shown in red) have essentially two types of sectors:

- A ‘fat-capitalist’ sector where capitalist margins verge on 100%;

- A ‘starving-capitalist’ sector where capitalist margins verge on 0%.

Note: The blue and red histograms plot the distribution of the capitalist share of income by sector

The results in Figure 10 tell us why value-added always correlates with labor time: because to imagine otherwise is unthinkable. Killing the correlation between value added and labor time (while keeping a realistic wage distribution) requires a fat-capitalist/starving-capitalist system of income. But such a system violates everything we know about human behavior. It requires that starving capitalists remain idle while their peers reap vast riches.

This scenario is like imagining a herd of cows in which one group is content to starve while the other group gorges itself. Such cows do not exist. And neither do such humans.

The fat-worker/starving-worker scenario

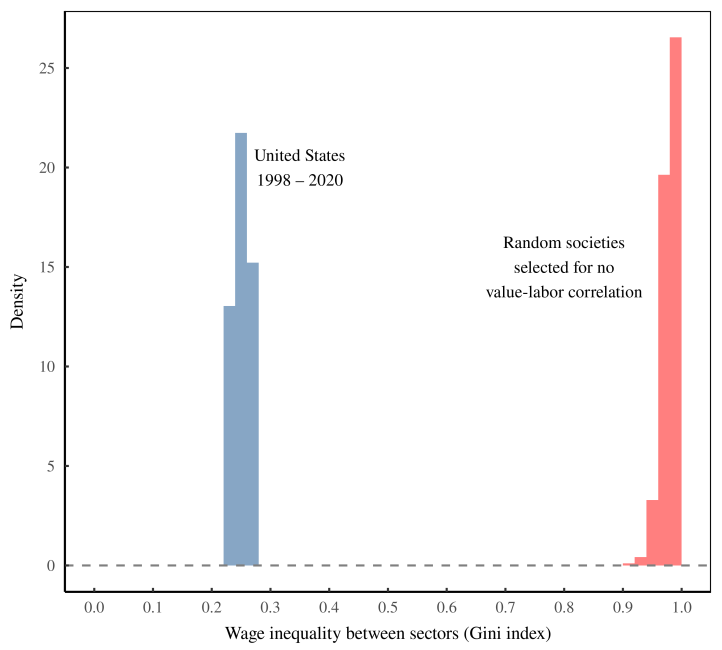

In the alternative scenario, we select for no value-labor correlation, but keep only the societies with a realistic distribution of capitalist income. When we do so, we produce societies with wage inequality that is obscene. Figure 11 runs the numbers.

I’ve plotted here the results of a two-step calculation. I first take average wages in each sector and measure their inequality using the Gini index. Then I plot the distribution of this Gini index. The blue histogram shows the results for the US over the last two decades. Between-sector wage inequality clumps tightly around a Gini index of 0.25.

In contrast, when we kill the value-labor correlation (but keep capitalist income in a realistic range), the resulting wage inequality is extreme (red histogram). The Gini index averages 0.98.

Note: The histograms plot the distribution of wage inequality between sectors. The blue histogram shows actual US values over the last 2 decades. The red histogram shows what happens when we select for societies that lack a value-labor correlation, but have capitalist income within normal bounds. [Sources and methods]

Again, this result tells us why value-added always correlates with labor time: to imagine otherwise is unthinkable. The fat-worker/starving-worker scenario kills the value-labor correlation by making wage inequality more extreme than anything found in the real world.

To give you some context, the most unequal societies on Earth — places like Botswana and Swaziland — approach a Gini index of 0.8. But this is for individual income, not sector averages. Achieving comparable inequality across sectors would mean having a sector of paupers living next to a sector of billionaires. Humans do not tolerate such inequality. And that’s why value added always correlates with labor time.

The tragedy of Marxism

Let’s review. With 150 years of hindsight, it seems clear that Marx’s contribution to science has been largely tragic. The problem is that Marx had two sides, one of which undermined the other.

On the one hand, Marx was an unrivalled empiricist. He was an astute observer of capitalism and a lucid documenter of its abuses and inequalities. And after a decade spent in the British Museum Library, he was a wise (and often riveting) historian. Marx the empiricist made seminal contributions to science.

On the other hand, Marx was also a theorist. It’s here that his work was disastrous. Yes, Marx was wrong … but that’s not the real problem. (Being wrong is part of science.) Marx’s problem was that he framed his ideas in a way that couldn’t be wrong. From the get-go, Marx’s conclusions about capitalism were so seductive that he and his followers forgot to (and often refused to) test their premise.

Marx looked at capitalism and saw a system that, in his eyes, was unjust. Then he took this ethical judgment and encoded it in a theory of value. The result was a seemingly objective way to show that capitalists exploited workers. But it all hinged on a leap of faith — the assertion that labor is value.

In a way, Marx was too clever for his own good. On top of his simplistic assertion about value, he built a towering theoretical edifice that he then wielded to great effect. Marx’s followers took up the mantle and became ‘lords of the labyrinth’6 — masters of wielding Marxist theory without ever questioning its foundation.

When the philosopher Karl Popper looked at the state of affairs in the mid-20th century, he was not impressed. Marxists, he noted, were able to explain anything and everything:

A Marxist could not open a newspaper without finding on every page confirming evidence for his interpretation of history;

… Whatever happened always confirmed [Marxist theory]. Thus its truth appeared manifest; and unbelievers were clearly people who did not want to see the manifest truth …

Popper’s insight was to turn this triumphant attitude on its head. When your theory can accommodate any type of evidence, that’s not a strength. For Popper, it’s a sign that your theory is pseudoscience.

To be fair to Marx, we should distinguish between his theoretical edifice and the foundation on which it rests. The edifice, described by Popper, came to be known as ‘historical materialism’. It’s an approach to understanding history that is so sweeping that it can accommodate almost any sort of facts. At the core of Marx’s theory, though, is a very simple hypothesis about human behavior: we judge value in terms of embodied labor. This hypothesis is easily tested. The problem is that it is immediately falsified.

The funny thing about theories of value is that if you proclaim them ‘universal’, any opposition disproves your point. If labor was the sole source of value, then the labor theory of value should be uncontested. Everyone would agree that labor time is how they judge value. But everyone does not agree. Real-world humans, it seems, judge ‘value’ using many different dimensions. So the labor theory of value appears to be obviously false.

Faced with this glaring problem, Marx had a clever response. Yes, Marx admitted, some people may not equate value with labor. But this fact does not falsify the labor theory of value. It falsifies people’s consciousness. In other words, if you claim to judge value other than by labor time, you’re fooling yourself — you have a ‘false consciousness’.

What Marx seemed to forget is that such a bold claim should be backed by extraordinaire evidence. It’s true that human ideas can be ‘false’. (If I believe that the Earth is flat, I’m wrong.) But what does it mean for human values to be false? If I claim to value trees because they provide shade (not because they have embodied labor), what evidence would prove me wrong? Here we enter the quicksand of human psychology. The thing about values is that there is no external standard for judging them. The mere fact of holding a value makes it true for the person who holds it. Such is the power of ideas.

From the beginning, then, the labor theory of value made nonsensical claims about human psychology. Marxists, however, were undeterred. That’s because they weren’t concerned with understanding the behavior of individuals. They wanted to understand capitalism’s ‘laws of motion’. The tragedy here is that Marx’s rich empiricism could have given rise to a flourishing interplay between evidence and ideas. But that did not happen. Enamoured by Marx’s conclusions about capitalism, his followers decided that the core of Marx’s theory was not a hypothesis. It was a dogma. The task was then to find evidence that supported the conclusion.

It’s in this light that we should interpret the correlation between value added and labor time. Yes, this evidence is consistent with the labor theory of value. But it is also consistent with a much broader theory of human behavior. If humans have evolved to be egalitarian, then a correlation between monetary value and labor time is nearly unavoidable. Indeed, to create a society that lacks a value-labor correlation requires preposterous inequality.

The irony here is that in his writings, Marx clearly espoused the ethic of egalitarianism. The tragedy is that he cloaked this ethic in the facade of objective truth. We are still paying the price for his mistake.

Support this blog

Economics from the Top Down is where I share my ideas for how to create a better economics. If you liked this post, consider becoming a patron. You’ll help me continue my research, and continue to share it with readers like you.

Stay updated

Sign up to get email updates from this blog.

This work is licensed under a Creative Commons Attribution 4.0 License. You can use/share it anyway you want, provided you attribute it to me (Blair Fix) and link to Economics from the Top Down.

Sources and methods

Data for the ultimatum game (Fig. 4) is from Joseph Henrich and colleague’s paper ‘Cooperation, Reciprocity and Punishment in Fifteen Small-scale Societies’.

US income data comes from the BEA, using the tables shown below. I have defined ‘sectors’ to be the smallest unit with available data.

- average wage by sector:

Table 6.6D(annual income per full-time-equivalent worker) - full-time-equivalent employees by sector:

Table 6.5D - value added by sector:

Table: Value Added by Industry - capitalist share of national income:

Table 1.12. (Capitalist income is the sum of net profits and corporate profits before tax.) - capitalist income by sector. Net interest data is from

Table 6.15D. Corporate profit data is fromTable 6.17D. The caveat here is that net interest is reported with less detail (fewer subsectors) than other forms of income. The result is that we know the distribution of capitalist income across sectors with less detail than we know the distribution of value added.

Generating random societies

My simulation assumes that sector value added

Sector labor time

I assume that sector average wages

I let

For each iteration of the simulation, I select

I repeat the simulation millions of times, after which I apply the selection criteria outlined in Box 1 an Box 2.

Notes

- Anwar Shaihk pioneered the method of using input-output tables to measure the total embodied labor used by each sector. Unfortunately, the complication (pointed out by Bichler and Nitzan) is that input-output tables report the flow of money. So to estimate labor time, you must convert monetary flows to labor flows. The problem is that labor time is supposed to predict monetary value, so it would seem invalid to use the latter to estimate the former.↩

- We can also use Cockshott’s dimensional reasoning to ‘invalidate’ physics. According to Einstein, energy and mass are related by the equation

. Imagine that we test this equation by converting different items (cars, pencils, houses, etc.) into pure energy. To see if Einstein’s equation holds, we then compare the change in mass against the change in energy. Lo and behold, the data checks out. Einstein’s equation is correct.

Using Cockshott’s reasoning, however, we can argue that the experiment is invalid. Why? Because we are not minding our dimensions. The different objects we annihilate (cars, pencils, houses, etc.) have different dimensions, meaning any comparison of their mass or energy is invalid.

The reality is that like prices, the whole point of mass and energy is to compare the otherwise incomparable. So if we accept Cockshott’s dimensional argument, we break physics.↩

- The exact number of ‘capitalists’ depends on how we define ‘capitalist income’. Should it include proprietors who are self employed? What about small-scale landlords who earn rent? I follow Nitzan and Bichler in defining ‘capitalist income’ narrowly as the sum of interest and corporate profits. Using this definition, the evidence suggests that virtually all capitalist income goes to the top 1%. For details, see ‘How the Rich Are Different’.↩

- To calculate inequality between workers and capitalists, I use the ‘adjusted’ Gini index, which accounts for small sample size. If the Gini index is

, the adjusted Gini index divides by the maximum possible Gini for the given sample size n:

In the case of inequality between capitalists and workers, the sample size is

, giving a maximum possible Gini index

.↩

- Interestingly, the interplay between signal and noise tells us why Marxists test the labor theory of value at the sector level. One way to counteract the statistical noise is to dial up the signal — variation in L. You do that by looking at swaths of the economy containing vastly different numbers of people. The greater the differences in sector size, the greater your ‘signal’, and hence, the stronger the correlation between value added and labor time.

In contrast, when you look only at consumer commodities, variation in the embodied labor time is small. Because the ‘signal’ is weak, it is easy to drown out. That’s why Marxists have given up testing the labor theory of value at the commodity level. They don’t get the evidence they want.

One way to counteract the signal-noise problem would be to redefine what you mean by a ‘commodity’. To most people, a ‘commodity’ is something small — shoes, shirts, cars, etc. If you want to dial up the labor-time signal, you could expand the concept of the ‘commodity’ to include big infrastructure projects — factories, power plants, roads, etc. By doing so you’d guarantee a price-labor correlation. You’d find that thermo-nuclear power plants are far more costly than pencils, and take far more labor. And by demonstrating this correlation, you would surprise nobody.↩

- ‘Lord of the labyrinth’ is linguist Rudolf Botha’s characterization not of Marx, but of Noam Chomsky. Anthropologist Chris Knight observes:

Botha pictures Chomsky as a skilled fighter at the centre of a vast intellectual labyrinth whose forks and hidden pitfalls are used aggressively to defeat anyone foolish enough to intrude. Nobody ever wins in a battle with ‘the Lord of the Labyrinth’, because the Master makes sure that each contest will take place on terrain which he himself has landscaped and designed.

Marx constructed a similar labyrinth. The best way to critique it is by not entering.↩

Further reading

Cockshott, P., Bichler, S., & Nitzan, J. (2010). Testing the labour theory of value: An exchange. https://bnarchives.yorku.ca/308/

Cockshott, P., Cottrell, A., & Valle Baeza, A. (2014). The empirics of the labour theory of value: Reply to Nitzan and Bichler. Investigación Económica, 73(287), 115–134.

Fix, B. (2020). How the rich are different: Hierarchical power as the basis of income size and class. Journal of Computational Social Science, 1–52.

Henrich, J., Boyd, R., Bowles, S., Camerer, C., Fehr, E., Gintis, H., & McElreath, R. (2001). In search of homo economicus: Behavioral experiments in 15 small-scale societies. American Economic Review, 91(2), 73–78.

Henrich, J., Boyd, R., Bowles, S., Camerer, C., Fehr, E., Gintis, H., … others. (2001). Cooperation, reciprocity and punishment in fifteen small-scale societies. SFI Working Papers, (2001-01-007), 1–9.

Hunt, E. K. (1983). Joan Robinson and the labour theory of value. Cambridge Journal of Economics, 7(3/4), 331–342.

Knight, C. (2016). Decoding Chomsky: Science and revolutionary politics. Yale University Press.

Nitzan, J., & Bichler, S. (2009). Capital as power: A study of order and creorder. New York: Routledge.

Popper, K. (1953). Science: Conjectures and refutations. Philosophy of Science, 104–110.

Shaikh, A. M. (1998). The empirical strength of the labour theory of value. In Marxian economics: A reappraisal (pp. 225–251). Springer.

In Figure 9, you have real US data in red and the randomized society in blue

In Figure 10, you switched the colors so the US is blue.

Not a mistake or anything, but some readers might get caught and confused. I had to do a double take myself. I’m no expert in data representation, but I think there might be a clearer way of presenting it.

LikeLike

Good catch. I’ll have to fix that.

LikeLiked by 1 person

All the stuff about Marx aside, this concept of “competitive egalitarianism” is fascinating. I’d love to read it and see the empiracle work stand without the critique of another ideology. Perhaps next time, I found the attacks on Marxism to be a little distracting from letting your own ideas shine, but if you built it as a responce I definitely see why you would write it this way to start. If you don’t, I’ll have to dig through and review this peice myself later for sure.

As a former Marxist this took me on a trip through memory lane, I even had a debate with Cockshott myself when I was Moderating a FB group of roughly 5,000 socialists https://paulcockshott.wordpress.com/2018/03/06/reply-to-harris/

There are just too many different kinds of marxists and interpretations of Marx to argue against them all. These days, if I mention the LTV at all I like to show the entirety of classical economics and how Labor Value, Exchange Value and Use Value lead up to Marginal Cost, Price and Utility for neoclasical economics. While reading this I felt like ommiting terms like “Exchange Value” or the various other values Marx mentions makes for a misrepresentation, but at the same time I feel its impossible to make an accurate representation of 100+ kinds of infighting marxists. Even if Marx was right it wouldnt matter, we’d have to wait until we rediscover the idea with new words because there is far too much historical baggage.

Anyway, I hope you write about this again without the stuff about LTV bogging it down and giving us recovering radicals war-time flashbacks to debates in OPRIG and arguing with the Trotskyists from Fight Back 😅

LikeLike

Thanks, James. I do hope to explore these ideas further. That said, I’m not sure I would have arrived at the idea of competitive egalitarianism had I not been thinking about the (supposed) evidence for the labor theory of value. So although the idea may stand on its own, it’s really a response to Marx.

LikeLiked by 1 person

Thats totally fair. I really look forward to seeing it again!

LikeLike

Great article Blair, as usual. As someone who’s not a Marxist but has some sympathies with certain parts of Marxism, let me just mention a few things you’re likely to hear, or have almost certainly heard before.

1) A lot of Marxists will vigorously dispute the notion that value is the same thing as price, and they’ll cite a lot of stuff from Volumes I and III in support of their position. My own sense of things is that Marx was vague and loose with his words in many places, to the point where it’s possible to read him in multiple ways (as people have). But I do lean in the direction that the two were not the same thing for him. I don’t think his central goal was ever to explain the nominal domain of capitalism (ie. why do those shoes cost $50 and that ice cream $4?) There’s a brilliant 1974 paper by William Baumol on this (“The Transformation of Values: What Marx “Really” Meant” in Journal of Economic Literature). Baumol was a neoclassical, but also one of the foremost economic historians in the 20th century. And he actually defends Marx in that paper, if you can believe. My own interpretation is similar, in the sense that Marx was trying to uncover the fundamental economic dynamics of capitalism beyond the world of prices. I think, based on what he writes in Volume III, that he would have easily agreed with the CaSP notion that money is a symbolic veil over the world designed to organize hierarchies and institutions. Marx would’ve also situated the nominal domain in the struggle for distribution, which is what Volume III is all about. Now, the problem for Marx is that he didn’t and couldn’t measure things like socially necessarily labor time, so there’s no way to confirm the veracity of his analysis. It’s in this way that his theory is unscientific. In trying to look at the fundamental dynamics of capitalism, he strayed too far from the empirical realm. At least partly.

2) If you’re willing to look past Marx’s silly theoretical pretensions in Volume I, there’s a lot of empirical research he conducted that was truly amazing, especially as he looks at the working conditions in various British industries. And to me it’s that research that’s really valuable, because he’s going over some of the same issues we struggle with today. Again, if you can look past the unjustified bravado on Marx’s part, he’s saying something very simple: capitalists love to boost profits by cutting down on labor costs, and they cut down on these costs by reducing wages and benefits, extending the working day (Chapter 10 is my favorite in Volume I), or decreasing the workforce through automation (and offshoring!). None of this is too controversial, and if Marx had simply let the research speak for itself, without getting bogged down in some metaphysical quest to understand the hidden essence of capitalism, he would have created a much more reliable and scientific work. That’s not the end of the story, of course, because capitalists boost profits in many other ways besides cutting down on labor and production costs (starting with the CaSP idea of their institutional control over property rights). But Marx has a good point nevertheless.

LikeLike

I think we’re mostly in agreement. When I read Capital, I was blown away by Marx’s history of the English enclosures. He was certainly a brilliant analyst of capitalism.

In a sense, my biggest problem is not with Marx, but with what his followers did with his ideas. It’s worth remembering, for instance, that Isaac Newton wrote thousands of pages of garbage about alchemy. His writing about actual physics seems to be in the minority. Fortunately, physicists keep the good and disregard the bad.

With Marx, however, his theoretical ideas seemed to be too intoxicating to keep them in their rightful place as a scientific hypothesis — and a pretty naive one at that. If Marxists had kept what was empirically sound and continued to test their ideas, I’d probably have no problems with the enterprise. But that’s not what happened.

More generally, I’d say that the norm in political economy is for schools of though to be what Lakatos called ‘degenerative’. Truly progressive schools of thought are rare and too often ignored.

LikeLike

Hi Blair,

Thanks for this thought-provoking post. Following our exchange on Twitter, I want to clarify my critique a little.

As noted, I completely buy the argument that the non-occurrence of the random-anti-Marx model entails a human tendency toward egalitarianism. In fact, even though you don’t use the word, yours is a kind of “transcendental” argument in answer to the following question: what must the social world be like for the empirically given distribution of income to be possible? Answer: egalitarian.

Since tendencies often face countervailing forces, they may go unexercised. That’s not a problem for your argument and neither does it make it dogmatic. But a tendency is not merely an accumulation of empirical instances, but an underlying mechanism.

I therefore disagree about the implications your insight has for the famous fact/value dichotomy. If I understand you correctly, your position is that values cannot be falsified. But if the tendency you have so convincingly established is a reflection of a real underlying (sociobiological?) mechanism, then specific inegalitarian behaviors (and the causally efficacious beliefs from which they stem) can be said to belie a basic fact of sociality: egalitarianism. In other words, your central insight allows for a kind of imminent critique, identifying inconsistencies between behaviors and beliefs.

True, no one can falsify you if you value the tree for its shade. But this kind of value, in itself, doesn’t govern the relationship between you and other people. Nor do you specify the practical consequences of holding such a value. Once we speak of values as governing relations between people and as being acted upon, one can apparently falsify values on grounds of internal inconsistency. If, as a consequence of your attitude towards the tree you end up felling it, you are immediately susceptible to an imminent critique. For instance, if the tree you fell is situated in the commons, you have thereby betrayed sociality by not having asked for the consent of others. All the while enjoying the perquisites of sociality elsewhere in life.

I assume this is probably peripheral to your concerns here, but I nonetheless think these far-reaching philosophical implications of your argument should be addressed.

Yigal

LikeLike

Very interesting ideas, Yigal.

I am hesitant to say that egalitarianism is a ‘transcendent’ value of the human species, and that inegalitarianism belies this fact. I personally take a more evolutionary approach.

The reason humans have a strong impulse for egalitarianism, I believe, is that it helps maintain group cohesion. This cohesion, in turn, is helpful when groups compete against one another.

What’s important is that there is an inherent tension between groups and individuals. For the individual, it is advantageous to be inegalitarian and hoard riches. But doing so undermines the group. This pressure limits inequality, but with significant variation. So when we observe that humans are largely egalitarian, we are in effect, observing the result of strong group selection.

While we can’t say that certain values are ‘correct’ or ‘incorrect’, we can say that some are ‘better’ than others in an evolutionary sense. If a certain value system allows a one group to beat another group, the winning value system is ‘better’ and will spread. Unfortunately for those of us wishing to judge values, we can only see the winner in hindsight.

On that note, David Sloan Wilson has been thinking about these issues for a long time. He has a new book out called Atlas Hugged that explores the morality (or lack thereof) of selfishness in an evolutionary light. He wrote it as a kind of hostile sequel to Ayn Rand’s Atlas Shrugged. I’m interested to read it.

LikeLike

Thanks for your response and for the literature recommendation, Blair. I just wanted to clarify one small point.

I’m not claiming that egalitarianism is a transcendent value. I have no insight into the transcendent. I was referring to *transcendental arguments.* These are arguments of the form “what must be the case for X to be possible” (X being any observable phenomenon or activity). It can be viewed as a form of retroductive argument. In your case, egalitarianism is the necessary precondition for the empirically observed distribution of income. One may also add that egalitarianism is the necessary precondition for sociality. In this sense, this argument form should be consistent with the evolutionary approach, or with any other explanatory scientific account.

On your other point, I do see how an individual can gain from being inegalitarian. But only to a point. Because widespread inegalitarianism would erode social relations, thereby making everyone worse off. I suspect this is why egalitarianism tends to ultimately prevail in the course of evolution.

If indeed there is a natural mechanism generating egalitarianism, without which (moreover) sociality and social existence would be impossible, then instances of inegalitarianism would constitute inconsistencies for a social agent. And that is for immanent reasons, not for any transcendent reasons.

LikeLike