| 15 | Breadth |

It is difficult to describe the rapacity with which the American rushes forward to secure the immense booty which fortune proffers to him. . . . for he is goaded onwards by a passion more intense than the love of life. Before him lies a boundless continent, and he urges onwards as if time pressed and he was afraid of finding no room for his exertions.

—Alexis de Tocqueville, Democracy in America

It is hard to think of a capitalist growth episode more exhilarating and promising than the nineteenth-century advancement of the ‘American frontier’. The promise of abundance, riches and endless opportunities (minus the Indians) excited tellers of stories and theories alike and lured millions to try their luck in the land of unlimited possibilities (Zinn 1999).

Yet, as the opening quote from de Tocqueville points out, even in this historically unique period, with a wilderness large and fertile enough to accommodate everyone, the pursuit of growth was decidedly differential. Growth itself may seem unbounded, but the control of growth is always bounded. No capitalist can ever control more than the entire social process. This is the whole. The only way for some owners to gain more power over this totality is for others to give up some of theirs. In the rush for power, there is never enough room for everyone.

The present chapter examines how dominant capital increases its power by augmenting the relative size of its corporate organs. To reiterate, there are two basic ways of doing so: (1) green-field investment that buys newly built facilities and hires new employees,238 and (2) mergers and acquisitions that take over the existing facilities and employees of other firms. We spend relatively little time on green-field growth, which, as we shall see, is the less important avenue. The bulk of the chapter is devoted to corporate amalgamation and its far-reaching implications for the capitalist creorder.

Green-field

Dominant capital can run its green-field investment at different speeds: it can sprint ahead of the pack, expanding its employment faster than the overall growth of the business sector; it can run with the pack, expanding at the same rate as the business sector; or it can trail the business sector. Of these strategies, the first two are relevant for our inquiry. Both augment the external breadth of dominant capital (differential employment per firm); but as it turns out, both act as a double-edged sword in that they also undermine external depth (differential profit per firm).

Running ahead of the pack

The consequences of running ahead of the pack are fairly clear. When larger firms hire new workers faster than the overall expansion of private employment, their corporate size grows relative to that of the average firm (particularly since, as we shall see shortly, the size of the average firm tends to fall even as overall employment rises).

But, save for exceptional circumstances, this strategy is suicidal. Recall that the ultimate purpose is to increase not the relative size of the organization (breadth), but of relative profit (the product of breadth and depth). And it turns out that that this strategy usually loses in depth more than it gains in breadth, leading to falling differential profit.

As the reader now knows, ‘letting industry loose’ undermines the fundamental tenet of ‘sabotage’ without which profit and accumulation are impossible. The vulnerability here is so great that even the mere anticipation of ‘excessive’ growth is often enough to trigger panic, price war and sharply lower differential profit per firm. Perhaps this is the reason that most dominant-capital executives respond to green-field ‘opportunities’ with the suspicion of a New-York-City driver who has just spotted an empty parking space. Their typical knee-jerk reaction is to look for the proverbial road-sign warning: ‘Don’t even THINK of parking (your cash) here’.

Running with the pack

Fortunately for dominant capital, there is no need to lead. Simply going with the crowd and letting employment expand in tandem with the business sector as a whole is sufficient to generate external breadth. The success of this ‘sound’ strategy has to do with the different expansion patterns of large and small firms.

Large companies react to overall growth mainly by increasing their employment ranks. Smaller companies, by contrast, respond by growing in number (through the birth of new firms) as well as in size (by hiring more workers). This difference is important since newborn firms, by their very nature, tend to be smaller than the average (recall our discussion of aggregate concentration in Chapter 14). The implication is that, even if green-field growth is spread proportionately between dominant capital and the rest of the business universe (since both expand at the same clip), as long as some of this growth results in the birth of smaller firms, the net impact is to reduce average employment per firm and, therefore, to augment the differential breadth of dominant capital.

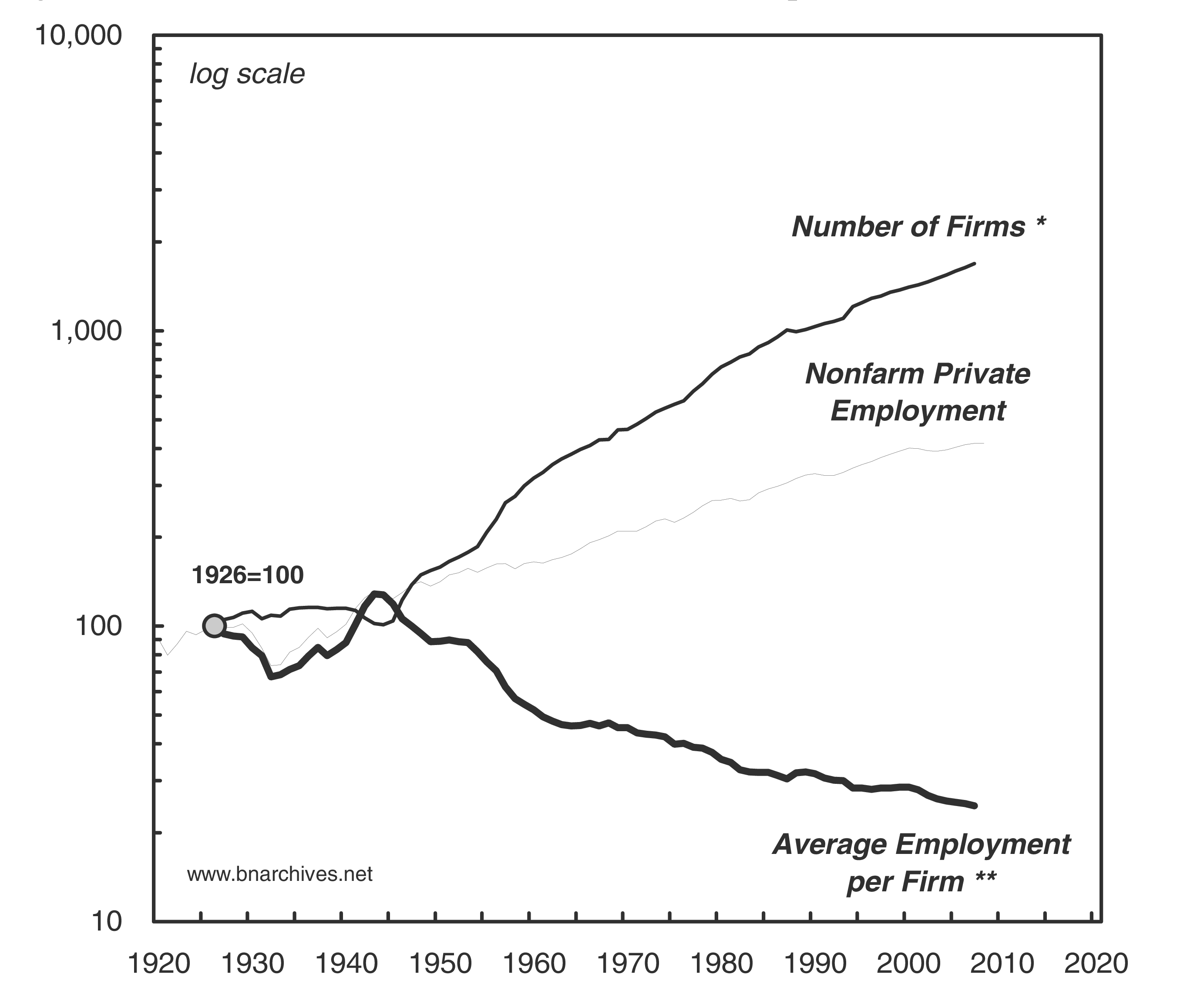

The evolution of this process in the United States is illustrated in Figure 15.1, which shows the number of corporations, the overall level of employment and the average number of employees per firm (with series rebased for comparison).239 The overall picture is one of pronounced divergence. From 1926 to 2008, the number of corporations has risen nearly sixteenfold, whereas overall employment has grown only threefold. As a result of this difference, average employment per firm has dropped by over 75 per cent (note the logarithmic scale).240

Figure 15.1: US employment, number of firms and size of firms

* Corporations only.

** Nonfarm private employment divided by the number of firms.

Source: U.S. Internal Revenue Service (number of corporate tax returns; the numbers for 2004–2006 are extrapolated based on recent growth rates); Historical Statistics of the United States (series codes: D127 for non-agricultural employment; D139 for non-agricultural government employment till 1938); U.S. Bureau of Economic Analysis through Global Insight (series codes: EEA for nonfarm private employment from 1939 onward).

The process wasn’t always even. During the two decades between the mid1920s and mid-1940s, the number of firms remained relatively stable, first because of the Great Depression, and subsequently due to the Second World War. Consequently, changes in overall employment during that period were reflected more or less fully in the average size of firms, which fell throughout the Depression only to rise rapidly thereafter.

In the longer run, however, this early pattern proved an aberration. As noted, capitalism is subject to strong centrifugal forces, one of which is the inability of business enterprise to control the overall number of independent capitalists on the scene. And indeed, after the war, the number of firms started multiplying again, while their average size trended down more or less continuously. Since large-firm employment has increased over the same period, we can safely conclude that overall employment growth served to boost the differential breadth of dominant capital.

The indirect impact of employment growth, operating through depth, is more complex and harder to assess. On the one hand, the multiplicity of small firms keeps their profit per employee low — partly by precluding cooperation and pricing discretion and partly by undermining formal political action. This fact bears positively on the differential depth of dominant capital. At the same time, unruly growth in the number of small firms can quickly degenerate into excess capacity, threatening to unravel cooperation within dominant capital itself. The balance between these conflicting forces is difficult if not impossible to determine.

All in all, then, green-field growth is no panacea for dominant capital. Although the process boosts its differential breadth, it has an indeterminate and possibly negative effect on differential depth. One way to counteract this latter threat is to scare the underlying population with ‘overheating’ and educate ‘policy makers’ about the benefits of ‘balanced growth’ — a stagnationary recipe that has been applied with considerable success over the past half-century.241 But the more fundamental solution to the problem is corporate amalgamation.

Mergers and acquisitions

A mystery of finance

Our discussion of amalgamation begins with Figure 15.2. The chart plots a ‘buy-to-build’ indicator, expressing the dollar value of mergers and acquisitions as a per cent of the dollar value of gross fixed investment. In terms of our own categories, this index corresponds roughly to the ratio between internal and external breadth. (The data sources and method of computing this index are described in the Data Appendix to the chapter.)

The chart illustrates two important processes — one secular, the other cyclical. Secularly, it shows that, over the longer haul, mergers and acquisitions indeed have become more important relative to green-field investment (Proposition 3 in Chapter 14). At the end of the nineteenth century, money put into amalgamation was equivalent to less than 1 per cent of green-field investment; a century later, the ratio surpassed 200 per cent. The trend growth rate indicated in the chart suggests that, year in, year out, mergers and acquisitions grew 3.4 percentage points faster than new capacity.

Figure 15.2: US accumulation: internal vs external breadth

Source: See Data Appendix to the chapter.

Now, whereas employment associated with new capacity is added by small and large firms alike, amalgamation increases mostly the employment ranks of dominant capital. The net effect of this trend, therefore, is a massive contribution to the differential accumulation of large firms.242

The reasons for this tendency are not at all obvious. Why do firms decide to merge with, or take over other firms? Why has their urge to merge grown stronger over time? And what does this process mean for the broader political economy?

These are not straw-man questions. Mergers baffle the experts. ‘Most mergers disappoint’, writes The Economist, ‘so why do firms keep merging?’ (Anonymous 1998). And the textbooks offer no clear answer. According to one influential manual, mergers remain one of the ‘ten mysteries of finance’, a riddle for which there are many partial explanations but no overall theory (Brealey et al. 1992: Ch. 36).

The efficiency spin

Needless to say, amalgamation is a real headache for mainstream economics, whose models commonly rely on the assumption of atomistic competition. Alfred Marshall (1920) tried to solve the problem by arguing that firms, however large, are like trees in the forest: eventually they lose their vitality and die out in competition with younger, more vigorous successors.

On its own, though, the forest analogy was not entirely persuasive, if only because incorporation made firms potentially perpetual. So, for the sceptics, Marshall had to offer an add-on. Even if large firms failed to die, he said, and instead grew into a corporate caste, the attendant social inconvenience was still tolerable — because, first, such a caste tended to be benevolent and, second, the political costs were outweighed by the greater economic efficiency of large-scale business enterprise.

The rigorous spin on this justification was provided by Ronald Coase (1937), who stated that the size of firms is largely a matter of ‘transaction costs’. Inter-firm transactions, he asserted, are the most efficient since they are subject to market discipline. Unfortunately, such transactions are not free, and therefore they make sense only if their efficiency gains exceed the extra cost of carrying them through; otherwise, they should be internalized as intra-firm activity. Using such a calculus, one can then determine the proper ‘boundary’ of the firm, which, according to Coase, is set at the precise point where ‘the costs of organizing an extra transaction within the firm become equal to the costs of carrying out the same transaction by means of an exchange on the open market or the costs of organizing in another firm’ (p. 96).

The ideological leverage of this theory proved immense. It implied that if companies such as General Electric, Cisco or Exxon decided to ‘internalize’ their dealings with other firms by swallowing them up, then that must be socially efficient; and it meant that their resulting size — no matter how big — was necessarily ‘optimal’ (for instance, Williamson 1985; 1986). In this way, the nonexistence of perfect competition was no longer an embarrassment for neoclassical theory. To the contrary, it was the market itself that determined the right ‘balance’ between the benefits of competition and corporate size — and what is more, the whole thing was achieved automatically, according to the eternal principles of marginalism.

But then, there is a little glitch in this Nobel-winning spin: it is irrefutable. The problem is, first, that the cost of transactions (relative to not transacting) and the efficiency gains of transactions (relative to internalization) cannot be measured objectively; and, second, that it isn’t even clear how to identify the relevant transactions in the first place. This measurement limbo makes marginal transaction costs — much like marginal productivity and marginal utility — unobservable; and with unobservable magnitudes, reality can never be at odds with the theory.243

For instance, one can use transaction costs to claim that the historical emergence of ‘internalized’ command economies such as Nazi Germany or the Soviet Union proves that they were more efficient than their market predecessors. The obvious counterargument, which may well be true, is that that these systems were imposed ‘from above’, driven by a quest for power rather than efficiency. But then, can we not say the exact same thing about the development of oligopolistic capitalism?244

In fact, if it were only for efficiency, corporations should have become smaller, not larger. According to Coase’s theory, technical progress, particularly in information and communication, reduces transaction costs, making the market look increasingly appealing and large corporations ever more cumbersome. And, indeed, using this very logic, Francis Fukuyama (1999) has announced the ‘death of the hierarchy’, while advocates of the ‘E-Lance Economy’ (as in freelance) have argued that today’s corporate behemoths are anomalous and will soon be replaced by small, ‘virtual’ firms (Malone and Laubacher 1998). So far, though, these predictions seem hopelessly wrong: amalgamation has not only continued, but accelerated, including in the so-called high-technology sector, where transaction costs have supposedly fallen the most.

From efficiency to power

From an efficiency perspective, the relentless growth of large firms is indeed puzzling. Why do firms give up the benefit of market transactions in pursuit of further, presumably more expensive internalization? Are they not interested in lower costs?

From a power viewpoint, though, the riddle is more apparent than real. Improved technology certainly can reduce the minimum efficient scale of production (MES); and, indeed, today’s largest establishments (plants, head offices, etc.) often are smaller than they were a hundred years ago. However, firms are not production entities but business units; and given that they can own many establishments, their boundary need not depend on production as such. The real issue with corporate size is not efficiency but differential profit, and the key question therefore is whether amalgamation helps firms beat the average — and if so, how?

The conventional wisdom here is that mergers and acquisitions are a disciplinary form of ‘corporate control’. According to writers such as Manne (1965), Jensen and Ruback (1983) and Jensen (1987), managers are often subject to conflicting loyalties, and this conflict may compromise their commitment to profit maximization (the so-called principal-agent problem). The threat of takeover puts these managers back in line, forcing them not only to improve efficiency, but also to translate such efficiency into higher profit and rising shareholders’ value.

This argument became popular during the 1980s. The earning yield on US equities fell below the yield on long-term bonds for the first time since the 1940s, and that drop gave corporate ‘raiders’ the academic justification (if they needed one) for launching the latest and longest merger wave. The logic of the argument, however, was and remains problematic. Mergers may indeed be driven by profit, but that in itself has little to do with productivity gains. Neither is there much evidence that mergers are prompted by inefficiency, or that they make the combined firms more efficient.245 Indeed, as we suggested in Chapter 12 and argue further below, the latent function of mergers in this regard is not to boost efficiency but to tame it — a task that they achieve by keeping a lid on overall capacity growth. Moreover, there is no clear indication that mergers make the amalgamated firms more profitable than they were separately — although here the issue is somewhat more complicated and requires some explication.

Two points are worth noting. First, there is a serious methodological difficulty. Most attempts to test the effects of mergers on profitability are based on comparing the performance of merged and non-merged companies.246 While this method may offer some insight in the case of individual firms, it is misleading when applied to dominant capital as a whole. Looking at the amalgamation process in its entirety, the issue is not how it compares with ‘doing nothing’ (that is, with not amalgamating), but rather how it contrasts with the alternative strategy of green-field investment. Unfortunately, such a comparison is impossible since the very purpose of mergers and acquisitions is to avoid creating new capacity. In other words, amalgamation removes the main evidence against which one can assess its business success.

Perhaps a better, albeit ‘unscientific’, way to tackle the issue is to answer the following hypothetical question: What would have happened to the profitability of dominant capital in the United States if, instead of splitting its investment one third for green-field and two thirds for mergers and acquisitions, it were to plough it all back into new capacity? As Veblen (1923) correctly predicted, such a ‘free run of production’ is not going to happen, so we cannot know for sure. But then the very fact it hasn’t happened, together with the century-long tendency to move in the opposite direction, from greenfield to amalgamation, already suggests what the answer may be.247

The second important point concerns the meaning of ‘profitability’ in this context. Conventional measures, such as earnings-to-price ratio, return on equity, or profit margin on sales, relevant as they may be for investors, are too narrow as indicators of capitalist power — particularly when such power is vested in and exercised by corporations rather than individuals. A more appropriate measure for this power is the distribution and differential growth of profit (and of capitalization more broadly), and from this perspective mergers and acquisitions make a very big difference. By fusing previously distinct earning streams, amalgamation contributes to the organized power of dominant capital, regardless of whether or not it augments the more conventional rates of return. In our view, this ‘earning fusion’, common to all mergers, is also their ultimate reason.

And indeed, by gradually shifting the emphasis from building to buying, from colliding to colluding and from a certain measure of public oversight to increasingly capitalized government, corporate capitalism in the United States and elsewhere has been able not only to lessen the destabilizing impact of green-field cycles pointed out by Marx, but also to reproduce and consolidate on an ever-growing scale. Instead of collapsing under its own weight, capitalism seems to have grown stronger. The broader consequence of this shift has been creeping stagnation (Proposition 3 in Chapter 14); and yet, as Veblen already suggested a century ago, the large accumulators have learned to ‘manage’ this stagnation for their own ends.

Patterns of amalgamation

Merger waves

Now, this general rationale for merger does not in itself explain the concrete historical trajectory of corporate amalgamation. Mergers and acquisitions grow, but not smoothly, and indeed the second feature evident in Figure 15.2 is the cyclical pattern of the series (Proposition 4 in Chapter 14).

Looking at the past century, we can identify four amalgamation ‘waves’. The first wave, occurring during the transition from the nineteenth to the twentieth century, is commonly referred to as the ‘monopoly’ wave. The second, lasting through much of the 1920s, is known as the ‘oligopoly’ wave. The third, building up during the late 1950s and 1960s, is nicknamed the ‘conglomerate’ wave. And the fourth wave, beginning in the early 1980s, does not yet have a popular title, but based on its all-encompassing nature we can safely label it the ‘global’ wave.

This wave-like pattern remains something of a mystery. Why do mergers and acquisitions have a pattern at all? Why are they not erratic? Or, alternatively, why do they not grow continuously or in line with green-field investment? So far, most attempts to answer these questions have approached the issue from the micro perspective of the firm, which is precisely why they run into a dead end.

Tobin’s Q

One of the more famous explanations is based on the work of Tobin and Brainard (1968; 1977), whom we have already met in Chapter 10. The underpinnings of the argument cannot be simpler: capitalists are rational, and rational actors buy what is cheap. Their yardstick is Tobin’s Q: the ratio between the capitalized value of an asset on the market and the price of building it from scratch. When Tobin’s Q is smaller than 1, existing capacity is cheaper, so the firm will buy it from others. And when Tobin’s Q is greater than 1, new capacity is cheaper, so the firm will construct it anew.

For the corporate universe as a whole, Tobin’s Q is the ratio of overall market capitalization to the replacement cost of all outstanding assets; and if individual rationality extends to aggregate rationality, we should observe the buy-to-build indicator moving inversely with Tobin’s Q: the less expensive existing assets are relative to newly produced ones, the greater the proportion of ‘financial’ to ‘real’ investment should be, and vice versa.

The explanation seems sensible enough, only that reality refuses to abide. Figure 15.3 shows the relationship between the two magnitudes: our own buy-to-build indicator, expressing mergers and acquisitions as a per cent of gross fixed investment; and Tobin’s Q, computed by dividing the overall market value of stocks and bonds by the total current cost of corporate fixed assets (both series are smoothed for easier comparison).

Figure 15.3: Tobin’s Q

Note: The market value of stocks and bonds is net of foreign holdings by US residents. Series are smoothed as 5-year moving averages.

Source: For data sources and computations of the Buy-to-Build Indicator, see Data Appendix to the chapter. Data for Tobin’s Q: U.S. Bureau of Economic Analysis through Global Insight (series codes: FAPNREZ for current cost of corporate fixed assets). The market value of stocks and bonds splices data from the following two sources. 1932–1951: Global Financial Data (market value of corporate stocks and market value of bonds on the NYSE). 1952–2007: Federal Reserve Board through Global Insight (series codes: FL893064105 for market value of corporate equities; FL263164003 for market value of foreign equities held by US residents; FL893163005 for market value of corporate and foreign bonds; FL263163003 for market value of foreign bonds held by US residents).

According to the chart, US capitalists have gone out of their minds: instead of investing in what is cheap, they have been systematically overspending on the expensive! Note that the two series move not inversely, but together. When Tobin’s Q rises, so does the buy-to-build ratio — which means that capitalists prefer costlier mergers and acquisition over cheaper greenfield. And when Tobin’s Q falls, so does our buy-to-build indicator — which suggests that they prefer pricier new factories over the inexpensive secondhand assets available on the market.

Of course, the problem here is not the capitalists; it’s the theory. If the positive correlation of the two series seems anomalous, it is only because we use a neoclassical logic that denies power in order to explain a process that is all about power.

The specific blind spot is prices. Locked into the atomistic individualism of the nineteenth century, liberal analysts tend to assume that prices are given by the market, and that the only thing capitalists need to do is minimize cost. Yet, as we have seen in Chapter 12 — and as the large owners know full well — this pricing ethics is a relic of history. In the new state of capital, the power struggle is fought over prices as well as costs. The issue is not only to reduce the latter, but also to actively maintain and increase the former. And this simultaneity changes the whole ‘buy or build’ calculus.

New capacity indeed may be cheap if only a few capitalists add it. But if many capitalists do the same, the calculus becomes very different. The latter circumstances spell ‘glut’; glut means the disintegration of full-cost pricing; and if prices end up dropping faster than costs, the consequence is falling profit. In this context, building green-field factories — although seemingly ‘cheaper’ than existing assets — is a recipe for business disaster. As we explain below, dominant capital understands this power logic all too well and acts accordingly. And as the emphasis flips from passively accepting prices to actively managing them, Tobin’s Q turns from a cause to a consequence: it goes up when investors happen to buy and down when they decide to build.

From classical Marxism to monopoly capitalism

In short, mergers and acquisitions, although pursued by individual firms, occur within a broader and ever-changing political–economic context. It is only when we make this restructuring process the centre of our analysis that the general pattern of amalgamation begins to make sense.

A highly interesting attempt in this direction was offered by Michael Lebowitz (1985), who tried to derive the tendency toward monopoly capitalism from the very logic of classical Marxism. According to Marx, argues Lebowitz, the essence of accumulation is the expropriation of means of production — initially from workers, but ultimately also from most capitalists — until capital becomes One, a unitary amalgamate held by a single capitalist or a single corporation. The road toward such amalgamation, Lebowitz continues, proceeds through horizontal, vertical and conglomerate integration (although not necessarily following the stylized pattern in Figure 15.2), and the key challenge is to show that all three phenomena are inherent in the inner logic of accumulation.

To establish this link, Lebowitz begins by assuming, along with Marx, an intrinsic connection leading from productivity growth to accumulation. Next, he suggests that all three forms of integration increase efficiency and hence contribute to accumulation: horizontal integration creates economies of scale; vertical integration leads to more roundabout, or mechanized production runs; and conglomerate integration improves allocative efficiency through inter-sectoral capital mobility. To constrain any of these processes therefore is to hinder accumulation; and since according to Marx capital works to dismantle its own barriers, it follows that all three types of integration are inevitable, and that capitalism is destined to become monopolistic.

Based on its own premises, this logic is undoubtedly elegant. But the premises are partly incorrect as well as incomplete. The first problem concerns production. As noted earlier, beyond a certain point there is no necessary connection between industrial size and measured efficiency/profitability, so complete business integration cannot be attributed to the ‘productive’ logic of accumulation.248

The second problem is the absence of power. Even if greater industrial integration were always more efficient and more profitable, that would still leave unexplained a growing proportion of mergers that merely fuse ownership while leaving production lines separate. The difficulty is most clearly illustrated in the case of conglomerate integration. Inter-sectoral capital movement can improve allocative efficiency only through green-field investment; but, if so, why does conglomerate consolidation almost invariably take the route of merger?

The answer, by now a bit tedious, is that business consolidation is not about efficiency but about the control of efficiency. While capital is forever trying to remove the barriers to its own accumulation, this very accumulation is inherently impossible without imposing barriers on others, including on most other capitalists. The act of merger fulfils both of these requirements, allowing investors to exercise their freedom to hinder.

Differential advantage

Seen from a differential-accumulation perspective, amalgamation is a power process whose goal is to beat the average and redistribute control. Its main appeal to capitalists is that it contributes directly to differential breadth, yet without undermining and sometimes boosting the potential for differential depth.249 In addition, by making the fused entities ever larger, increasingly intertwined with other larger firms and government bodies, and more involved in setting polices and regulations, mergers stabilize earnings growth and therefore reduce differential risk.250 Finally, mergers often generate differential hype that owners can leverage to their own advantage.

Thus, everything else remaining the same, it makes more sense to buy than to build. But then everything else does not and indeed cannot remain the same. The reason is simple: amalgamation creorders the very conditions on which it is based.251

Three transformations

Three particular transformations need noting here. First, amalgamation is akin to eating the goose that lays the golden eggs. By gobbling up takeover targets within a given corporate universe, acquiring firms are depleting the pool of future targets. Unless this pool is somehow replenished, mergers and acquisitions are bound to create a highly centralized structure in which dominant capital owns everything worth owning. From a certain point onward, therefore, the pace of amalgamation has to decelerate. Although further amalgamation within the circle of dominant capital itself may be possible (large firms buying each other), the impact on the group’s differential accumulation relative to the average is negligible: by this stage, dominant capital has grown so big it is the average.

Green-field growth, by adding new employment and firms, works to replenish the takeover pool to some extent. But then, and this is the second point worth noting, since green-field growth tends to trail the pace of amalgamation in both employment volume and dollar value, its effect is mostly to slow down the depletion process, not to stop it. Indeed, the very process of amalgamation, by directing resources away from green-field investment, has the countervailing impact of reducing growth, and that reduction hastens the depleting process. Thus, sooner or later, dominant capital is bound to reach its ‘envelope’, namely the boundaries of its own corporate universe with few or no takeover targets to speak of.252

Finally, corporate amalgamation is often socially traumatic. It commonly involves massive dislocation as well as significant power realignments; it is restricted by the ability of broader state institutions to quickly accommodate the new corporate formations; and it is capped by the speed at which the underlying corporate bureaucracy can adapt (a point emphasized by Penrose 1959). The consequence is that as amalgamation builds up momentum, it also generates higher and higher roadblocks, contradictions and counter-forces.253

Taken together, the depletion of takeover targets, the negative effect on growth associated with lower levels of green-field investment and the emergence of counter-forces suggest that corporate amalgamation cannot possibly run smoothly and continuously (Proposition 4 in Chapter 14).

Breaking the envelope

But then, why should amalgamation move in cycles? In other words, why does the uptrend resume after it stumbles? And what does this resumption mean?

From the perspective of dominant capital, amalgamation is simply too important to give up. And while there may not be many candidates worth absorbing in their own corporate universe, outside of this universe targets are still plentiful. Of course, to take advantage of this broader pool, dominant capital has to break through its original ‘envelope’ — which is precisely what happened as the United States moved from one wave to another (Proposition 5 in Chapter 14).

The first, ‘monopoly’ wave marked the emergence of modern big business, with giant corporations forming within their own original industries. Once this source of amalgamation was more or less exhausted, further expansion meant that firms had to move outside their industry boundaries. And indeed, the next ‘oligopoly’ wave saw the formation of vertically integrated combines whose control increasingly spanned entire sectors, such as in petroleum, machinery and food products, among others. The next phase opened up the whole US corporate universe, with firms crossing their original boundaries of specialization to form large conglomerates with multiple business lines ranging from raw materials, through manufacturing, to services and finance. Finally, with the national scene having been more or less integrated, the main avenue for further expansion now is across international borders, hence the latest global merger wave.254

Until recently, the global wave was characterized by considerable de-conglomeration, with many firms refocusing on so-called core activities where they enjoyed a leading profit position. The main reason is that globalization enables additional intra-industry expansion across borders while legitimizing further domestic centralization in the name of ‘global competitiveness’. Eventually, though, such refocusing is bound to become exhausted, pushing dominant capital back toward conglomeration — and this time on a global scale. In fact, such re-conglomeration is already happening in areas such as computing, communication, transportation and entertainment, where technological change is rapidly blurring the lines between standard industrial classifications.255

And, indeed, the pivotal impact of mergers is to creorder not capitalist production but capitalist power at large. The reason is rooted in the dialectical nature of amalgamation. By constantly pushing toward, and eventually breaking through their successive social ‘envelopes’ — from the industry, to the sector, to the nation-state, to the world as a whole — mergers create a strong drive toward ‘jurisdictional integration’, to use Olson’s terminology (1982). Yet this very integration pits dominant capital against new rivals under new circumstances, and so creates the need to constantly creorder the wider power institutions of society, including the state of capital, international relations, ideology and violence.

Although this merger-driven creordering of power is yet to be theorized and empirically investigated, some of its important patterns can be outlined tentatively. In the remainder of the chapter we examine several key developments that unfold as mergers enter their ultimate, global envelope.

Globalization

From the viewpoint of capital as power, globalization is the capitalization of power on a global scale, and its key vehicle is the movement of capital.256 The notion of ‘movement’ here can have different meanings, so some clarification is in order before we begin.

In common parlance, reference to international capital mobility connotes a macro-statist frame of reference: capital is seen as an ‘economic–productive’ entity that somehow ‘flows’ from one state to another. But that isn’t what happens in practice. By definition, capital mobility is a purely pecuniary process. Usually, the only thing that happens is a reshuffle of ownership claims, in which foreign capitalists acquire an asset from (or sell one to) their domestic counterparts. Occasionally, the acquisition alters the value of the transacted asset, but that change, too, is entirely pecuniary. The accountants simply adjust the value of equity or debt on the right-hand side of the balance sheet and of goodwill on the left-hand side, and that’s it.

There is no cross-border flow of machines, structures, vehicles, technical know-how, or employees. These items may or may not move later on, but such movements are merely rearrangements of the left-hand side of the balance sheet; they have no bearing on the act of foreign investment per se.

The real impact of capital flows is on the underlying nature of power. When ownership crosses a border, it alters the organization and institutions of power on both sides of that border and, eventually, the significance of the border itself. In this sense, capital mobility creorders the very state of capital — from within and from without — and it is this fundamental transformation that we need to decipher.

Capital movements and the unholy trinity

Most analyses of capital movement concentrate on its alleged cyclicality. The common view is that, although capital flow has accelerated since the 1980s, the acceleration is part of a broader recurring pattern, and that the peaks of this process in fact were recorded during the late nineteenth and early twentieth centuries (Taylor 1996).

The standard approach to these ups and downs in capital mobility is the so-called ‘Unholy Trinity’ of international political economy. According to this framework, there is an inherent trade-off between (1) state sovereignty, (2) capital mobility and (3) international monetary stability — three conditions of which only two can coexist at any one time (Fleming 1962; Mundell 1963; Cohen 1993).257

Thus, during the ‘liberal’ Gold Standard that lasted until the First World War, limited state sovereignty allowed for both free capital mobility and international monetary stability. During the subsequent inter-war period, the emergence of state autonomy along with unfettered capital flow served to upset this monetary stability. After the Second World War, the quasi-statist system of Bretton Woods put a check on capital mobility so as to allow domestic policy autonomy without compromising monetary stability. Finally, since the 1970s, the rise of neoliberalism has, again, unleashed capital mobility, although it is still unclear which of the other two nodes of the Trinity — state sovereignty or monetary stability — will have to give.

Why has the world moved from liberalism, to instability, to statism and back to (neo)liberalism? Is this some sort of inevitable cycle, or is there an underlying historical process here that makes each ‘phase’ fundamentally different? The answers vary widely.258

Liberal interpretations emphasize the secular impact of technology that constantly pushes toward freer trade and greater capital mobility, with unfortunate setbacks created by government intervention and distortions. From this perspective, post-war statism, or ‘embedded liberalism’ as Ruggie (1982) later called it, was largely a historical aberration. After the war, governments took advantage of the temporary weakness of capitalism to impose all sorts of restrictions and barriers. Eventually, though, the unstoppable advance of information and communication forced them to succumb, as a result of which the rate of return rather than political whim once again governs the movement of capital.

Critics of this natural-course-of-things theory tend to reverse its emphasis. Thus, according to Helleiner (1994), the key issue is neither the expansionary tendencies of technology and markets, nor their impact on the propensity of capital to move, but rather the willingness of states (i.e. governments) to let such movements occur in the first place. From this viewpoint, state regulation is not an aberration, but rather the determining factor — and one that governments remain free to switch on and off.

One important reason for such cyclical change of heart, suggests Frieden (1988), is the shifting political economy of foreign debt. According to this view, during the Gold Standard, Britain became a ‘mature creditor’, and therefore was interested in liberalization so that its debtors could have enough export earnings to service their foreign liabilities. The United States reached a similar position during the 1970s, and since then it has used its hegemonic power to re-impose liberalization for much the same reason. According to Goodman and Pauly (1995), this second coming of liberalism was further facilitated by the desire of governments to retain the benefits of transnational production. The latter desire required that they also open the door to transnational financial intermediation, hence the dual rise of portfolio and foreign direct investment.

Global production or global ownership?

Plus ça change, plus c’est pareil? According to the globalization sceptics, the answer is pretty much yes. Despite the recent increase in capital mobility, they point out, most companies remain far more national than global (see for instance, Doremus et al. 1998; Weiss 1998; Hirst and Thompson 1999). The extent of transnational production is fairly limited: its share in global GDP rose from 5.6 per cent in 1982, to 6.8 in 1990, to 10.1 per cent in 2006. Even the world’s top 100 transnational corporations are not yet ‘fully’ global: their 2005 ‘Transnationality Index’ — defined as the average of the ratios of foreign to total assets, foreign to total sales, and foreign to total employment — is only 60 per cent, compared to 51 per cent in 1990.259

The data themselves are hard to argue with — only that they aren’t really the relevant ones to use. As noted in the preamble to this section, capital flow denotes the movement not of machines or production, but of ownership. The key issue, therefore, is not the location of factories and employees, but of the capitalists, and from this latter perspective the picture looks very different.

Seen from the assets side of the balance sheet, a company whose factories and offices are all located in the United States is entirely ‘domestic’. But this ‘all-American’ production tells us nothing about the company’s liabilities. If its owners float bonds on the European market, borrow money from a Kuwaiti bank, or sell their equity to a Korean capitalist, their company — although still ‘domestically’ located — suddenly becomes ‘global’.

How extensive is the globalization of ownership as distinct from the globalization of production? According to recent research by the McKinsey Global Institute, between 1990 and 2006 the global proportion of foreign-owned assets has nearly tripled, from 9 per cent to 26 per cent. The increase was broadly based: foreign ownership of corporate bonds rose from 7 to 21 per cent, of government bonds from 11 to 31 per cent and of corporate stocks from 9 to 27 per cent (Farrell et al. 2008: p. 73, Exhibit 3.10).

How do these ratios compare to the situation during the late nineteenth and early twentieth centuries, a period when capital mobility was supposedly hitting a record high? Since there are no data on global assets in that earlier period, the question is impossible to answer directly. But we can examine the process indirectly, by measuring the growth of global assets relative to global GDP. This comparison is presented in Figure 15.4. The estimates, taken from the work of Obstfeld and Taylor (2004), show the ratio of gross foreign assets (comprising cash, loans, bonds and equities owned by non-residents) to world GDP.

Figure 15.4: Ratio of global gross foreign assets to global GDP

* Gross foreign asset stocks consist of cash, loans, bonds and equities owned by non-residents.

Source: Obstfeld and Taylor (2004), pp. 52–53, Table 2-1.

Based on this approximation, the historical transnationalization of ownership seems far less cyclical that the globalization sceptics would like to believe. The chart confirms the build-up of foreign assets during the latter decades of the nineteenth century, as British imperialism was approaching its zenith; it shows the relative build-down of these assets during the first half of the twentieth century, as instability, depression, wars and capital controls hampered the movement of capital; and it demonstrates the resurgence of foreign ownership since the early 1970s, as embedded liberalism gave rise to global capitalism.

The amplitude of this long-term ‘cycle’, though, has increased quite a bit. During the previous phase, foreign assets peaked at less than 20 per cent of world GDP; in the current phase, which so far shows no sign of abating, their ratio to GDP has already surpassed 90 per cent.

Net or gross?

The question, then, is: How could a supposedly cyclical pattern of foreign capital flows generate what seems like a secular surge in foreign capital stocks? The answer is twofold. First, even if the movement of capital indeed ebbs and flows, over time the impact it has on the level of capital stocks tends to be cumulative (a point emphasized by Magdoff 1969). A second point, less intuitively obvious but equally important, is that the movement of capital may not be as cyclical as it seems.

Note that most analyses of capital flow concentrate on net movements — namely, on the difference between inflow and outflow.260 This choice is inadequate and potentially misleading. Capitalist integration and globalization can move both ways, which means that the proper measure to use here is the gross flow — that is, the sum of inflow and outflow (Wallich 1984). The net and gross magnitudes are the same when capital goes only in one direction, either in or out of a country. But when the flow runs in both directions, the numbers could be very different.

The divergence of the two measures is clearly illustrated in Figure 15.5. The chart contrasts the net and gross capital flows in the G7 countries (with both series expressed as a per cent of the G7’s gross fixed capital formation).261 It shows that since the 1980s, the relative increase of gross private flows was both powerful and secular, whereas that of net flows was more limited and cyclical. As a result, by 2007 the value of gross flows reached 82 per cent of green-field investment, compared to only 16 per cent per cent for net flows.262

Figure 15.5: G7 cross-border private investment flows as a per cent of gross fixed capital formation

Note: Series are smoothed as 3-year moving averages. Flows comprise direct and portfolio investment. Gross flows are computed as the sum of inflows and outflows. Net flows are computed separately for each country as the difference between inflows and outflows and are then converted into absolute values and aggregated. Each series denotes the ratio of overall G7 flows to overall G7 gross fixed capital formation, both in $US.

Source: IMF’s International Financial Statistics through Global Insight (series codes: LAF for the $US exchange rate; L93E&C for gross fixed capital formation); IMF’s Balance of Payment Statistics through Global Insight (series codes: B4505 for direct investment abroad; B4555Z for direct investment in the reporting country; B4602 for portfolio investment abroad; B4652Z for portfolio investment in the reporting country); Global Insight International Database (series codes RX@UZ for Euro/$US exchange rate; IFIX@EURO for fixed capital formation from 1998 for EU countries).

Unfortunately, lack of historical data on gross movements makes it difficult to compare current developments with conditions prevailing at the turn of the twentieth century. Nonetheless, the facts that the share of gross investment in GDP was generally higher then than now and that two-way capital flow is a relatively recent phenomenon, together serve to suggest that the current pace of globalization, let alone its level, may well be at an all time high.

Capital flow and the creorder of global power

Theoretically, the common thread going through most analyses is the belief that capital flows in response to the ‘primordial’ forces of production and trade. According to this view, capital flows are directed by profit signals; profit signals show where capital is most needed; and capital is most needed where it is the most productive (comparatively or otherwise).

To us, this view is akin to putting the world on its head. The global movement of capital is a matter not of production and efficiency but of ownership and power. On its own, the act of foreign investment — whether portfolio or direct — consists of nothing more than the creation or alteration of legal entitlements.263 The magnitude of such foreign entitlements — just like the magnitude of domestic entitlements — is equal to the present value of their expected future earnings. And since the level and pattern of these earnings reflect the control of business over industry, it follows that cross-border flow of capital reflects the restructuring not of global production, but of global capitalist power at large.264

One of the first writers to approach international capital mobility as a facet of ownership and power was Stephen Hymer (1960). In his view, firms would prefer foreign investment over export or licensing when such ownership conferred differential power, or an ‘ownership advantage’ as it later came to be known. Based on this interpretation, the power of US-based foreign investors seems to have risen exponentially over the past half-century, as illustrated in Figure 15.6.

Figure 15.6: The globalization of US business: ownership vs trade

* Receipts from the rest of the world as a per cent of corporate profit after tax.

Note: Series are smoothed as 5-year moving averages.

Source: U.S. Bureau of Economic Analysis through Global Insight (series codes: GAARP till 1998 and ZBECONRWRCT from 1999 for after tax corporate profit receipts from the rest of the world; ZA for after tax corporate profit; X for export; GDP for GDP).

The chart presents two proxies for the globalization of US business. The first proxy, measuring the share of export in GDP, provides a rough indication of the contribution to overall profit of outgoing trade. The second, measuring the share of foreign operations in overall net corporate profit, approximates the significance of foreign as opposed to domestic investment.

Up until the 1950s, the relative contribution to profit of foreign assets was similar to that of export (assuming domestic and export sales are equally profitable, so that the ratio of export to GDP corresponds to the ratio of export profit to overall profit). But since then, the importance for profit of foreign investment has grown much faster than that of trade, reaching one third of the total in recent years. This faster growth of foreign profit may seem perplexing since, even with the recent resurgence of capital mobility, US trade flows are still roughly three times larger than capital flows. But then, unlike trade, investment tends to accumulate, and that accumulation eventually causes overseas earnings to outpace those generated by export.

This divergence serves to heighten the power underpinnings of trade liberalization. Advocates of global integration, following in the footsteps of Adam Smith and David Ricardo, tend to emphasize the central role of ‘free trade’. Unhindered exchange, they argue, is the major force underlying greater efficiency and lower prices. And as it stands their claim may well be true. Indeed, downward price pressures are one reason why dominant capital is often half-hearted about indiscriminate deregulation, particularly when such deregulation allows competitors to undermine its differential margins. Yet despite this threat, large firms continue to support freer trade, and for a very good reason. For them, free trade is a means to something much more important, namely free investment — or more precisely, the freedom to impose and capitalize power.

Foreign investment and differential accumulation

Although difficult to ascertain with available data, the cumulative (albeit irregular) build-up of international investment must have contributed greatly to the differential accumulation of US dominant capital. The reason is that whereas exports augment the profits of small as well as large firms, the bulk of foreign earnings go to the largest corporations. Therefore, it is the globalization of ownership, not trade, which is the real prize. While free trade can boost as well as undermine differential accumulation, free investment tends mostly to raise it. But then, since free investment can come only on the heels of liberalized trade, the latter is worth pursuing, even at the cost of import competition and rising trade deficits.

Foreign investment, like any other investment, is always a matter of power. The nature of this power, though, has changed significantly over time. Until well into the second half of the nineteenth century, the combination of rapidly expanding capitalism and high population growth enabled profitability to rise despite the parallel increase in the number of competitors.265 There was only a limited need for business collusion and the explicit politicization of accumulation — and, as a result, most capital flows were relatively small portfolio investments, associated mainly with green-field expansion (Folkerts-Landau, Mathieson, and Schinasi 1997, Annex VI).

Eventually, though, excess capacity started to appear, giving rise to the progressive shift from green-field to amalgamation as described earlier in the chapter. Yet for more than half a century this shift was mostly domestic, with mergers and acquisitions first having to break through their various national ‘envelopes’. It was only since the 1970s and 1980s that the process became truly global, and it was only then that the character of capital flow started to change.

The need to exert control has moved the emphasis gradually toward larger, ‘direct’ foreign investment, while the threat of excess capacity has pushed such investment away from green-field and toward amalgamation. At present, over 75 per cent of all foreign direct investment takes the form of cross-border mergers and acquisitions (United Nations Conference on Trade and Development 2000: 117, Figure IV.9).

From a power perspective, therefore, one could say that during the late nineteenth and early twentieth centuries capital mobility was still largely a matter of ‘choice’. But by the end of the twentieth century it became more or less a ‘necessity’, mandated by the combination of excess capacity and the cumulative build-up of giant firms, for which profitable expansion increasingly hinges on global amalgamation and creeping stagnation (Proposition 3 in Chapter 14).266

In summary, there is a long but crucial link leading from the broad power imperatives of capitalism, to the logic of differential accumulation, to amalgamation, to capital mobility (Proposition 5 in Chapter 14). From this viewpoint, the purpose of globalization is not aggregate growth but differential gain; it is driven not by the quest for greater global efficiency, but by the need to control efficiency on a global scale; and finally and most importantly, it is inherent in the capitalist creorder. Without the globalization of ownership, dominant capital cannot break its national envelope; and if it cannot go global, its differential breadth is bound to collapse. In this sense, globalization is part of the inner logic of accumulation. It can be reversed only by altering that logic, or by moving away from it altogether.

Appendix to Chapter 15: data on mergers and acquisitions

There are no systematic historical time series for mergers and acquisitions in the United States (other countries have even less information). The mergers and acquisitions series constructed in this chapter and plotted in Figures 15.2 and 15.3 is computed on the basis of various studies. These studies often use different definitions, covering different universes of companies.

The dollar values of mergers and acquisition for the 1895–1919 period are taken from Nelson (1959, Table 14, p. 37), whereas those covering the 1920–29 period come from Eis (1969), as reported in Historical Statistics of the United States (U.S. Department of Commerce. Bureau of the Census 1975, Vol. 2, Table V38–40, p. 914). Both data sets cover manufacturing and mining transactions only and thus fail to reflect the parallel amalgamation drive in other sectors (Markham 1955).

Data for the 1930–66 period are from the U.S. Federal Trade Commission, reported in Historical Statistics of the United States (1975, Vol. 2, Table V38–40, p. 914). These data, again covering only manufacturing and mining, pertain to the number of transactions rather than their dollar value. Significantly, though, the number of mergers and acquisitions correlates closely with the value ratio of mergers and acquisitions to green-field investment during previous and subsequent periods for which both are available (the 1920s and 1960s–1980s). In our computations, we assume that there is a similar correlation during 1930–66 and use the former series (with proper re-basing) as a proxy for the latter ratio.

From 1967 onward, we again use value data which now cover all sectors. Figures for 1967–79 are from W.T. Grimm, reported in Weston (1987, Table 3.3, p. 44). For 1980–83, data are from Securities Data Corporation, comprising transactions of over $1 million only. The next batch, covering the period from 1984 to the 2003, consists of transactions of $5 million or more and is from Thompson Financial. The data for 2004–7, also from Thompson Financial, cover transactions of $10 million or more. These latter data are spliced with the previous series for consistency.

In constructing our indicator for the ratio of mergers and acquisitions to gross fixed investment, we divided, for each year, the dollar value of mergers and acquisitions by the corresponding dollar value of gross fixed private domestic investment. Until 1928, the green-field investment data pertain to total fixed investment (private and public) and are taken from the Historical Statistics of the United States (1975, Vol. 1, Series F105, p. 231). From 1929 onward, the data cover gross fixed private investment and are from the U.S. Bureau of Economic Analysis via Global Insight (series code: IF). For the 1930–66 period, we spliced in the number of deals, linking it with prior and latter value ratios.

Throughout the chapter, we use the term ‘green-field investment’ to denote the purchase of newly produced plant and equipment. The production of these items is distinct from the process of accumulation.↩

Note that not all ‘active corporations’, as the IRS classifies them, accumulate. Many firms are incorporated solely for legal purposes, tax evasion, etc., and often have neither assets nor employees. The proportion of such firms is fairly large but also fairly stable. According to the IRS, in 2004 roughly 12 per cent of all active corporations had no assets (zero book value) — a bit less than in 1935, when 13 per cent of corporations were in the same position. The long-term stability of this ratio means that the attendant bias need not concern us here.↩

Our measurements here are not strictly comparable: we contrast the number of corporations with overall non-agricultural private employment (that also includes proprietorships and partnerships), rather than with corporate employment only (for which data are not publicly available). However, we can assess the accuracy of this comparison indirectly, by looking at the share of corporations in nonfarm private GDP (using data from the U.S. Bureau of Economic Analysis, Tables 1.3.5 and 1.14). This share rose from 61 per cent in 1929 to 67 per cent in 2007 — a 10 per cent increase. Now, if we assume that relative employment trends roughly track relative GDP trends, the implication is that, over the entire period, corporate employment rose by only 10 per cent more than overall nonfarm employment. Compared to the threefold rise in nonfarm private employment reported in the text, this bias is too small to affect the overall results.↩

For a neo-Marxist analysis of this long-term policy bias, see Steindl (1979).↩

The effect on relative employment growth is probably somewhat smaller than implied by the dollar figures. First, amalgamated companies often end up shedding some workers, and second, merger and acquisition data include divestitures that reduce rather than raise employment (though only if the acquirer isn’t part of dominant capital). Correcting for these qualifications, though, isn’t likely to alter the overall trend.↩

The literature on ‘measuring’ transaction costs is reviewed sympathetically by Wang (2007) and Macher and Richman (2008). For a critical assessment, see Buckley and Chapman (1997).↩

For more on the contrast between power and efficiency arguments here, see Knoedler (1995).↩

See for example, Ravenscraft and Scherer (1987), Caves (1989), Bhagat, Shleifer and Vishny (1990) and Kaplan (2000).↩

For instances of this approach, see Ravenscraft (1987), Ravenscraft and Scherer (1989), Scherer and Ross (1990: Ch. 5) and Healy, Palepu and Ruback (1992).↩

See also footnote 12 in Chapter 12, for the accumulation consequences of Japan’s anti-merger/all-for-growth attitude.↩

Economies of scale, impressive as they were in Marx’s time, are not a timeless iron law, but rather historically and technologically contingent. Diseconomies of scale can be as important, and there is no reason to believe that completely centralized planning, capitalist or otherwise, is most efficient (recall our discussion in Chapter 12 of industrial ‘resonance’ and the open-ended democratic notion of ‘efficiency’). Similarly with roundabout processes: longer production runs may be more efficient, but only up to a point, beyond which they almost always run into organizational barriers.↩

1 Note that the act of merger itself has no direct effect on depth. The impact on depth works only indirectly, through increasing corporate centralization — and even that is merely a facilitating factor. Consolidation makes it easier for firms to collude as well as to fuse with government organs. But that facilitation doesn’t imply that collusion and fusion will actually take place, or that they will be effective.↩

This power perspective is usually lost on financial analyses of merger. As we saw in Chapter 11, the standard view on risk reduction focuses on diversification. Merger does the job when it fuses firms with divergent volatility patterns. But according to the analysts, owners can achieve the same reduction with far less hassle simply by including shares of the pre-merged firms in a diversified financial portfolio.

The glitch in this argument is that the owned entities in the two cases are very different. To see why, imagine a capitalist owning 1 per cent of the shares of every independent oil refiner that populated the business landscape before the arrival of John D. Rockefeller. Now compare this scenario to one in which the capitalist owns a 1 per cent stake in Rockefeller’s Standard Oil of New Jersey after the company absorbed all these independent refiners. The diversification of the two ownership stakes is technically identical, but their earnings pattern most certainly is not. Historically, the ‘before’ case was associated with cutthroat competition and the absence of organized power, which together meant massive volatility; in the ‘after’ case, the political–economic regime imposed by Standard Oil brought a more stable flow of earnings and greatly reduced risk.↩This creordering is also why most macro studies of mergers and acquisitions, such as Mitchell and Mulherin (1996), Weston, Chung and Siu (1998) or Winston (1998), are usually insufficient. Although these studies acknowledge the role of structural changes, such as increased competition, technical change and policy deregulation, they tend to treat these changes as external societal ‘shocks’ to which business ‘responds’ with amalgamation.↩

A typical illustration of this process is provided by the food business (based on data from the authors’ archives). During the 1980s, the sector went through rapid amalgamation. In 1981, a $1.9 billion merger between Nabisco and Standard Brands created Nabisco Brands, which then merged in a $4.9 billion deal with R.J. Reynolds to create RJR Nabisco. A few years later, KKR, which had earlier acquired Beatrice for $6.2 billion, paid $30.6 billion to take over RJR Nabisco in what was then the largest takeover on record. Elsewhere in the sector, Nestlé took over Carnation ($2.9 billion) and Rowntree ($4.5 billion); Grand Metropolitan acquired Pilsbury ($5.7 billion) and Guinness ($16 billion); Phillip Morris bought General Foods ($5.7 billion) and Kraft ($13.4 billion); BCI Holdings took over some Beatrice divisions ($6.1billion); and Rhône-Poulenc bought Hoechst ($21.9 billion). By the end of the 1980s, the merger flurry died down. According to the Financial Times, food companies at the time were very cheap, yet ‘shareholders have deserted food stocks … partly because of the absence of genuinely attractive acquisition targets’ in an industry whose ‘biggest problem has been minimal sales growth’ (Edgecliffe-Johnson 2000). During the 1990s, there were a few more big transactions, such as the $14.9 billion acquisition of Nabisco by Philip Morris, but these were mostly reshuffles of assets among the large players. The experience of reaching the ‘envelope’ was summarized metaphorically by a Bestfood executive whose company had been taken over by Unilever: ‘I have been to Bentonville, Arkansas [home of Wal-Mart’s headquarters], and I would like to say that it is not the end of the world, but you can see it’ (ibid.).↩

The 1933 Glass-Steagall Act, for instance, barred US banks from making industrial investments, a prohibition that only recently has been relaxed. Similar transformational effects were brought on by the post-war dismantling of the Japanese Zaibatsu, by the 1990s unbundling of South African holding groups and the divestment of Israeli banks of their ‘non-financial’ holdings, and by the transnationalization of the Korean Chaebol during the 2000s.↩

The process of course is hardly unique to the United States. For example, ‘Before [South Africa] started the progressive unwinding of exchange controls in 1994’, writes the Financial Times, ‘large companies were prevented from expanding overseas. With capital trapped at home, they gobbled up all available companies in their industries before acquiring companies in other sectors and becoming conglomerates’ (Plender and Mallet 2000). For analyses of differential accumulation, business consolidation and globalization in South Africa and Israel, see Nitzan and Bichler (1996) and Nitzan and Bichler (2001).↩

For instance, information, telecommunication and entertainment companies such as Cisco, Alcatel-Lucent, Microsoft, Time Warner, NewsCorp, Hutchison Whampoa and Vivendi increasingly integrate computing (hardware and software), services (consulting), infrastructure (cables and satellite), content (television, movies, music and print publishing) and communication (internet and telephony), while leisure firms like Carnival Cruise own shipping lines, resort hotels, air lines and sport teams. Other companies, like General Electric or Philip Morris, have never abandoned conglomeration in the first place and continue spreading in numerous directions.↩

Globalization of course has numerous other dimensions, but these are secondary for our purpose here. For more on the globalization debate, see Gordon (1988), Du Boff et al. (1997), Sivanandan and Wood (1997), Burbach and Robinson (1999), Hirst and Thompson (1999), Radice (1999), Sutcliffe and Glyn (1999) and Mann et al. (2001–2).↩

The rationale is based on the external account identity between the current and capital balances. If the international monetary system were to remain stable (in terms of exchange rates), governments can retain domestic sovereignty over exports and imports only if capital movements are controlled to ‘accommodate’ the resulting current account imbalances. In the absence of such capital controls, governments would have to give up their policy autonomy; if they don’t, the mismatch between the current and capital balances would lead to currency realignment and international monetary instability.↩

For views and reviews, see Cerny (1993), Helleiner (1994), Sobel (1994) and Cohen (1996).↩

The ratios in the paragraph are computed from the United Nations Conference on Trade and Development (2000, Table I.1, p. 4 and Table III.3, p. 76; 2007, Table I.4 p. 9 and Table I.12 p. 26).↩

The main reason for this choice is convenience. Direct data on capital flow often do not exist; those that do exist are difficult to obtain; and most of those who write on the subject prefer to stay clear of empirical research in the first place. Unfortunately, the analysts have found an easy way around these difficulties. The national accounting identities make net capital flow equal to the current account deficit, by definition; and since data for the latter are readily available, most writers simply use them to approximate the former.↩

We stick to the G7 (G8 without Russia) in order to maintain sufficiently long time series.↩

Note that the series in Figure 15.5 are based on end-of-year data and therefore fail to reflect shorter ‘hot money’ movements. Including these latter movements in our measure would have further widened the disparity between the gross and net flows.↩

The popular perception that ‘direct’ investment creates new productive capacity, in contrast to ‘portfolio’ investment which is merely a paper transaction, is simply wrong. In fact, both are paper transactions whose only difference is relative size: investments worth more than 10 per cent of the target company’s equity commonly are classified as direct, whereas those worth less are considered portfolio.↩

The ‘delinking’ of capital flows from the ‘underlying’ growth of production (assuming that they were previously linked) is slowly dawning even on the most religious. In a recent gathering of the world’s central bankers at the Jackson Hole Retreat, the pundits sounded almost bewildered:

Today, capital flows ‘uphill’ from poor to rich nations — above all the US — in contrast to the predictions of all standard economic theories. Moreover, as Raghu Rajan, chief economist at the International Monetary Fund, explained at Jackson Hole, there is no evidence of a positive relationship between net capital inflows and long-term growth in developing countries. Foreign direct investment may be a special case. But overall, the correlation is negative: countries that have relied less on foreign capital have grown on average faster. This is surprising, since extra capital should normally boost growth.

(Guha and Briscoe 2006, emphasis added)

But then, just to make sure that bewilderment doesn’t clash with faith, the experts quickly blame it all on ‘distortions’:

One possible explanation, Mr Rajan said, is that developing countries may be unable to absorb foreign capital effectively because they have inadequate financial systems. . . .

(Ibid.)

2 See for example, Veblen (1923, Ch. 4), Josephson (1934), Hobsbawm (1975, Chs 2–3), Arrighi, Barr, and Hisaeda (1999) and Figure 12.3 and related discussion in this book.↩

‘Economic growth’ of course is hardly an end in itself. It is only that, in capitalism, such growth is crucial for the livelihood, employment and personal security of most people.↩