| 12 | Accumulation and sabotage |

The truly great fortunes are made only by those who grab hold of the nation’s nervestrings.

—B. Traven, The White Rose

The categories of power

In the introductory chapter to his Grundrisse (1857: Ch. 1), Marx struggles with the difficulty of picking a theoretical starting point. The choice of categories, he points out, is complicated by considerations of abstraction and specificity, as well by questions of historical progression. The capitalist order, like any other social order, enfolds its preceding histories. Each of its categories, Marx observes, embodies not only contemporaneous relations with other categories, but also deep lineages to a past from which it emerged and which it negates.

Our own story of capital focuses on power. But in order to get to power we first had to critique the existing categories, relations and histories of political economy. Common to these theories and explanations is their unwillingness or inability to deal with the power underpinnings of capital. Our journey to explore this difficulty has taken us through various territories: the social myths of Newtonian mechanics; the bifurcation of ‘politics’ and ‘economics’ and the academic splintering of the social sciences; the creed of efficiency and the impossibility of quantifying productivity; the distinction between the ‘real’ and the ‘nominal’ and the tortured relationship between tangible wealth and financial markets; and, finally, the history of capitalization from Middle-Age discounting to present-day asset pricing.

Capitalization stands at the centre of contemporary capitalism. The discounting to present value of expected future earnings is now the organizing ‘economic’ principle that shapes and directs daily life on our planet. But as our journey has repeatedly suggested, capitalization is not merely an ‘economic’ category. It is an encompassing mode of power.

Until the emergence of capitalism, power was largely separate from and situated above the processes of production and consumption. It was administered by large doses of force sprinkled with small promises, mostly for after life fulfilment. The new regime of capital introduced a whole new technology of power, one that penetrates and shapes the very souls of its subjects. It invented the concept of ‘ideology’ and the institution of ‘public education’; it developed mass psychology, mass culture and mass consumption; it gave rise to a one-dimensional man; it opened up domains that prior rulers could not even fathom. These inventions have made capital the most invasive, encompassing and flexible form of organized power ever known to humanity. And since these power processes all bear on profitability and therefore are all discounted into asset prices, to study capitalization is to study the nature and evolution of organized power in contemporary capitalism.

Thus, our starting point in this part of the book is that the capitalization of earnings is not a narrow offshoot of production but a broad representation of power. Pecuniary earnings, we argue, do not have a material ‘source’, whether counted in utils or labour time. Instead, they are the symbolic representation of a struggle — a conflict between dominant capital groups, acting against opposition, to shape and restructure the course of social reproduction at large. In this struggle, what gets accumulated is not productivity as such, but the ability to subjugate creativity to power.

Theorizing this capitalized struggle, however, is anything but trivial. The immediate problem, again, is the categories themselves. Nowadays, almost every concept that pertains to capital embodies or connotes production and consumption. The notions of ‘business’ and ‘industry’, ‘investment’ and ‘private ownership’, the ‘normal rate of return’ and the ‘natural rate of unemployment’, ‘commodity pricing’ and ‘wealth maximizing’, ‘equity’ and ‘debt’, ‘profit’ and ‘interest’, the ‘corporation’ and its ‘material’ and ‘immaterial’ assets, ‘accumulation’ and ‘circulation’, and, finally, the so-called ‘fractions’ of capital — are all articulated, understood and used as economic entities.

This prejudice may serve neoclassical and Marxist arguments, but it undermines our own: given our focus on power, the ‘economic’ bias of these concepts makes it impossible for us to use any of them ‘as is’. And so, just as Marx had to peer through the voluntary equivalences of liberalism in order to articulate exploitation, we too find ourselves having to tear through the economic language of capital in order to see the real picture of capital as power.

And the task is certainly tricky. On the one hand, we need to translate the existing categories, one by one and in relation to each other, so that slowly, out of the façade of material productivity there can emerge the power nature of capital. On the other hand, we must keep in mind the conventional meaning of these categories, so that we can refer to prevailing explanations and measures. And then there are several ideas that require new categories altogether.

A new language can easily be misunderstood, so we tread as carefully as we can. We articulate our argument at length, in detail and with occasional repetition — and we ask our reader to suspend judgement. You are likely to find the argument easier to assess when you reach the end of our story.

Perhaps the first attempt to develop a power theory of capital was offered at the turn of the century by Thorstein Veblen. Later, his student and colleague, Lewis Mumford, expanded some of Veblen’s themes into a sweeping theory of power civilizations. Both frameworks build on the primal interaction between creativity and power. Veblen, whom we deal with in the present chapter, associated this interaction with a distinction between industry and business. Mumford, to whom we turn in the next chapter, saw this interaction as part of a conflict between democratic and totalitarian technologies. Their profound insights, unduly neglected by political economists, deserve closer scrutiny and offer bases for further development.

Veblen’s world

Veblen’s view stood in sharp contrast to the utilitarian dogma of his day. While his neoclassical peers preached the gospel of hedonic pleasure and equilibrium as the governing mechanism, or at least the underlying ideal, of all societies, Veblen focused on conflict. Unlike Marx, though, he emphasized not only the conflict between owners and non-owners, but also what he saw as a broader clash between creativity and power. In his opinion, this wider conflict pervades all societies, appearing in different guises at different times. In the modern capitalist order, it takes the form of a fundamental distinction between industry and business.

Industry and business

For Veblen, industry and business are two increasingly distinct spheres of human activity. Industry constitutes the material context of capitalism, although industry is not unique to capitalism. When considered in isolation from contemporary business institutions, the principal goal of industry, its raison d’être according to Veblen, is the efficient production of quality goods and services for the betterment of human life. The hallmark of industry is the so-called ‘machine process’, a process that Veblen equated not merely with the use of machines, but more broadly with the systematic organization of production and the reasoned application of knowledge. Above all, Veblen accentuated the holistic nature of industry. The neoclassical emphasis on individualism and its Robinson Crusoe analogies of the innovative ‘entrepreneur’ and single ‘consumer’ are misleading myths. The machine process is a communal activity; its productivity derives, first and foremost, from cooperation and integration. The reasons are both historical and spatial.

First, modern industrial production is contingent on what Veblen called the ‘technological heritage’ of society, the general body of ‘community knowledge’ grounded in the ‘accumulated wisdom of the past’ (Veblen 1908: 326–29). Second, over time the gradual accumulation of knowledge makes production more spatially interdependent. ‘Evidently’, writes Veblen ‘the state of industrial arts is of the nature of a joint stock, worked out, held, carried forward, and made use of by those who live within the sweep of the industrial community. In this bearing the industrial community is a joint going-concern’ (1923: 64). Following Werner Sombart, he emphasized the comprehensive and encompassing nature of industry, in that it ‘draws into its scope and turns to account all branches of knowledge that have to do with the material sciences, and the whole makes a more or less delicately balanced complex of sub-processes’ (1904: 7–8).

Given this growing interdependency of both knowledge and processes, says Veblen, the efficiency of industrial production increasingly hinges on synchronization and standardization of both production and wants (an issue resurrected half a century later by Galbraith with his ‘revised sequence’ and attack on ‘consumer sovereignty’). As a highly integrated system, industry is strongly disposed toward elaborate planning and close cooperation. Ultimately, it calls for ‘solidarity in the administration of any group of related industries’ and, more generally, ‘for solidarity in the management of the entire industrial traffic of the community’ (Veblen 1904: 17).

Although Veblen’s emphasis on integration and synchronization hardly seems earthshaking, mainstream and to some extent Marxist economists have systematically managed to ignore two of its key implications. One implication of integration and synchronization is that distribution cannot possibly be based on individual factor productivity or atomized labour time. Consequent to this conclusion, the other implication is that distribution should be sought in the realm of power.

This is where business comes into the picture. According to Veblen, business differs from industry in both methods and goals. Business enterprise means investment for profit.162 It proceeds through purchase and sale toward the ulterior end of accumulated pecuniary wealth. While industry is a manifestation of the ‘instinct of workmanship’, business is a matter of ownership and power; whereas the former requires integration, cooperation and planning throughout society, the latter depends and thrives on conflict and antagonism among owners and between owners and the underlying population.

The two languages

These profound differences have crystallized into two separate languages. Unlike industrial activity, with its tangible, material categories, business traffic and achievements are counted strictly in pecuniary terms. Economists insist on reducing ‘nominal’ business magnitudes to ‘real’, utilitarian units, though that insistence merely attests to their pre-capitalist habit of thinking. As we have seen earlier in the book, this reduction is impossible to achieve. But even if the conversion proved feasible, according to Veblen the capitalists couldn’t care less. Under the price system, he pointed out,

men have come to the conviction that money-values are more real and substantial than any of the material facts in this transitory world. So much so that the final purpose of any businesslike undertaking is always a sale, by which the seller comes in for the price of his goods; and when a person has sold his goods, and so becomes in effect a creditor by that much, he is said to have ‘realized’ his wealth, or to have ‘realized’ his holdings. In the business world the price of things is a more substantial fact than the things themselves.

(Veblen 1923: 88–89, emphases added)

The pecuniary nature of business terminology is not a mere accounting convention; it is the very gist of business enterprise.

At first sight, Veblen’s separation between industry and business seems to resemble Marx’s distinction between simple reproduction of use value (C ⟶ M ⟶ C) and expanded reproduction of exchange value (M ⟶ C ⟶ M′) — the former representing the life cycle of the workers/creators, the latter of the capitalists/rulers. There is a crucial difference, however. Marx used a single material unit — abstract labour — to measure both processes. By contrast, Veblen began at the outset with two distinct categories: heterogeneous material units for industry and a universal pecuniary unit for business. This duality enabled him to avoid the Marxist Transformation Problem altogether: prices and accumulation are business magnitudes, and hence their determination cannot be attributed, at least not in any straightforward way, to the complex and largely intractable sphere of industrial interactions.

According to Veblen, unlike industry in the abstract, capitalist industry is subordinated to business ends; its aim is no longer serviceability and livelihood, but profit. Simple as it seems, this hierarchy inverts conventional economic reasoning. Being a quest for profit, argues Veblen, business enterprise is a claim on pecuniary earnings. It is wholly and only an act of distribution. The objects over which profits constitute an effective claim are created elsewhere, in the industrial sphere (as well as in nature). Yet, given that capitalist industry is carried on for the sake of business, it follows that the primary line of causality runs not from production to distribution, but from distribution to production. And if causality is a guide for analysis, the study of capitalism should begin with business, not industry.

Indeed, on its own, industry provides no insight into distribution. Anticipating and dismissing the Cambridge Controversy more than half a century before it arose, Veblen pointed out quite bluntly that J.B. Clark’s marginal productivity theory was wishful thinking. In order to explain distribution by productivity, we must first identify the productivity of each individual factor of production. Yet this identification, he said, could not be achieved because the so-called economic inputs did not possess any individual productivity to begin with.

The immaterial equipment

As already noted, Veblen viewed industrial activity as an integrated community process centred on the ‘technological heritage’ of society. On the surface, this view may look similar to prevailing convictions, popular since Galbraith (1958; 1967), that emphasize the growing significance of technology vis-à-vis the traditional factors of production — i.e. land, labour and capital.

That is not what Veblen had in mind, however. In his opinion, technology — or the ‘immaterial equipment’ of society, as he liked to call it — was not just another ‘factor of production’, however important. Instead, it was the vital cultural substance that made raw materials, machines and physical human labour useful in the first place: ‘To say that these minerals, plants and animals are meaningful — in other words, that they are economic goods — means that they have been brought within the sweep of the community’s knowledge of ways and means’ (Veblen 1908: 329). Without this ‘immaterial equipment’, he argued, the physical factors of production were economically meaningless objects.

For instance, the usefulness of any given computer depends crucially on the current state of technology. With the arrival of new software, the hardware quickly ends up in the junk heap; the new technology makes it socially obsolete, and although it may have lost none of its operational features, it is no longer a ‘capital good’. Or rolling history in reverse, a modern factory producing semiconductors would have been a worthless (and indeed meaningless) collection of physical objects during Veblen’s time — first, because it could not have been operated; and second, because its output would have had no perceptible use. In these and all other cases, the transformation of a physical object into an economically useful capital good can neither lead nor lag the existing ‘state of industrial arts’. The same logic applies to labour power and raw materials. A jungle tribesman would be lost in a modern factory, much as a bank manager would be lost in the Sahara desert. Similarly, ancient stone utensils are as useless today as was petroleum before the invention of modern combustion engines.

Labour, land and capital goods are obviously essential for production, but only because they are part of a comprehensive social and cultural process. It hence ‘seems bootless to ask’, argued Veblen, although few neoclassicists were listening, ‘how much of the products of industry or of its productivity is to be imputed to these brute forces, human and non-human, as contrasted with the specifically human factors that make technological efficiency’ (1908: 349–50). In short, as the industrial system grows in complexity, the productivity theory of distribution becomes an oxymoron.

To illustrate the ‘holistic’ nature of contemporary industry, consider the automobile sector. Its research and development process incorporates knowledge from fields as diverse as mathematics, physics, chemistry, biology, metallurgy, economics, demography, sociology and politics. Its production relies on coordinating the interaction of raw materials, labour, assembly facilities, infrastructure, transportation and distribution systems in numerous countries. Finally, development, production and consumption are all path-dependent. For example, the emergence of large-scale petroleum refining, suburbanization and the highway system accelerated automobile production in the twentieth century, while congestion and environmental limits will likely hinder it in the twenty-first.

In this increasingly complex context, with technology being temporally cumulative, spatially interdependent and intermingled with politics, it is practically impossible as well as theoretically inconceivable to even identify all ‘inputs’, let alone determine their separate productive contributions. And that is merely the first step.

The hand of power

Our automobile example shows that the industrial process is comprehensive and integrated. But that in itself does not make it ‘efficient’. The added difficulty emerges because, according to Veblen, industry is subjugated to business. The compass that directs the production of automobiles in our example is corporate earnings — yet contrary to the various doctrines of political economy, says Veblen, these earnings depend not on efficiency, but on ‘sabotage’. Most generally, the income of an owner is proportionate not to the specific productive contribution of his or her input, and not even to the exploitation of productive workers — but rather to the overall damage that an owner can inflict on the industrial process at large.

The implication is that every bit of the industrial process is touched by the hand of power. In the case of automobile production, every aspect — from environmental considerations, suburbanization and the highway system, through the global coordination of manufacturing and the conditioning of workers and consumers, to the development process and the basic science — is intermingled with power. And so, even if we were somehow able to miraculously conjure up the distinct connections between these many ‘inputs’ and their automobile ‘output’, the result would reflect not productivity per se, but the control of productivity for capitalist ends.

From this viewpoint, it is impossible to speak of a depoliticized economy as the liberals do, or of a separation between economic exploitation and political oppression as the Marxists articulate. The basic distinction, rather, is between power and creativity, and the task is to analytically disentangle their specifically capitalist incarnations of industry and business.

Absentee ownership and strategic sabotage

The natural right of investment

Over the long term, argued Veblen, output depends mostly on the size of the population and the scope of the industrial arts; ‘tangible assets’ are relatively insignificant. Throughout history, the occasional destruction of material equipment and resources has usually been a relatively minor inconvenience. In Ireland, for example, the encouragement of illiteracy by the British occupiers hindered development much more effectively than the destruction of the country’s infrastructure. Even in the twentieth century, when physical accumulation had reached unprecedented levels, it took war-stricken Germany and Japan only a few years to launch their ‘economic miracles’.

In the short term, however, tangible equipment is significant, and it is here, according to Veblen, that ownership comes into the picture:

For the transient time being, therefore, any person who has the legal right to withhold any part of the necessary industrial apparatus or materials from current use will be in a position to impose terms and exact obedience, on pain of rendering the community’s joint stock of technology inoperative for that extent. Ownership of industrial equipment and natural resources confers such a right legally to enforce unemployment, and so to make the community’s workmanship useless to that extent. This is the Natural Right of Investment.

(Veblen 1923: 65–66, emphasis added)

A modern reader may find this definition of investment puzzling, so it is perhaps useful to put the term in historical context. Originally, the meaning of ‘investment’ had nothing to do with money and even less to do with production. Investment was a matter of power, pure and simple. Investio in Latin means ‘to dress’, and in Europe of the Middle Ages it was a signifier of feudal property rights. Lords would typically give their vassals a suit of clothing — or vestes — as part of their keep and as a sign of honour. The symbolic ceremony of transferring property rights from the lord to the vassal was known as investiture. The property in question could have been an estate, an office, a monastery, or simply a stipend (feodum de bursa). The ceremony ‘vested’ the vassal with the fief, conferring on him tenure or seisin — a legal seizure protected against invasion from any quarter (Bloch 1961: 173, 349; Ganshof 1964: 97, 126). According to the Oxford English Dictionary, the word ‘investment’ entered commercial use only in the early seventeenth century with the East India trade, and its contemporary connotation of converting money capital into tangible income-yielding assets appeared only in the middle of the eighteenth century.

In other words, throughout the early history of the term, the causal link ran not from the creation of earnings to the right of ownership, but from vested ownership to the appropriation of earnings. And according to Veblen, the same principle continues to hold in the capitalist epoch. ‘Capital goods’ yield profit not because of their individual productivity, but because they are privately owned to begin with — that is, owned against others.

Private ownership and institutionalized exclusion

How does private ownership ‘generate’ earnings? By necessity, every social order is created and sustained through a certain mixture of cooperation and power. In simple egalitarian societies, cooperation was paramount; in capitalism, power is the governing principle. The power principle of capitalism is rooted in the centrality of private ownership. The word ‘private’ comes from the Latin privatus, meaning ‘restricted’, and from privare, which means ‘to deprive’. As Jean-Jacques Rousseau tells us, ‘The first man, who, after enclosing a piece of ground, took it into his head to say, “This is mine”, and found people simple enough to believe him, was the true founder of civil society’ (Rousseau 1754: Part III).

The most important feature of private ownership is not that it enables those who own, but that it disables those who do not. Technically, anyone can get into someone else’s car and drive away, or give an order to sell all of Warren Buffet’s shares in Berkshire Hathaway. The sole purpose of private ownership is to prevent us from doing so. In this sense, private ownership is wholly and only an institution of exclusion, and institutional exclusion is a matter of organized power.

Exclusion does not have to be exercised. What matters is the right to exclude and the ability to exact terms for not exercising that right. This right and ability are the foundation of accumulation. Business enterprise thrives on the implicit threat or explicit exercise of power embedded in ownership, with capitalist income being the ‘ransom’ for allowing industry to resonate:

Plainly, ownership would be nothing better than an idle gesture without this legal right of sabotage. Without the power of discretionary idleness, without the right to keep the work out of the hands of the workmen and the product out of the market, investment and business enterprise would cease. This is the larger meaning of the Security of Property.

(Veblen 1923: 66–67, emphasis added)

Of course, the role of power is hardly unique to capitalism. According to Veblen, all forms of ownership are based on the same principle of coercive appropriation, which in his view dates back to the early stages of barbarism and the initial emergence of predatory social customs. The differentiating factor, he says, is technological: the institutionalization of forceful seizure is intimately linked to the nature of tangible implements and to their relative significance in production. In the earlier stages of social development, forced appropriation was limited because there was little to appropriate and most objects were easily replaceable. But as society’s ‘immaterial assets’ started to accumulate, so did the benefit from controlling its key ‘material assets’.

The right to property

The first form of property rights, according to Veblen (1898; 1899a), was the ownership of people, particularly women. Etymologically, the English word ‘husband’ and the Mesopotamian word ‘baal’ both share the double meaning of ownership and marriage — and, in the latter case, also sexual exploit and the superior male-god of the west-Semitic pantheon.165

Subsequently, the focus of ownership shifted (although not necessarily linearly) from slaves, to animals, to land. The specific trajectory depended on the nature of technological development, and it was only recently that it moved primarily to produced means of production.166 Notably, prior to capitalism neither slave ownership nor landed wealth were ever justified on grounds of productive contributions; both were institutionalized as a ‘right’ — by virtue of divine will or sheer force, but never as a consequence of creativity.

Now, clearly, the mere ownership of capital is no more productive than the ownership of slaves or land, so why do economists insist it is?

The answer, according to Veblen, is that economic theory had been unduly influenced by the transitory institutions of handicraft that existed during the transformation from feudalism to capitalism. Common sense suggested that craftsmen, working for themselves with their own material appliances, had a ‘natural right’ to own what they had made; it also implied that they could dispense with their product as they saw fit — that is, sell it for an income.167 Handicraft and petty trade thus helped institutionalize pecuniary earnings as a natural extension of ownership-by-creativity. With exchange seen as a ‘natural right of ownership’, the very earning of income became a proof of productivity.

But this common sense is misleading for two reasons. First, even at the handicraft stage, production was an integrated societal process. Thus, despite the myth of ‘individualism’, private ownership was at least partly dependent on the dynamics of organized power (with the exclusionary practices of guilds offering a conspicuous illustration). Second, and more significantly, the institutions of handicraft were short-lived. As Veblen pointed out, technical change ushered in by the onset of the industrial revolution meant that production had to be conducted on a large scale, which in turn implied the progressive separation of ownership from production.

The absentee ownership of power

During the earlier stages of capitalism, production and business were still partly interwoven.168 Indeed, even as late as the nineteenth century, US ‘cap tains of industry’ such as Cornelius Vanderbilt and Andrew Carnegie were seen as creative forces, acting as master workmen as well as astute businessmen. This duality did not last for long, however, and as business became increasingly separate from industry, the implication was no less than pro found. Gradually, capitalism came to mean not merely the amassment of ‘capital goods’ under private ownership, but more profoundly a division between business and industry affected through the rise of absentee ownership.

The institution of absentee ownership has altered the very nature and meaning of capital. Not unlike the European lords of the Middle Ages, who gradually withdrew from the direct management of their estates, modern capitalists have become investors of ‘funds’, absentee owners of pecuniary wealth with no direct industrial dealings.

The complete delinking of capital from ‘capital goods’ is well illustrated by comical extremes. In the summer of 1928, the world’s largest oil companies signed the secret Red Line Agreement, parcelling the Middle East between them for years to come. To celebrate the occasion, the architect of the deal, Calouste Gulbenkian, or ‘Mr Five Percent’ as he was otherwise known, chartered a boat to cruise the Mediterranean with his daughter Rita:

Off the coast of Morocco, he caught sight of a type of ship he had never seen before. It looked very strange to him, with its funnel jutting up at the extreme stern of the long hull. He asked what it was. An oil tanker, Rita told him. He was fifty-nine years old, he had just made one of the greatest oil deals of the century, he was the Talleyrand of oil, and he had never before seen an oil tanker.

(Yergin 1991: 206)

This illustration is not an outlier. Currently, roughly half of all capitalist assets are owned indirectly through institutional investors such as pension and mutual funds, hedge and sovereign funds, insurance companies, banks and corporations. The ultimate owners of these assets, whether big or small, exercise little voice in the management of the underlying production processes. For the most part, they merely buy and sell shares of these assets and collect the flow of dividends. Often, their diversification is so extensive that they don’t know exactly what they own. And that characterization is by no means limited to portfolio owners. Many of the largest direct investors — including the capitalist dons whose names populate the Forbes listing of the superrich — are equally removed from any industrial dealings. Most of their energies are spent on the high politics of sabotage and the fine art of cutting and pasting assets through endless deals of divestment and merger — activities that they commonly carry out, just like Gulbenkian, without ever seeing a single ‘capital good’.

Whereas most economists continue to view capital as an amalgamation of machines, structures, semi-finished commodities and measure-of-their-ignorance technology, for the business investor capital has long been stripped of any physical characteristics. In the eyes of modern owners — whatever their gender, colour, religion, sexual inclination, ethnicity, culture, nationality, creed, height, weight or age — capital means one thing and one thing only: a pecuniary capitalization of earning capacity. It consists not of the owned factories, mines, aeroplanes, retail establishments or computer hardware and software, but of the present value of profits expected to be earned by virtue of such ownership.

Of course, neoclassicists have never had a quarrel with capital as the present value of future earnings. In the long run, they assure us, demand and supply make this present value equal to the cost of producing that capital (assuming competitive markets, perfect foresight and the rest of the hedonic fairy tale). But as Veblen (1908) acutely observed long before the Cambridge Controversy (and as we have seen in Part III), this explanation was logically faulty from the very start. If capital and capital goods were indeed the same ‘thing’, he asked, how could capital move from one industry to another, while capital goods, the ‘abiding entity’ of capital, remained locked in their original position? Similarly, how could a business crisis diminish the value of capital when, as a material productive substance, the underlying capital goods remained unaltered? Or how could existing capital be denominated in terms of its productivity, when technological progress seemed to destroy its pecuniary value?

For Veblen, the answer was straightforward: capital simply is not a double-sided entity. It is a pecuniary magnitude, and only a pecuniary magnitude, and its magnitude depends not on the capacity to produce but the ability to incapacitate. In the final analysis, the modern capitalist is nothing more than an absentee owner of power.

Strategic sabotage

What exactly is this power to incapacitate? Where does it come from, what form does it take, and how does it yield profit? According to Veblen, the answer remained obscure partly because the historical consolidation of capitalist property rights slowly substituted ideological manipulation and legal authority for brute force and religious sanctity.

With the twin emergence of the modern corporation and the modern state, capitalism has acquired a ‘civilized’ face: absentee ownership has become a legitimate norm; open violence has been replaced by latent threats underwritten by hefty advertising budgets, bloated security services and overflowing jails; and power has solidified into a mystical structure (at least for those subjected to it). In this new order, the power to incapacitate — or ‘sabotage’ as Veblen liked to call it — becomes a fully legitimate convention, carried out routinely and invisibly through the very subordination of industry to business. The blueprints of capitalist production are already programmed for business limitation, its hired managers are schooled in the art of invisible restriction, and its top executives are remunerated in proportion to profit. In order to merely earn the normal rate of return, all the owner has to do is own.

But then where is the ‘sabotage’? Is it not true that in order to profit, business enterprise needs to promote industrial creativity, productive ingenuity and ‘best practices’? The answer is not really. Strictly speaking, business cannot ‘promote’ industry. At most, it can unleash it — and even that it does only up to a point and under very specific conditions. Earnings do depend on output — but not on any type of output and not only on output. Moreover, the dependency is non-linear and sometimes inverted, which is why Veblen referred specifically to strategic sabotage.

Seen as an entire social order, business enterprise certainly is far more ‘productive’ than any earlier mode of social organization.169 Yet, in Veblen’s opinion, the immense productive vitality of this social order is an industrial, not a business phenomenon. Business enterprise is possible only in conjunction with large-scale industry, though the reverse is not true (as illustrated by socialist industry or giant cooperatives such as Mondragon). The practices of business of course are closely related to industry, but only in point of control, never in terms of production and creativity. From this a priori vantage point, business per se is distinct from industry and therefore cannot boost industry, by definition. Even companies in possession of cutting-edge technology cannot promote industrial creativity; instead, they can merely relax — usually for a hefty fee — some of the constraints that would otherwise limit creativity.

This interpretation of the hyperproductivity of capitalism is quite different from that of Marx. In our view, Marx was correct to stress the dialectical imperative of technical change, an emphasis that the evolutionist Veblen preferred to disregard. Over the longer haul, capitalists indeed find themselves compelled — and in turn force their society — to constantly revolutionize the pattern of social reproduction. They continually ‘invest’ in having industry develop for them new methods and products and in expanding their capacity to produce them. Yet all of this they do in the expectation of adequate differential returns, and differential returns are possible only through restriction.

‘Free is not a business model’, explains the representative of eBay China (Dickie 2006). Money spent on having your engineers invent open-source technology or on making your workers create physical capacity that everyone can freely use is money gone down the drain. The only way such spending can become a profit-yielding investment is if others are prohibited from freely utilizing its outcome. In this sense, capitalist investment — regardless of how ‘productive’ it may appear or how much growth it seems to ‘generate’ — remains what it always was: an act of limitation.

The direction of industry

The limitation takes two general forms. The more important — but also more elusive and harder to delineate — concerns the very direction of industrial development. This restriction, of course, is hardly unique to capitalism, being inherent to the very development of any system of hierarchical production.

According to the historical evidence marshalled by Stephen Marglin (1974), rulers almost invariably fight to impose techniques that secure and amplify their power — often at the expense of efficiency (conventionally measured). This was true when the Romans forced slaves into brick and pottery ‘factories’ — just as it was true when European feudal lords imposed water mills and prohibited hand mills, when post-bellum American planters forced a credit-based system of share-cropping on small farmers, and when Stalin collectivized Soviet agriculture. The purpose of these technological impositions, Marglin argues, was ‘divide and conquer’. And in his opinion, the same remains true with capitalist production: this is why British capitalists retained demonstrably inefficient mining techniques, why they introduced the factory system well before the arrival of machines, and why they insisted on a minute division of labour that was debilitating to the point of becoming technically counterproductive.

At first sight, this capitalist imposition of inefficiency may seem surprising, if not counterintuitive. After all, capitalists seek profit, profit increases as cost falls, and cost falls as efficiency rises — so isn’t it in capitalists’ best interest to adopt the most productive techniques? What exactly is the point of increasing power if the end result is lower profit? The question may sound biting — but it is the wrong one to ask. In fact there is no contradiction at all: in reality, power means not less profit but more profit.

The confusion is easy to sort out. The idea that profit maximization necessitates cost minimization and that cost minimization requires efficient production holds only in the fairy tale of perfectly competitive equilibrium. In this fictitious context, where prices and wages are set by mother market to equilibrate marginal productivity and utility, it certainly makes sense for the ‘representative’ capitalist to adopt the most efficient techniques.170

But once we get rid of the fiction and move to the real world where prices represent not utility and productivity but power, these imperatives immediately break down on their own terms. ‘Productive efficiency’ (minimum inputs per unit of output) no longer implies ‘economic efficiency’ (minimum cost per unit of output), and ‘economic efficiency’ no longer means ‘maximum profit’. In this imperfect context, it makes perfect sense for capitalists to impose ‘inefficient’ techniques: their very inefficiency is the power leverage through which profits are generated.

Let’s illustrate this principle with more contemporary examples. Take transportation. On the face of it, a well-designed public transit seems much more conducive to human welfare and the natural environment than private transit. Yet, in the US and elsewhere, capitalist transportation has tended to move away from the public and toward the private. And the reason is not hard to grasp. Public transportation resonates with the integrated operation of industry and therefore doesn’t sit well with regular flow of business profit.

This is perhaps the reason why early in the twentieth century the automobile companies bought and dismantled 100 electric railway systems in 45 US cities (Barnet 1980: Ch. 2). And it is also why these companies have long shunned any radical change in energy sources. The electric car, first invented in the 1830s, predates its gasoline and diesel counterparts by half a century, and for a while was more popular than both (Wakefield 1994). But by the early twentieth century, having proved less profitable than the gas guzzlers, it fell out of favour and was forcefully erased from the collective memory. Then came intolerable pollution, which in the 1990s led the state of California to mandate a gradual transition of automobiles to alternative energy. Complying with the new regulations, General Motors had its engineers quickly develop a highly efficient electric car, the EV1. But fearing that this gem of a car would undermine profit from their gas guzzlers, the company’s owners, along with owners of other concerned corporations in the automotive and oil business, also invested in an orchestrated attempt to defeat the California bill. When the regulation was finally overturned, every specimen of the EV1 was recalled and literally shredded (Paine 2006).171

A similar pattern emerges in the setting of broad electronic standards. In theory, the goal of such standards is to have as many different electronic components and processes resonate as seamlessly and effortlessly as possible. In practice, though, the debate is not over industrial resonance but business profit: it is not the technical blueprint that matters, but who will control it.

The production of digital audio tapes (DAT) in the early 1990s, for instance, had been postponed (to the point of making the technology outdated) because several large firms could not reach a consensus regarding its effect on recording profits, a saga that has since been replayed in the ‘format wars’ over digital versatile discs (DVD) and high-definition optical discs.

These examples can easily be extended. Other broad industrial diversions include the development by pharmaceutical companies of expensive remedies for invented ‘medical conditions’ instead of drugs to cure real disease for which the afflicted are too poor to pay; the development by high-tech companies of weapon technologies instead of alternative clean energies; the development by chemical and bio-technology corporations of one-size-fits-all genetically modified vegetation and animals instead of bio-diversified ones; the forced expansion by governments and realtors of socially fractured suburban sprawl instead of participatory and sustainable urbanization; the development by television networks of lowest-denominator programming that washes the brain instead of promoting its critical faculties; and so on.

Of course, as we repeatedly noted the line separating the socially desirable and productive from the undesirable and counterproductive is inter-subjective and contestable. But taken together, these examples nonetheless suggest that a significant proportion of business-driven ‘growth’ is wasteful if not destructive, and that the sabotage underlying these socially negative trajectories is exactly what makes them so profitable.

The pace of industry

The other limitation — perhaps less important but easier to approximate — concerns the growth of industrial capacity and output, whatever their purpose. The conventional view, both popular and academic, is that business loves growth. The more utilized the capacity and the faster its expansion, the greater the profit — or at least that’s what we are told. The facts, though, tell a very different story. In reality, business can tolerate neither full-capacity utilization nor maximum growth. And why the aversion? Because otherwise profit would collapse to zero.

Consider again the automobile sector. Were the large car companies to decide to produce as much as possible rather than as much as the ‘traffic can bear’, their output could probably double on fairly short notice. And this potential is hardly unique to automobiles. Almost every modern industrial undertaking — from petroleum, through electronics, to clothing, machine tools, telecommunication, pharmaceuticals, construction, food processing and film, to name a few — tends to operate far below its full technological capacity (not to be confused with full business capacity).172 If all industrial undertakings were to follow the reckless example of automobiles, the relentless pressure of oncoming goods and services would undermine tacit agreements and open cooperation among dominant firms and government agencies, trigger massive downward price spirals, and sooner or later end up in a Great Depression and a threat of political disintegration.

Speculating in a similar vein, Veblen (1923: 373) concluded that it was therefore hardly surprising that ‘such a free run of production has not been had nor aimed at; nor is it at all expedient, as a business proposition, that anything of the kind should be allowed’.173 Profits are inconceivable without production, but they are also impossible under a ‘free run’ of production. For profits to exist, business enterprise needs not only to control the direction of industrial activity, but also to restrict its pace below its full potential.

Business as usual

Conceptually, we would expect there to exist a non-linear relationship between the income share of capitalists on the one hand and their limitation of the pace of industry on the other.174 This relationship is illustrated hypothetically in Figure 12.1. The chart depicts the utilization of industrial capacity on the horizontal axis against the capitalist share of income on the vertical axis. Up to a point, the two move together. After that point, the relationship becomes negative.

Figure 12.1: Business and industry

The reason is easy to explain by looking at extremes. If industry came to a complete standstill, capitalist earnings would be nil (bottom left point in Figure 12.1). But capitalist earnings would also be zero if industry always and everywhere operated at full socio-technological capacity (bottom right point). Under this latter scenario, industrial considerations rather than business decisions would be paramount, production would no longer need the consent of owners, and these owners would then be unable to extract their tribute earnings.175

In a capitalist society, ‘business as usual’ means oscillating between these two hypothetical extremes, with absentee owners limiting industrial activity to a greater or lesser extent. When business sabotage becomes excessive, pushing output toward the zero mark, the result is recession and low capitalist earnings. When sabotage grows too loose, industry expands toward its societal potential, but that too is not good for business, since loss of control means ‘glut’ and falling capitalist earnings. For owners of capital the ideal condition, indicated by the top arc segment in Figure 12.1, lies somewhere in between: with high capitalist earnings being received in return for letting industry operate — though only at less than full potential. Achieving this ‘optimal’ point requires Goldilocks tactics — neither too warm nor too cold — or what Veblen sardonically called the ‘conscious withdrawal of efficiency’.

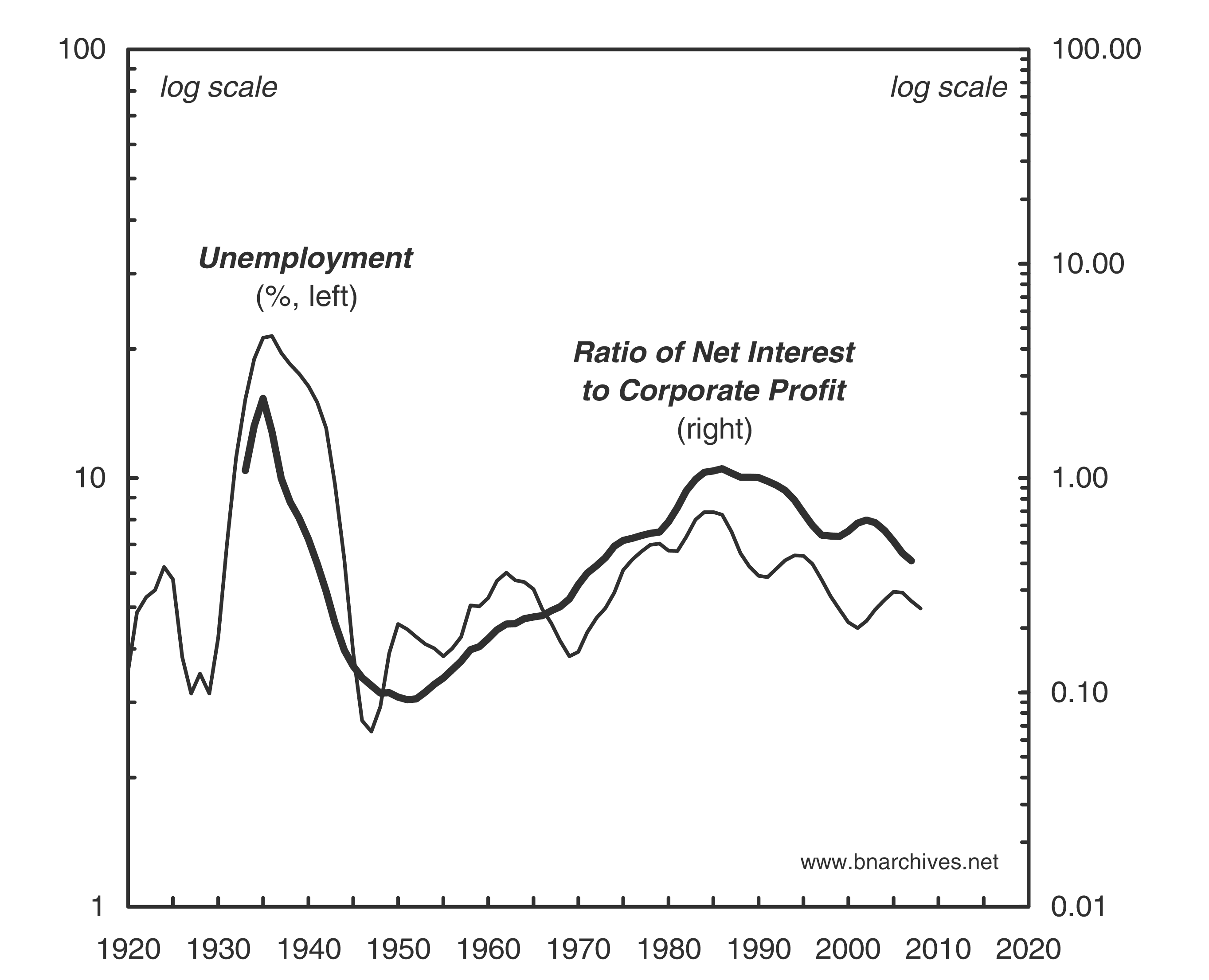

This theoretical relationship receives an astounding empirical confirmation from the recent history of the United States, depicted in Figure 12.2. The chart contrasts the success of business on the vertical scale with the limitation of industry on the horizontal. The former is measured by the income share of capitalists (profit and interest), the latter by the rate of unemployment (inverted from right to left).176 The data clearly show the negative effect on business — both of excessive industrial sabotage until the early 1940s and of insufficient sabotage during the Second World War. ‘Business as usual’ was restored only after the war, with growing industrial limitations helping capitalists move up and to the left on the chart, toward their ‘optimal’ income share.177

Figure 12.2: Business and industry in the United States

Note: Series are shown as 5-year moving averages.

Source: U.S. Department of Commerce through Global Insight (series codes: INTNETAMISC for interest; ZBECON for profit; YN for national income; RUC for the rate of unemployment).

Taking stock and looking ahead

Building on Veblen, our discussion so far has illustrated how business and industry could be thought of as fused yet distinct spheres of capitalism. According to this framework, industry is an integrated creative process whose productivity derives from the totality of its purposefully resonating pulses. By contrast, business is a power process carried out through the prerogatives of ownership. Owning per se is an idle act. It has no productivity and therefore no bearing on industry, either positive or negative. Owners of course can impact industry indirectly. But for this impact to be profitable it has to be negative. It is only by stirring the development of industry in directions that are wasteful and harmful yet easier to control, or by strategically limiting its pace so that their own discretion doesn’t become redundant, that profit can be earned. It is this threat of dissonance that enables absentee owners to lay claim to a process to which they do not directly contribute. That is how capitalist earnings are generated.

In what follows, we concentrate specifically on the way in which business limits the pace of industry. Extending Veblen, we identify two types of sabotage: (1) universal business-as-usual limitations that are carried out routinely and uniformly by all firms; and (2) limitations that are unique to a single company or group of companies. Corresponding to these two types of limitations are two rates of return: (1) a normal rate of return that all capitalists believe they deserve; and (2) a differential rate of return that capitalists seek over and above the normal.

Pricing for power

Begin with the universal methods of sabotage. To the uninitiated, these are practically invisible. They involve no violence and force, no fire and blood, no hunger and deprivation. They do not even seem to restrict industry. For the most part, their path is clean and detached. And the reason is simple: they operate not directly, but indirectly, through the fundamental unit of the capitalist order: price.

From price taking to price making

According to received liberal dogma, firms are ‘price takers’: they accept whatever price mother market gives them. The reality, though, seems to suggest the exact opposite. The standard practice, documented extensively and repeatedly since the 1930s, shows that most modern firms are ‘price makers’: they set their own price and then sell as much as possible at that price.

Neoclassicists have fought tooth and nail to deny this inverted reality. They had no other choice: to recognize price making would have pulled the rug from under conventional price theory and brought down the rest of economics. Substantively, their counterattack was a failure. Although led by some of the heaviest guns, it hardly dented the facts: price making was here to stay. Pedagogically, though, the attack was highly successful. It managed to expunge the whole debate from introductory economics textbooks, with the result that today’s students know little or nothing about the controversy. A brief outline therefore seems appropriate.178

The first to question seriously the competitive price-taking model and to emphasize the tendency toward oligopoly and monopoly was Veblen.179 During the roaring twenties his interventions were duly ignored; but by the 1930s, with the Great Depression having opened the door to intellectual dissent, his insights began to echo. Within a few years, the neoclassicists found themselves confronted with two sets of challenges. The first were the theories of ‘imperfect competition’ (by Robinson 1933) and ‘monopolistic competition’ (by Chamberlin 1933). Many neoclassicists considered these deviations scandalous, but in due course they managed to domesticate and absorb them into their creed. Their task, though, wasn’t nearly as easy with the second set of challenges. These were empirical, and they proved impossible to tame.

The debate opened with Gardiner Means’ path-breaking work on industrial prices in the United States (1935a; 1935b). Means showed that there were in fact not one but two types of prices. The first were the familiar ‘market prices’: relatively flexible, moving up and down with supply and demand and prevalent in competitive industries. But there was also a second and heretofore unfamiliar type of ‘administered prices’: relatively inflexible, changing only infrequently, responding slowly to market conditions and typical of concentrated industries.

This duality had two far-reaching implications. The first was that prices were intimately connected to crisis — and in more than one way. Means showed that during the Great Depression, competitive industries saw massive declines in their market prices, but only moderate drops in their output and employment. The situation in concentrated industries, though, was exactly the opposite: prices declined slightly, while production and payroll collapsed, sometimes by as much as 80 per cent. In other words, the Great Depression occurred mostly in concentrated industries whose prices proved relatively inflexible. Seen from a Veblenian perspective, administered prices were nothing but a mechanism of industrial sabotage.

The second implication was theoretical and general. Profit maximization requires that firms make the best out of the circumstances they face. Administered prices, though, respond only partly or not at all to market conditions. This discrepancy means that companies that set such prices do not make the best out of the circumstances, and, therefore, that they do not maximize their profit. The conclusion was simple and painful: the more prevalent administered prices become, the greater the irrelevance of standard price dogma. And since, according to study after study, most prices are administered, the agony must be considerable.180

The markup and the target rate of return

The first explicit confirmation of this painful conclusion came a few years later, with the publication of Hall and Hitch’s work on business behaviour (1939). Whereas Means focused on the pattern of prices, Hall and Hitch investigated those who set them. They interviewed company officials in Britain, asking them to explain how they determined prices. And their conclusions were stunning, at least by neoclassical standards. It turned out that firms did not follow the neoclassical recipe of equating marginal revenues and cost; that they did not know what these marginal magnitudes meant; and, most embarrassingly, that they did not care about profit maximization to begin with. The process that firms did follow was totally different: they started by calculating what they considered to be ‘normal’ unit cost (namely the cost at ‘normal’ levels of output); they tacked onto this cost a ‘conventional’ markup; and they kept the resulting price stable in the face of cyclical variations in demand.

Later on, these findings were augmented by the notion of a ‘target rate of return’. According to the empirical research of Kaplan, Dirlam and Lanzillotti (1958), modern firms, particularly the leading ones, begin with a long-term target rate of profit, and then back-calculate the markup necessary to realize this rate of return over the longer haul.181

This method seems straightforward — and it probably is for the price-setting firm. But not so for the theorist. Whereas the former merely has to act, the latter has to reason. And as it turns out, the pricing formula cannot be ‘explained’ easily. The main problem is the ‘target rate of return’ and the associated ‘conventional’ markup: since these no longer obey the rules of profit maximization, there is no way to find their unique values. In theoretical parlance, they become ‘indeterminate’. Hall and Hitch (1939: 28) tried to solve the problem by making the markup a reflection of the ‘community of outlook’ of businessmen, while others, such as Eichner (1976), anchored the target rate of return in the firms’ ‘investment plans’. However, conventional economic theory does not know how to theorize airy concepts such as the ‘community of outlook’ and ‘investment plans’, as a result of which ‘economic science has not yet solved its first problem — what determines the price of a commodity?’ (Robinson 1966: 79).

A possible way out of this puzzle was pointed out by Michal Kalecki (1943a), whom we have mentioned in Chapter 4. For Kalecki, the markup was not simply a vague social convention, but a measure of power: he called it the ‘degree of monopoly’.182 Monopoly power, like every other form of power, can be known only by its consequences. And for Kalecki, that consequence was the markup: the higher the markup and its associated rate of return, the greater the implied power of those who set it, and vice versa.

Pricing and incapacitating

And so the circle closes and sabotage becomes invisible. The vast majority of modern capitalists (or their managers) are ‘price makers’: they fix the price of their product and then let ‘market forces’ do the rest for them. To the naked eye they all seem keen on producing and selling as much as possible, but beyond the façade the picture is very different. The specific level at which they set the price already embodies the power to incapacitate. On the one hand, the profit target and markup built into the price reflect the firm’s power, while, on the other hand, that power, exercised by the high price, serves to restrict industry below its full capacity. The sabotage and the power to inflict it remain concealed, but their consequences are very real.

Is free competition free of power?

Now, up to this point, our discussion has been limited to the mainstream of administered prices. It should be added, however, that even in those isolated cases where ‘free competition’ is said to reign, the power to incapacitate is not at all absent. To see why this is so, consider a neoclassical ‘perfectly competitive’ firm — but instead of focusing on what it does, think of what it is unwilling to do. For illustration, take the case of mining, where prices are presumably set by global supply and demand. A reader schooled in neoclassical theory may be tempted to conclude that, at least in such cases, the presence of market prices excludes sabotage. But it ain’t necessarily so.

Mining output, much like any other output, is controlled by business. The actual production of a single firm and the number of firms in operation therefore are bounded not by the state of industrial arts, but by what can be sold at a ‘reasonable’ profit. In fact, this is exactly what standard neoclassical manuals tell the owner of a perfectly competitive firm: in the long-run, have your company produce only if you expect to earn at least the normal rate of return. Otherwise, shut down.

For neoclassicists who insist on equating the normal rate of return with the marginal revenue product of capital, this stipulation simply assures efficient resource allocation. From a Veblenian standpoint, though, this unwillingness to produce for less than some conventional rate of return is the very manifestation of industrial sabotage. Thus, although ‘perfectly competitive’ firms may not set prices, their productive activity — individually and in the aggregate — nevertheless is limited by the imperative of earning a normal rate of return.

The capitalist norm

The normal rate of return and the natural rate of unemployment

The normal rate of return of course is a fuzzy magnitude, a convention that varies among business owners and over time. The important point, however, is that this normal rate exists in the first place. With the gradual penetration of capitalist institutions, owners have come to believe that the flow of profit is a natural, orderly phenomenon. As such, profit is seen as having a more or less predetermined mean growth rate and a dispersion that varies with circumstances (expressed by the standard deviation from this mean).

According to Veblen, this development is hardly trivial. Until a few hundred years ago, profit was seen more as a coincidence than a regular feature of ownership. The main goal was to retain property, and owners of land, slaves or gold rarely expected their assets to grow ‘on their own’. But under capitalism, where the business limitation of industry grows increasingly universal, the consequent profit is regarded as natural and its rate of expansion as normal. In this way, the strategic limitation of industry can prevail even in the absence of explicit binding arrangements.

The normality of profit has been so thoroughly accepted that the industrial limitation from which it derives is no longer self-evident. Consider the fact that since 1890, the first year for which aggregate data are available, the official US rate of unemployment averaged 7 per cent (5.7 per cent without the 1930s). Economists, however, remain unimpressed by this fact. Indeed, that is exactly what they expect. Given that this average rate has been associated with ‘business as usual’, most now take it to represent ‘the natural rate of unemployment’. In an unconscious Orwellian bent, modern textbooks casually talk about the ‘full employment unemployment rate’, ‘unemployment equilibrium’ and ‘over-full employment’ — generally without quotation marks (see for example Parkin and Bade 1986: 282–83; and Branson 1989: 188). Even Carlyle could not have foreseen the dismal state of a society subjugated to the economic science.

Antecedents: return and sabotage in antiquity

The power features of the capitalist normal rate of return are not without precedent. Their origins can be traced to the early emergence of the rate of interest in the Middle East some 4,500 years ago. The ancient interest rate, just like today’s normal rate of return, was a matter of power and sabotage. But its institutional and societal underpinnings were radically different and are worth exploring so as to put our discussion in context.183

The roots of the pecuniary standard are inherently negative. In almost every language, the concept of debt is associated with guilt and sin. Originally, proto-money was used for the settling of obligations, including reparations (‘pay’ and ‘pacify’ share the same root in both English and Hebrew), marriage debts, communal fines, religious offerings and, eventually, royal taxes. The máš – the Sumerian term for interest — means ‘kid’ and ‘calf’, a term that developed from the earlier religious proto-tax of the máš-fee. Mikneh in Hebrew means ‘herd’ narrowly and ‘moveable property’ more broadly. Similarly, the words ‘pecuniary’, ‘fee’ and ‘feudal’ all derive from the Latin pecus — a concept that later came to denote ‘cattle’, but that originally referred more broadly to ‘personal chattels’ and ‘moveable wealth’.

Livestock etymologies and growth metaphors have led neoclassicists to conclude that ancient interest payments on debt were natural returns on productive agricultural yield. This is an erroneous interpretation for two reasons. First, although debt (along with many other concepts) was often counted in ‘pastoral’ units, it was considered barren throughout antiquity. Second and more straightforwardly, most lending in antiquity had nothing to do with ‘investment’ and therefore had no ‘return’ from which to deduct interest.

The institution of interest was first invented in Sumer during the third millennium BCE, from where it later spread to the Eastern Mediterranean, Greece and Rome. From their very inception, debt, credit and interest were matters of organized power. The Sumerian proto-monetary architecture was fundamentally statist.184 It developed as a royal method of administration and accounting, a system with which the palace and temple allocated material provisions, organized production and collected taxes. Commercial and longterm trade accounting, wherever they existed, were part and parcel of this statist architecture.

The Sumerian debt system was very different from the capitalist one. Capitalist borrowers are usually thought of positively, as entrepreneurs who leverage their own money in order to make more money. By contrast, most Sumerian borrowers were farmers in distress, on-the-brink subjects whose dire circumstances forced them to ‘mortgage’ (or death-pledge) their cattle and even family members just to make ends meet. These peasants did not ‘invest’ their loans; they used them simply to stay alive. And since the borrowers made no productive advances, there was no reason for the interest they paid to bear any relationship to the ‘efficiency’ of their chattel or the ‘yield’ of their fields.185

And, indeed, contrary to the ever-fluctuating capitalist normal rate of return, the standard Sumerian rate of interest never changed. It was fixed at 1/60 per month, or 20 per cent annually, and did not budge for more than a millennium. The Greek interest rate of 1/10 per annum and the Roman rate of 1/12 — although not nearly as durable as the Sumerian — were also set for long periods of time. The stability of these ancient rates reflected the pattern of agricultural seasons, a system of mathematical fractions and a set of religious myths — a combination that the ruling elites gradually synthesized and locked into an inflexible architecture of pecuniary rules.

This pre-capitalist architecture, just like the capitalist one, was rooted in organized power and inflicted plenty of damage. Exorbitant interest rates dispossessed and enslaved numerous borrowers. In fact, the sabotage was so severe that ancient rulers had to announce periodic debt moratoriums, or Clean Slates, to avoid social disintegration. But this is where the similarity ends.

Pecuniary power: ancient versus capitalist

In antiquity organized power was enforced directly by royal decree and increased by the open use of force. Wealth was a subset of power, an entity whose magnitude depended on the whim of gods and the dose of violence. It had no predetermined pace of growth, positive or negative, natural or religious. And whatever its erratic rate of expansion, it obviously could not have depended on a fixed rate of the interest. The latter was seen primarily as an administrative device. The ancients even forbade its compounding.

The capitalist order puts this logic on its head. On the surface, organized power seems to have vanished. With autonomous, growth-seeking agents engaged in voluntary transactions, the normal rate of return no longer connotes destitution and enslavement. But this is no more than an optical illusion. Paraphrasing Anatole France, the main novelty is that now ‘everyone is free to sleep under the bridge’. Organized power is still very much there, albeit in a totally different form. Instead of open violence administered by state rulers, we have administered prices openly imposed by private absentee owners. On the consensual surface of the market, no one seems to hold that power. But the unshaken belief in the normal rate of return and its associated natural rate of unemployment attests to the omnipresence of power.

Unlike its ancient predecessor, the normal rate of return is no longer a mere administrative device. Whereas in antiquity the rate of interest was a subsidiary of state power, under the system of business enterprise the capitalist state itself is gradually subsumed by the logic of the normal rate of return. Government deliberations and decisions are constantly under the long shadow of the bond market, and even central bankers, who ostensibly ‘determine’ the short-term ‘risk-free’ rate of interest, in fact take their cue from the ‘market’.186 The normal rate becomes a central feature of the capitalist nomos. It is the yardstick on which capitalization is based and the principal evidence that not only the level of organized power, but also its augmentation, is natural, inherent and just.

The differential underpinnings of universal sabotage

Where does the capitalist normal rate of return come from? Paradoxically, the universality of profit and the regularity of its expansion are based on the specific institutions of differential sabotage. Indeed, a normal rate of return can exist only because owners are never satisfied with it. What owners believe they are entitled to under normal circumstances is not what they seek in practice. The primal drive of modern business enterprise is not to meet but to beat the average. Business performance is denominated in relative, not absolute terms, and it is ‘getting ahead of the competition’ that constitutes the final aim of all business undertakings. This compelling desire to outperform — to earn more, to grow larger, to expand faster than others — is perhaps the most fundamental urge of contemporary business. In that sense, even members of the tightest oligopolistic coalition are fiercely competitive.

Paul Johnson (1983: Ch. 1) associates this relativism with the twentieth-century vulgarization of Einstein’s theory. In his view, the misplaced social ization of physics ushered in a total meltdown of the absolute values, both religious and ethical, that characterized the nineteenth century. But such cultural emphasis, however appealing, misses the structural imperative of accumulation. Understood as a power institution, capital is inherently differential, a crucial aspect to which we turn below. For the moment, though, our focus is on how the differential limitation of industry forms the basis for the normal rate of return.

Differential returns mean above-average profit growth. Such returns usually require raising one’s own profit growth — though that in itself is rarely feasible without also limiting the average growth of profit. The problem is simple. Profit is a product of sales and the profit share in sales. Individual firms can try to raise their sales volume faster than the average; but that alone will not guarantee differential profit growth, since sales and the profit share are not independent. If all firms push their sales up, the consequence is an overall loss of business control over industry and a resulting drop in the overall profit share of income. The conclusion — well known since antiquity but broadly institutionalized only since the late nineteenth century — is the imperative of restricted access: for the profits of one owner (or a coalition of owners) to beat the average, others must be prevented from accessing the same earnings. Whereas the conventional logic of profit maximization focuses only on the capitalist’s own lot, the quest for differential profit also involves the lot of other capitalists.

The means of achieving this differential end are numerous, transcending both business and politics and spanning the societal spectrum from the individual to the global. These means include direct limitations, such as predatory pricing, formal and informal collusion, advertising and exclusive contracts. They also include broader strategies like targeted education, patent and copyright laws, industrial policies, financial regulations, preferential tax treatment, legal monopolies, labour legislation, trade and investment pacts and barriers and, of course, the use of force, including military, for differential business ends.

The negative industrial impact here is often indirect. For the benefiting owner, the differential gain accrues because the necessary industrial limitation is borne by other owners. For instance, historically the large petroleum companies have gained from expanding world demand at least partly because they have been politically able to keep smaller ‘independent’ companies largely out of the loop (Blair 1976). On the other hand, when exclusion cannot be ensured, like in the case of software development or the manufacturing of microchips, soaring production often overshoots into excess capacity and falling profits. In general, then, the negative impact of business on industry is both indirect and non-linear: while profits usually correlate positively with one’s owned industrial activity, beyond a certain point this correlation is maintained only insofar as the production controlled by others is contained.

In sum

Business profits are possible because absentee owners can strategically limit industry to their own ends. Such control is carried out routinely, either by pricing products toward earning a target rate of return at some standard capacity utilization, or by making industrial activity conditional on earning a normal rate of return. Underlying these universal business principles are numerous differential practices, with owners, individually or in groups, trying to redistribute income via institutional and organizational change. The specific aim of most (though not all) differential tactics is to restrict the industrial activity controlled by existing or potential rivals. Their aggregate consequence is dissonance that undermines the industrial community at large, yielding a natural rate of unemployment on the one hand and a corresponding normal rate of return on the other.

The link between differential and universal industrial sabotage is closely related to the twin conflicts pervading the regime of business enterprise — one between absentee owners and the industrial community, the other between absentee owners themselves. These two conflicts resemble Marx’s distinction between the class struggle and intra-capitalist competition — but with a big difference. Whereas for Marx the class struggle was conceptually prior to the intra-class relationship among capitalists, in our view they are two sides of the same process: the dominance of capital over society depends on a pecking order among capitalists themselves, and vice versa. On a disaggregate level, the distribution of profit among absentee owners is roughly related to the balance of business damage they can inflict on each other. And on the aggregate level, the overall industrial sabotage arising from their internal business warfare determines their overall profit share (although not in any linear way and along with other factors). In other words, the goals of business owners revolve around the distribution of profit, while the methods of business sabotage ensure that such profit is made available in the first place.

Capital and the corporation

Capital as negation

One reason why Veblen’s analysis never became too popular is that it made business capital a negative industrial magnitude. This view of the business-industry nexus is alien to both neoclassical and Marxian thinking. For neoclassicists, who emphasize harmony and equilibrium, the positive social value of capital is hardly in doubt. Contrary to this view, Marx accentuated the antagonistic social basis of capital, linking accumulation to exploitation. However, just like his liberal counterparts, he too stressed the relentless pressure to improve productivity — pressure that stems not from the lure of monopoly and imperative of power, but from the discipline of competition. And so despite the antagonism — or perhaps because of it — capitalists according to Marx must use their capital in the most productive way possible.

Even British contributors to the Cambridge Controversy were still ambiguous on the industrial footing of capital. As Joan Robinson (1971) pointed out, Sraffa broke the ‘conspiracy of silence’ by destroying the presumption that the profit rate measured the contribution of investment to national income, let alone to human welfare; by calling into question the positive connotation of both accumulation and growth; and by refocusing attention on distribution. But although Robinson later realized that Veblen had anticipated much of this critique, she never took the next step to explore the possibility that distributive power and industrial production were not simply uncorrelated, but negatively correlated (1967: 60; 1975: 115–16).

The difference is subtle but crucial: while the Cambridge Controversy raised the possibility that capital could be unproductive, Veblen contended that, from an industrial point of view, it was necessarily counterproductive.

This claim is not easy to dismiss. Business, like other power institutions throughout history, can force people to act, but it cannot make them productive. Moreover, productivity as such, being socially hologramic and therefore open and unrestricted, cannot generate a profit. The only way for capitalists to profit from productivity is by subjugating and limiting it. And since business earnings hinge on strategic sabotage, their capitalization represents nothing but incapacitation. In this particular sense, capital, by its very construction, is a negative industrial magnitude.

The rise of the modern corporation

The emergence of capital as a business limitation of industry was greatly facilitated by the rise of the modern corporation and the larger use of credit as ownership. Now, on the face of it, this claim sounds counterintuitive. In fact, most readers would probably expect the exact opposite to be true — namely, that the corporation emerged precisely because of its productivity. But as with many other productivist categories, there is more here than meets the eye.

Perhaps the first to contemplate the broad social significance of incorporation was Karl Marx. Prescient as usual, he suggested that the corporation may mark the dawn of a new capitalist regime: ‘The capitalist stock companies as well as the co-operative factories’, he wrote, ‘may be considered as forms of transition from the capitalist mode of production to the associated one’ (Marx 1909, Vol. 3: 521). Yet, in his opinion, this transition was driven by the imperative of efficiency. The corporation helped concentrate the means of production and in so doing enabled capitalists to further increase productivity and hasten accumulation.

The liberal view is different, but not by much. According to mainstream economics, the corporation is the most effective way for society — not just its capitalists — to reap the benefits of large-scale production. The following pronouncement by Samuelson Inc. is typical: